Over the past few weeks, it’s been hard to have a conversation with clients without oil coming up. It’s visible, and it moves quickly. And when it does, people feel it almost immediately — at the pump, in the headlines, and in the general tone of the market.

But one of the challenges in moments like this is separating what feels urgent from what is actually shaping the path of the economy over time. I’m not saying oil doesn’t matter; it always has. But it tends to operate in cycles — sharp moves, followed by adjustments, followed by normalization.

What’s been on my mind more lately is something that doesn’t move like that at all. It moves slowly, almost in the background, especially when the headlines take our attention to something as immediate as oil. And yet, over time, it may matter more than any short-term shock we’re watching today.

This is one of those charts that’s easy to look past because it hasn’t changed direction in a long time.

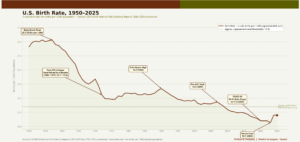

1.

Birth rates in the U.S. have been declining for decades. There isn’t a single moment when it breaks — just a steady drift lower. At this point, we’re well below replacement levels, which means over time, the population isn’t naturally replenishing itself the way it once did. There is nothing dramatic about that on a year-to-year basis. But over longer periods, it changes the underlying math.

Fewer people entering the system, eventually, means fewer workers, fewer households, and fewer consumers. It doesn’t create an immediate slowdown, but it does take away one of the quiet tailwinds which the economy benefited from for a long time.

And unlike most of the things we talk about — rates, inflation, policy — this isn’t something that responds quickly. It simply unfolds.

At the same time, the people who are here are moving through life a bit differently than they used to.

2.

Marriage rates have been gradually declining for decades. It’s ephemeral — just steadily shifting. It’s easy to frame that as purely cultural, and to some extent, it is, but it also carries economic implications that are easy to underestimate.

Household formation has always been one of the more important inflection points in the economy. It’s when spending becomes more committed. Marriage and kids create spending that is more durable and less discretionary.

When that moment happens later, the economy still functions — it just takes longer to fully engage.

There’s a natural inclination to think that modern tools and technology should make these transitions easier. In some ways they do. But they also tend to introduce new forms of complexity. Making something more efficient doesn’t always make it simpler. The dating app is a fitting example of that.

You can see where all of this comes together most clearly in housing.

At first glance, the homeownership rate itself doesn’t look particularly unusual. It hasn’t broken down in a way that would immediately raise concern. But when you look a layer deeper, the shift becomes more apparent.

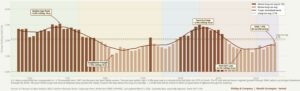

3.

The age of the first-time homebuyer has moved steadily higher and is now approaching 40. That’s a meaningful change — not just statistically, but economically. It represents a delay in when individuals and families step into a more permanent phase of spending and asset ownership.

Part of that shift is preference. There’s a noticeable tendency among younger generations to prioritize flexibility — experiences, mobility, and optionality — before committing to something as fixed as a home. That’s a real change in behavior.

But it would be incomplete to view it only through that lens. Housing has also become more difficult to access. Prices have risen faster than incomes, and interest rates have altered affordability in a very real way. Not to mention supply constraints haven’t kept pace with demand in many markets.

So, while it can look like a choice, in many cases it’s simply a constraint. The desire to own a home hasn’t disappeared; it’s just being deferred.

When you step back and put these pieces together, a pattern starts to emerge: fewer people over time, participating economically later, forming households later, and buying homes later.

This creates a shift in when people move into their most consumption-intensive years. The economy doesn’t stop because of it. It adapts. But the timing changes. Growth becomes more gradual and more dependent on existing wealth, rather than being driven by a steady influx of new participants.

And that brings us back to where the conversation is today —Artificial intelligence.

AI is often discussed in abstract terms, but in practice it’s already working its way into businesses in fairly ordinary ways.

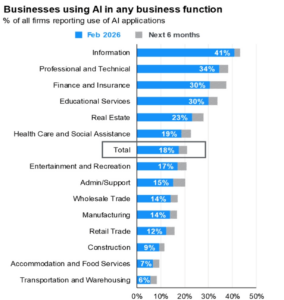

4.

Not everywhere at once, and not evenly, but broadly enough to matter, it’s showing up across industries and functions — sometimes in small efficiencies, sometimes in more meaningful changes to how work gets done. What’s notable isn’t just the level of adoption today, but the direction of travel.

It’s penetrating our economy much quicker than most think, and it’s driving a ton of productivity growth in our macroeconomic system. Yet it’s not creating the mass layoffs the doomsday scenario would suggest.

For a long time, productivity has been the missing piece in the economic story. We’ve had capital, we’ve had demand, but output per worker hasn’t meaningfully accelerated.

5.

That may be starting to shift. It’s still early, and it’s far from consistent, but the trend is worth paying attention to. Productivity is one of the few levers an economy has when it runs into structural limits like fewer people.

Viewed all together, the timing becomes difficult to ignore. At a point when population growth is slowing, when household formation is delayed, and when labor supply is tighter than it might appear on the surface, we’re introducing a set of tools (AI) designed to increase what each individual can produce.

That doesn’t mean that people become irrelevant. It means the value of each unit of labor potentially increases.

It’s also worth being clear about what this doesn’t solve. AI isn’t going to reverse demographic trends. It won’t make housing more affordable overnight. And it won’t simplify the more human aspects of how people build relationships and lives.

We’ve seen enough technological cycles to know that those dynamics tend to persist. But technology doesn’t need to solve everything to matter.

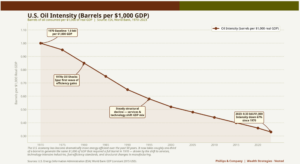

A brief note on oil — Given how much attention energy has been getting, it’s worth putting that in context as well.

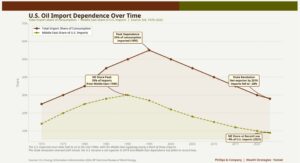

The U.S. today is far less dependent on oil in general than it was in prior decades. Import exposure has declined meaningfully, and reliance on the Middle East is a fraction of what it once was. At the same time, the economy has become more efficient. We use less energy per unit of output than we did in the past — 67% less!

6.

7.

None of that means oil shocks don’t matter. They do. They affect sentiment, and they can influence behavior in the short term. But structurally, they don’t carry the same weight they once did. They tend to pass through the system more quickly, and with less lasting impact.

Where this leaves us:

If the underlying constraint in this cycle is people — not capital — then the way we think about growth needs to adjust. That shifts where the opportunities are as well — not just in the technologies themselves, but in the businesses that find ways to use them effectively.

There’s always something in the market that feels immediate. Right now, that’s oil.

But the more durable changes tend to happen more quietly.

- Fewer people.

- Later starts.

- Different shape of the economic cycle.

And alongside it, a set of tools (AI) arriving at a moment when they may be needed more than we realize.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

1. CDC/NCHS National Vital Statistics Reports for U.S. birth rates (1950–2025) and 2. marriage rates (1900–2023), 3. the U.S. Census Bureau for homeownership data, 4. and the National Association of Realtors (NAR) Profile of Home Buyers & Sellers for first-time buyer age; 5. AI adoption data from J.P. Morgan Asset Management’s Guide to the Markets (drawing on U.S. Census Bureau Business Trends & Outlook Survey, KPMG AI Pulse Survey, and RAMP AI Index) ; 6. productivity data from the U.S. Bureau of Labor Statistics (BLS); 7. and energy data from the U.S. Energy Information Administration (EIA) and Bureau of Economic Analysis (BEA) for oil import dependence and oil intensity. Data reflects the most recent available information as of early 2026.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.