Fireworks - Do They Matter?

Entering the Independence Day holiday, we had some pretty good economic news to celebrate.

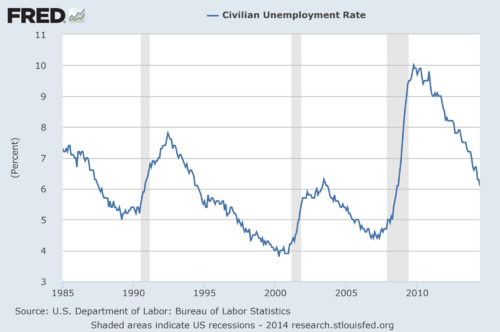

The jobs report from the Department of Labor came out on Thursday and crushed economists’ expectations. The report said the US economy added 288,000 jobs in the month of June and the unemployment rate plummeted to 6.1%, its lowest level since 2008.[i] The unemployment rate has fallen 1.4% over the past year, that's the steepest decline in over 3 decades.[ii,iii]

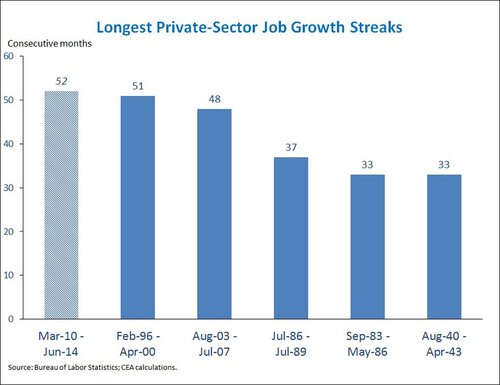

Further, the number of consecutive months that the US economy has added jobs reached a record 52 months.[iv]

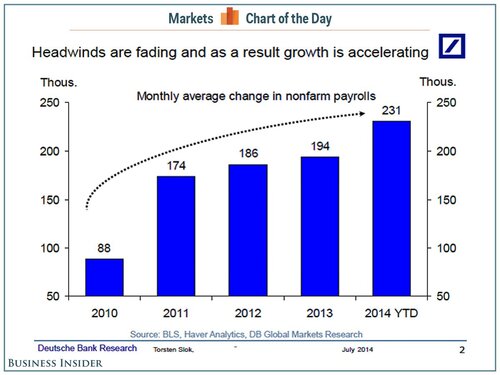

Additionally, the trend for average monthly job growth shows an improving economy.[v] It's hard to argue with the data and the Dow Jones certainly agreed by setting another record, crossing over 17,000 for the first time based upon all of the employment fireworks.

Unfortunately for all of us investors, we can't celebrate too much mostly because we have to live in the future. Capital market participants are constantly absorbing, digesting, discounting and pricing in data (especially current data like the jobs report).

To avoid getting too carried away by all the jobs-related fireworks, I tend to focus on what really drives equity valuation to get a better understanding of where prices could head.

What really matters is simple: Earnings.

We know historically that the long-run 10% stock market returns have been driven by a combination of dividends (5%) and earnings growth (5%).[vi] With the current S&P 500 dividend yield well below 5%, even higher earnings growth is needed to achieve the historic rate of return.

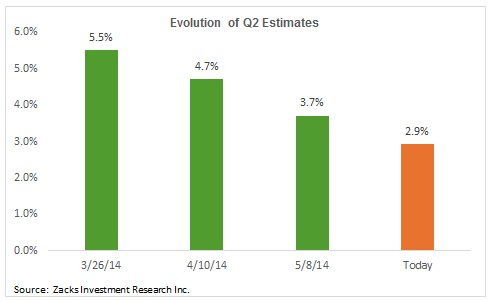

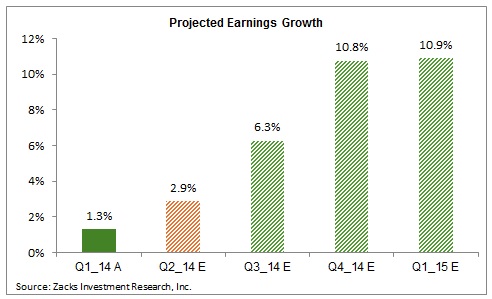

Unfortunately, current earnings growth expectations for Q2 2014 are much more muted. Both Zacks and FactSet are forecasting a benign Q2. Zacks clearly shows a degrading earnings estimate picture for most of Q2. In March, estimates suggested 5.5% EPS growth and now they sit at just over half that at 2.9%. [vii] This is clearly well below the long-term trend for the S&P 500.

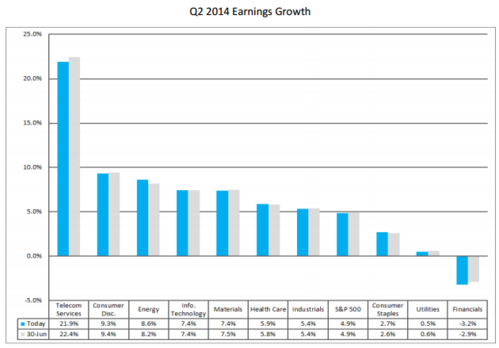

FactSet shows a slightly higher EPS growth estimate for Q2 at 4.9%.[viii]

What is compelling in all of this is the future growth being anticipated. Both FactSet and Zacks are showing considerable growth in EPS for Q3 and Q4. The 10.8% estimated Q4 growth rate is almost 3.75x the 2.9% Q2 rate.[ix]

While the employment fireworks were great, what matters is the earnings growth being forecast for Q3 and Q4. It's understandable to be cautious, especially as earnings are coming in well below long term growth averages, however, the expectation is for companies to earn more in the near future.

Perhaps it's the better jobs picture that will fuel more consumption and fulfill expectations.

That's what really matters in this part of the market cycle.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Jeff Paul, Senior Investment Analyst – Phillips & Company

References

[i] Logiurato, B. (Jul 3, 2014). The US Just Broke The Record For The Longest Stretch Of Private Sector Job Growth. Business Insider.

[ii] Ibid.

[iii] Federal Reserve Economic Data.

[iv] Logiurato, B. (Jul 3, 2014). The US Just Broke The Record For The Longest Stretch Of Private Sector Job Growth. Business Insider.

[v] Weisenthal, J. (Jul 3, 2014). CHART OF THE DAY: Here’s the Chart Obamacare Critics Don’t Want You to See. Business Insider.

[vi] Journal of Indexes. (Nov 1, 2005). Bogle’s Corner. ETF.com.

[vii] Mian, S. (Jun 26, 2014). Mixed Start to Q2 Earnings Season. Zacks.

[viii] Butters, J. (Jul 3, 2014). S&P 500 Earnings Insight. FactSet.

[ix] Mian, S. (Jun 26, 2014). Mixed Start to Q2 Earnings Season. Zacks.