Weekly CEO Commentary 9-4-12

"Snatching Defeat from the Jaws of Victory"

Weekly CEO Commentary 9-4-12

Tim Phillips, CEO – Phillips and Company

Leave it to Lincoln to come up with another great quip that is very fitting to our current monetary agenda. Allegedly, Lincoln used this phrase when he was referring to the ill-fated General Ambrose Burnside, shortly after a military defeat and subsequent sacking of said general by Lincoln.

Before we get to the Defeat Snatching component of my assessment, let's review the Jaws of Victory side of the equation.

Jaws of Victory

There are some fairly positive signs bubbling up in our economy. It's almost hard to imagine saying that in the wake of so much uncertainty.

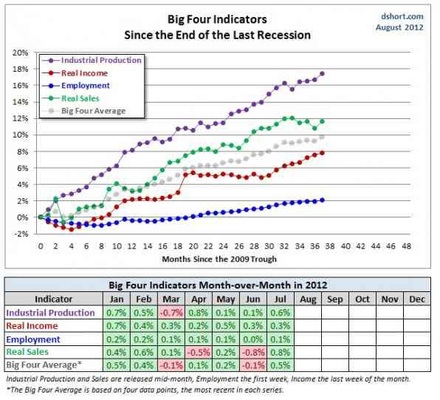

In fact, a host of economic indicators are pointing in a positive direction. If you take a look at the chart below you can see key economic factors, like employment, are improving. What's ironic is this is a chart from our friends at the ECRI (Economic Cycle Research Institute), the guys that are calling for a recession. While they may still be right, the current data is not trending their way.

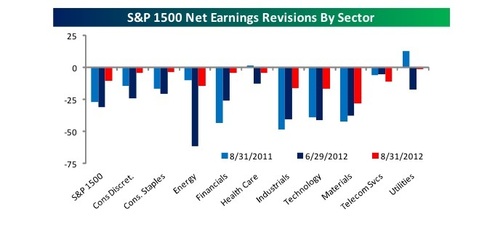

Secondly, earnings estimates have seen some improvement in the last several weeks. I turn to our source at Bespoke to help make the point. While estimates are still negative, analysts are getting more constructive on their outlook. In fact, they are getting more constructive in almost all sectors.

Snatching Defeat

Last Friday, The Federal Reserve concluded their seminal "Jackson Hole" meeting with Chairman Bernanke delivering his much anticipated closing remarks. He strongly suggested non-traditional monetary tools were effective and would be strongly considered in the future.

“the costs of nontraditional policies, when considered carefully, appear manageable, implying that we should not rule out the further use of such policies if economic conditions”

One interesting and perhaps overlooked event during the meeting was a presentation by noted Stanford economist Edward P. Lazear. He wrote a paper that suggested our current unemployment issues were not structural but cyclical. He went on to suggest much of our high unemployment might be strongly explained by "mismatch" in the labor force both within industries and between industries. Basically, people need time to get retrained and relocated from shrinking skill sets and industries to those growing and needed. One compelling point he made was:

"First, the unemployment rate was 4.4% in the spring of 2007 and rose to

10.0% by October of 2009. Thus, in a little over two years, unemployment rates went up by over5 ½ percentage points. Most structural changes do not occur so rapidly."

The bottom line is the Federal Reserve is not mandated to handle structural employment problems but cyclical ones. So, Lazear essentially provided the rationalization for further monetary intervention.

The bad news is that most market participants are expecting intervention to occur—which may actually create a sell off when it happens with traders taking profits on “buying the rumor.” Conversely, if the economy heats up and there is no intervention, market participants could be disappointed–also leading to a sell off. That's what happens when government intervention distortions a market based economy.

Ultimately though: if the fundamental economic data improves and we get a Federal Reserve induced sell off, then snatching defeat from the jaws of victory could be a great buying opportunity.

If you have questions or comments please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can Email me directly.

Tim Phillips, CEO – Phillips & Company

Research supported by:

Adam Gulledge, Associate – Phillips & Company

Alex Cook, Associate – Phillips & Company