Can't Live With It, Can't Live Without It

Can't Live With It, Can't Live Without It

Weekly Market Commentary 8-26-2013

Tim Phillips, CEO—Phillips & Company

Fixed income was once an easy asset class to allocate to. You could by US Treasuries or municipal bonds, collect good income, hedge against deflation and mitigate the risk of having equity exposure in the other part of your portfolio.

In fact, over the course of a longer period of time a 100% fixed income portfolio produced some of the best risk adjusted returns over other generic allocations.

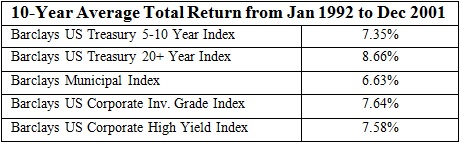

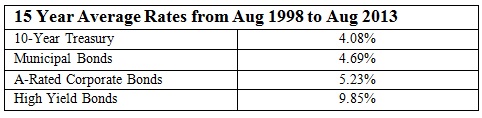

Prior to this last mega bull market in fixed income (pre-2002) the average returns you could expect from the asset was impressive [i]:

Unfortunately, today it's an entirely different time and the asset class has entirely different risks. Rising rates and Federal Reserve activity have created tremendous uncertainty and risk to fixed income. So many investors are either ignoring the risks or abandoning the asset class only to face another set of risks associated with too much equity exposure.

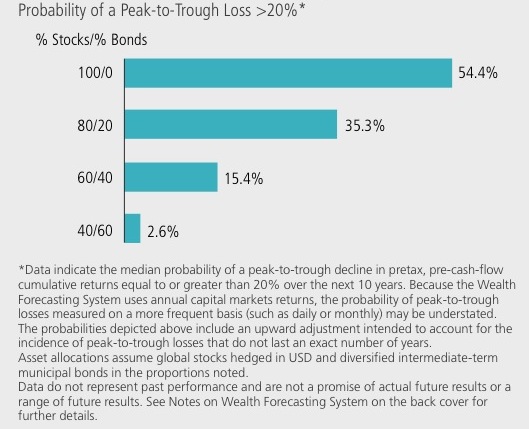

On the one hand fixed income is providing "return free risk". Yet on the other hand it does provide an excellent defense against equity risk. The chart below shows from top to bottom a 100% stock portfolio could drop 54% [ii].

We have all seen this in the not too distant past. It also suggests mixing bonds into an allocation can mitigate the drop substantially.

How to manage in today’s environment

In our current environment it's just not enough to have "bonds" in your allocation. In today's fixed income reality, you need to define your goals much more clearly with your advisor.

Let's assume almost all bonds will provide a hedge against deflation. That leaves us with 3 other basic goals for fixed income allocations: hedging against volatility in equity holdings, low risk liquidity, and of course maximizing income.

Again, in the past you could almost get all three objectives in a core bond portfolio, but today it's more complicated.

If your goal is to maximize income, you’re going to need more high yield bonds—potentially both corporate and municipal. The good news about high yield is they tend to hold up better in a rising rate environment. The tradeoff is in credit risk and some call risk.

If your goal is to maintain liquidity with low risk, you’re going to have to choose to trade off income. You can buy money markets, CD's and very short term bonds as well as some investment grade floating securities.

Finally if you goal is to hedge against your equity exposure in the other part of your allocation you might consider all of the above as well as more intermediate term bonds, long/short fixed income alternatives, industry specific bonds and mortgage backed securities.

The bottom line is you can't lock it and leave it anymore. Much better definition of your goals and time frame as well as better matching your goals to the fixed income mix will be necessary for the time being.

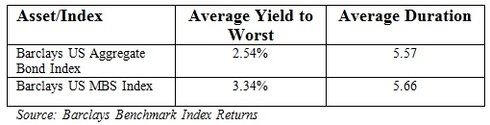

The good news is we could return to a more normal environment in the coming years. Once rates normalize you could see better normalized yields [iii]:

Until then, be prepared to adjust quickly according to your objectives.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Alex Cook, Investment Analyst – Phillips & Company

[i] Data table source: Morningstar Direct

[ii] “Bonds: Using the Full Toolkit”, AllianceBernstein, page 3

[iii] Data table source: Federal Reserve