When fear shows up, it rarely knocks politely. It barges in through the headlines, raises its voice, and tells us that whatever is happening right now will probably get worse before it gets better. That is where we are again. The failed Iran peace talks, blockades, and threats of more military conflict have put oil and gas prices back in focus, and whenever energy prices jump, it is easy to jump straight to the conclusion that the consumer is about to fold and the market will have no choice but to follow.

That is the emotional case. Markets, however, often work through more complicated logic. One of the more counterintuitive truths in investing is that fear can set the stage for better forward returns, not because the underlying concern is imaginary, but because investors tend to price in fear faster than the economy can absorb the damage.

That is what makes elevated volatility so interesting. Historically, when fear has been high and the volatility index has started from elevated levels, forward six-month S&P 500 returns have often been better than when investors were calm and complacent. At current levels, that might suggest forward six-month returns could be more than 9%.

That does not mean every spike in fear is a buying opportunity on cue, and it certainly does not mean risk disappears. It simply means that by the time people are most worried, expectations have often already adjusted. Fear changes the price you pay long before it changes the long term value of what you own.

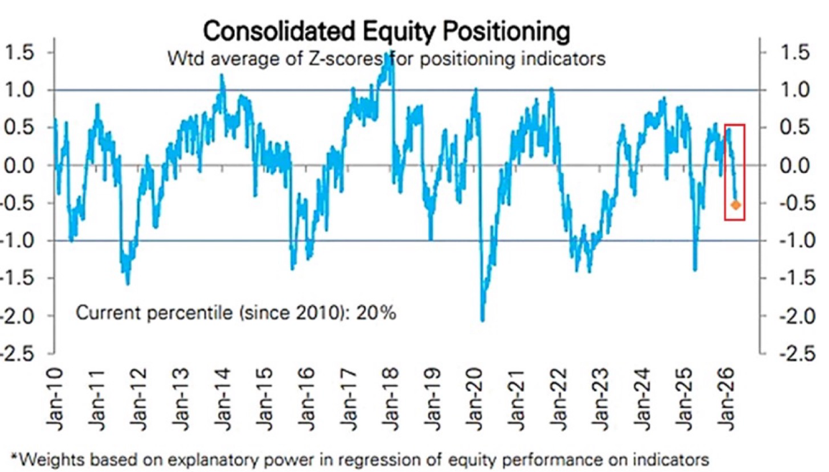

That point becomes even more relevant when you look at how investors are positioned today. We are not looking at a market that is wildly over-owned by enthusiastic bulls. If anything, the opposite is true.

Deutsche Bank’s consolidated equity positioning work shows current positioning at around the 20th percentile since 2010. In plain terms, there is still a fair amount of caution in the system. That matters because markets do not need universal optimism to rally. They just need conditions that are a little less bad than feared. When investors are underexposed and incoming data holds together, some of that sidelined capital tends to work its way back into equities. A rally can be fueled just as much by skepticism softening as by outright enthusiasm.

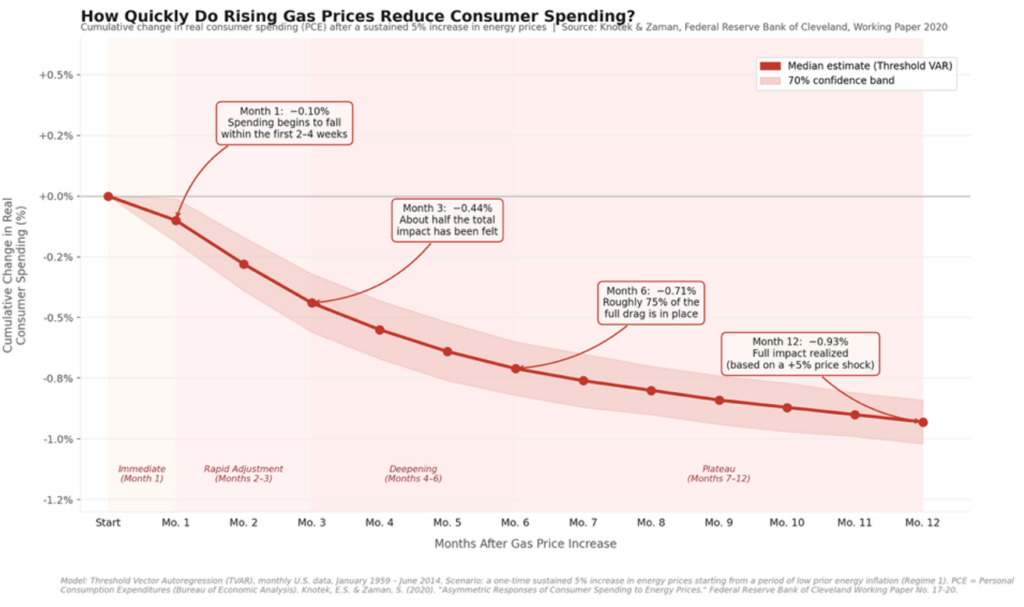

Of course, the energy concern is real. Higher gas prices matter. They act like a tax on households, particularly for people with longer commutes or tighter budgets. But even here, it helps to slow down and look at the timing rather than just the headline.

The drag from higher gas prices tends to show up in phases, not all at once. The initial adjustment starts quickly, within the first few weeks, but the full effect builds over months. By month three, a meaningful share of the drag has taken hold. By month six, most of it is in place. By month twelve, the effect is more fully realized. That is a very different picture from the idea that one geopolitical flare-up instantly causes consumers to slam on the brakes.

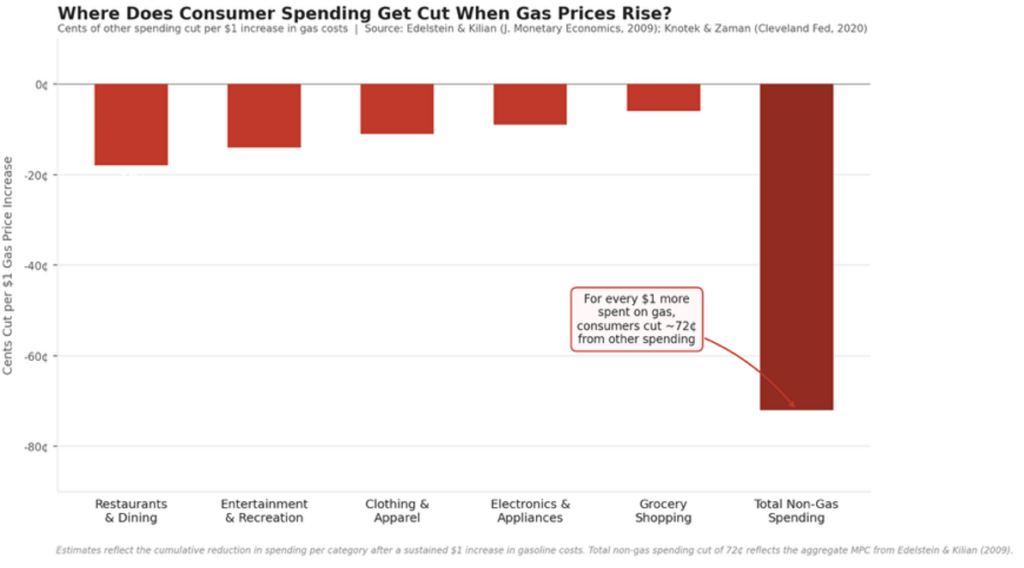

And just as importantly, the pressure is unevenly spread across the economy.

When consumers must absorb more at the pump, they usually do not cut everything equally. The first places to feel it tend to be the more discretionary parts of the budget: restaurants, entertainment, apparel, and other purchases that can be postponed. Grocery spending tends to hold up better. Essentials tend to hold up better. So, when energy spikes, the story is usually not, “all spending collapses.” It is more often, “some categories feel it first, and others hold in better than people expect.”

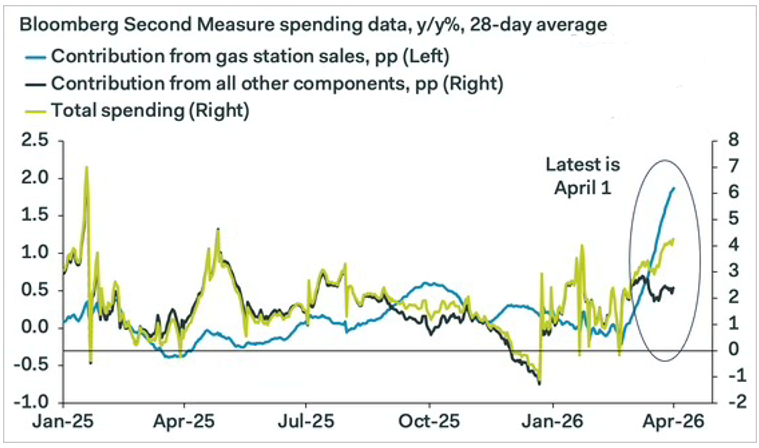

That distinction matters because the real time spending data still looks more resilient than consumer sentiment.

Bloomberg’s second measure of spending still shows overall spending still expanding. Gas station sales are clearly a factor, but spending from the rest of the consumer basket is still positive. That does not look like an economy in immediate retreat.

If that were the whole story, it would already be enough to push back against the most bearish interpretation of current events. But there is another leg that matters just as much. Earnings.

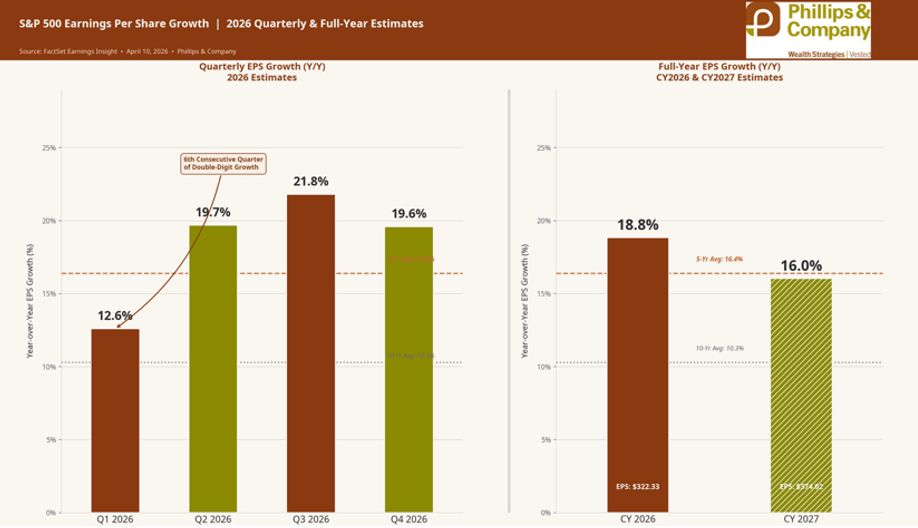

The earnings outlook remains strong. FactSet’s current estimates show quarterly S&P 500 earnings growth at very strong levels throughout each quarter in 2026. Full- year 2026 EPS growth is estimated at nearly 19% and 2027 EPS growth is estimated at 16%. That growth is remarkable. They do not eliminate risk, and they do not guarantee that every company will deliver, but they do remind us that the corporate backdrop remains much better than the emotional tone of the market would suggest.

That is often how these periods feel from the inside. The macro narrative is loud. War risk, oil, inflation worries, and policy uncertainty all compete for attention. But underneath that noise, businesses continue to report, margins get managed, capital gets deployed, and earnings keep compounding. Markets eventually must reconcile those two narratives. When positioning is cautious and earnings are still growing, the path of least resistance can be better than people think.

That brings us to the next important turn in the story. Reporting season starts this week.

As earnings season gets underway, the market will start shifting from theoretical macro fears to actual company results and guidance. The early calendar gives us the usual read from the financials, along with some important signals from industrial, consumer, and technology-linked names. This is where investors move from imagining what might happen to reacting to what management teams are seeing.

That does not mean the Iran conflict or gas prices stop mattering. They do. But markets have a way of recentering around earnings once the reporting season begins. If results and guidance hold up well, a market that is still under-owned has room to absorb better news. And if the consumer continues to bend rather than break, some of the fear that has been holding investors back may start turning into demand for equities again.

Could all this fear and under-positioning set the stage for another wall-of-worry rally as earnings kick off?

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

1. FactSet Earnings Insight (April 10, 2026)

2. Bloomberg Second Measure spending data (latest reading April 1, 2026)

3. Deutsche Bank Asset Allocation

4. Federal Reserve Bank of Cleveland

5. Edelstein & Kilian (2009)

6. Earnings Whispers

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.