For most of this cycle, the U.S. economy has been carried by the consumer. People complained about inflation, worried about rates, grumbled about the price of groceries, and then kept spending anyway. That is the odd resilience of the last few years. The consumer does not feel great, but the register keeps ringing.

Now the story is starting to shift based on a look at the latest GDP report.

The economy is not moving away from the consumer, but the next leg of growth looks more dependent on business investment: not financial investment like stocks and bonds, but physical investments like data centers, chips, power equipment, cooling systems, transmission lines, construction labor, and the infrastructure needed to make artificial intelligence useful outside of a demo.

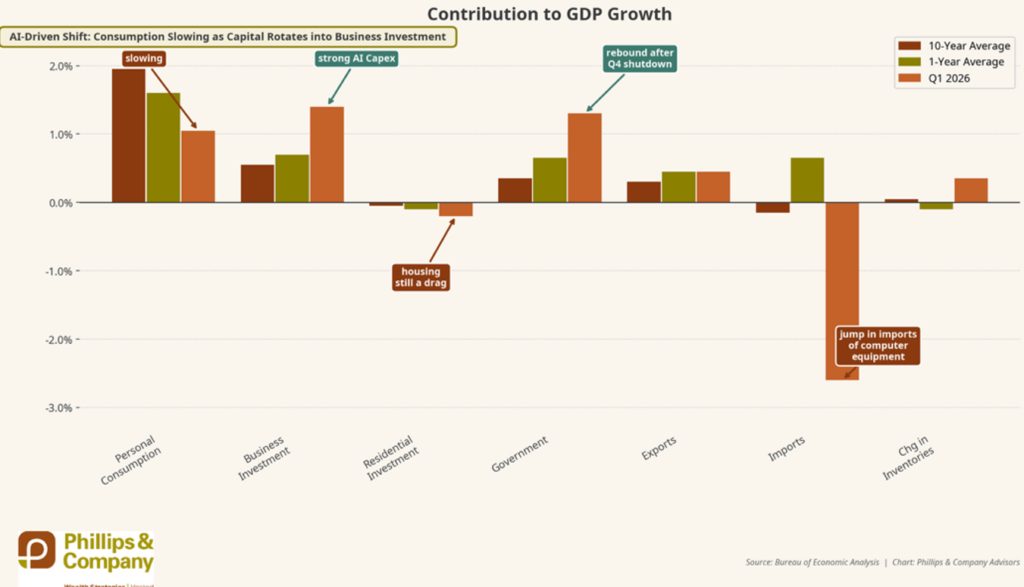

The handoff is already showing up in the GDP data. Personal consumption is still contributing to growth, but the contribution has slowed from roughly 2% over the 10-year average to closer to 1% in Q1 2026. Business investment, meanwhile, has moved the other way, rising from roughly 0.5% over the 10-year average to around 1.4% in Q1. Residential investment is still a drag, imports are a major negative because of computer equipment demand, and government spending rebounded after the Q4 shutdown noise.

The shopping cart has not stopped, but the server rack is becoming more important. In fact, without that investment contribution, we might be close to no growth at all.

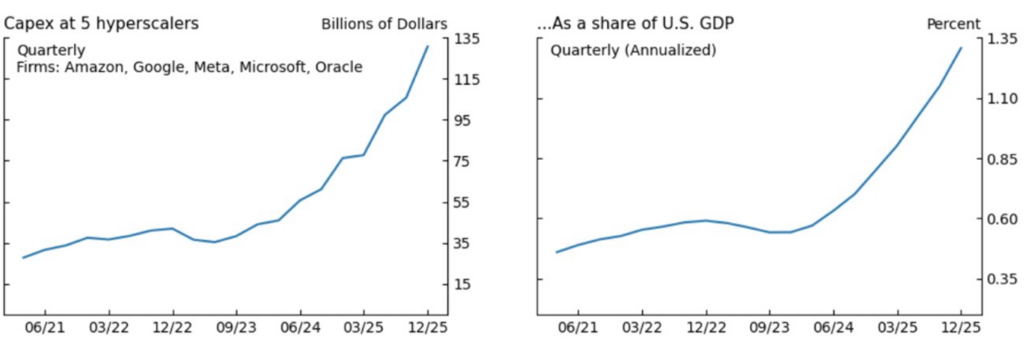

The spending behind this shift is hard to ignore. Five companies — Amazon, Google, Meta, Microsoft, and Oracle — have pushed quarterly capex from roughly $30 billion in 2021 to more than $130 billion by late 2025. As a share of GDP, that spending has climbed from around 0.5% to roughly 1.3%.

That is no longer just a tech sector story. At that size, it becomes a macroeconomic story that has major implications.

This is also why markets keep coming back to AI even when the headlines sound excessive. The spending is real. The demand for chips, power, construction, land, cooling, and cloud capacity is real. What we do not know yet is how much of this spending turns into durable productivity and how much turns into the usual overbuilding that comes with every major capital cycle.

Probably some of both.

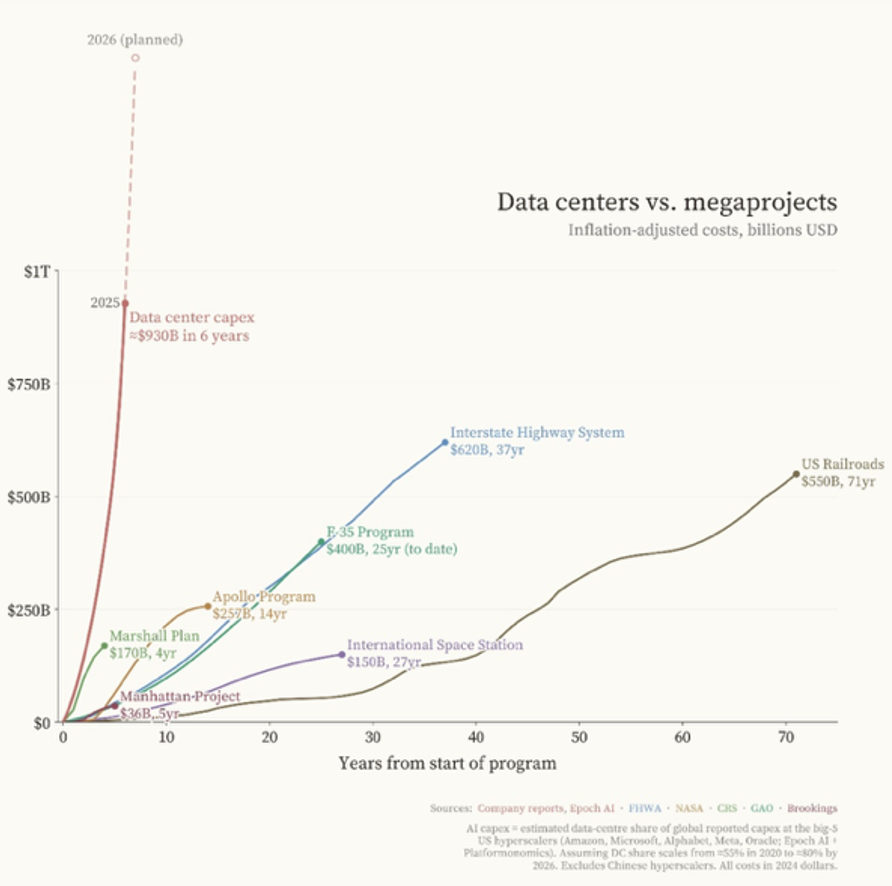

The scale is what makes this period unusual. Data center capex is approaching $930 billion over six years, with 2026 planned spending pushing toward the $1 trillion mark. For context, that compares with the interstate highway system at roughly $620 billion over 37 years and the U.S. railroad buildout at about $550 billion over 71 years.

Those comparisons are imperfect, but they are useful. Big technology shifts rarely stay digital. They eventually require steel, concrete, power, logistics, and a lot of permitting meetings that no one puts in the investor presentation.

That is where the enthusiasm meets the dirt.

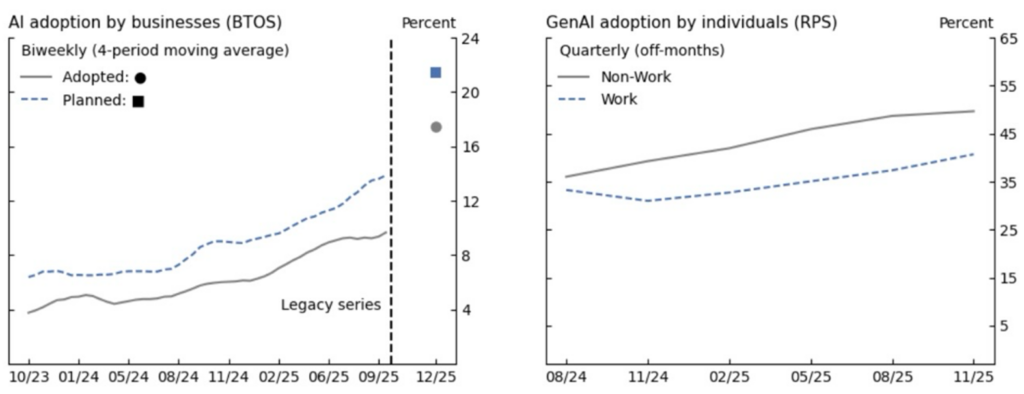

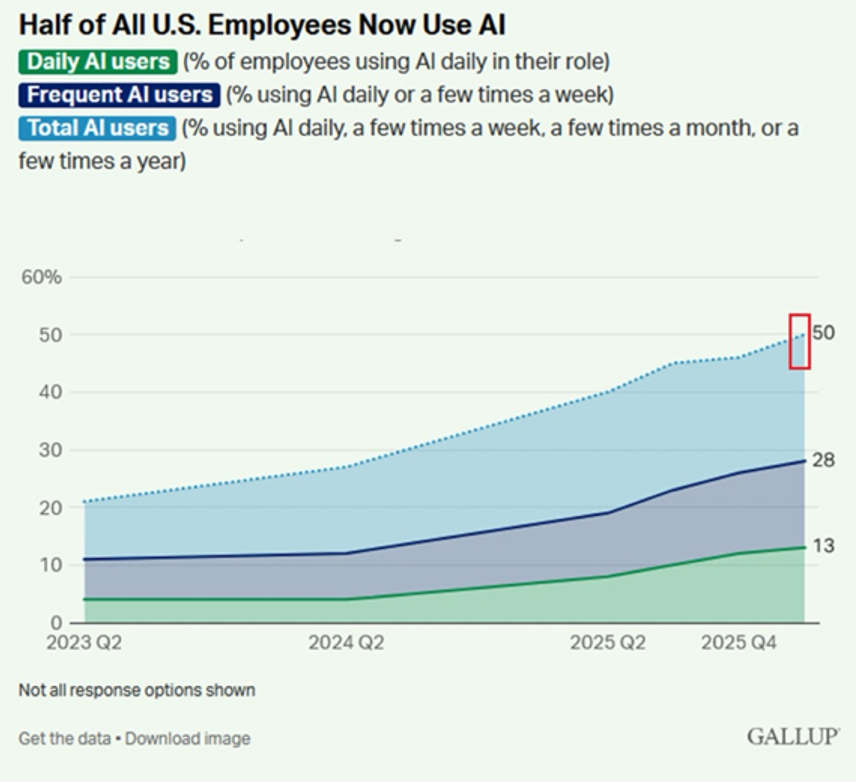

The reason the spending may be justified is that adoption is no longer theoretical. Business AI adoption has moved steadily higher since 2023 according to a recent Federal Reserve study. And planned adoption is running ahead of actual adoption. On the individual side, non-work usage is nearing 50%, while work usage has moved into the low-40% range.

Gallup shows the same direction from a different angle. About half of U.S. employees now use AI at least occasionally. Roughly 28% are frequent users, and about 13% use it daily.

That matters because technologies usually become economically important before they are perfectly measured. A worker using AI to summarize documents, write code, analyze data, answer client questions, or speed up internal workflows may not immediately show up in GDP statistics. But enough small improvements, spread across enough workers, eventually start to matter.

The key word is eventually.

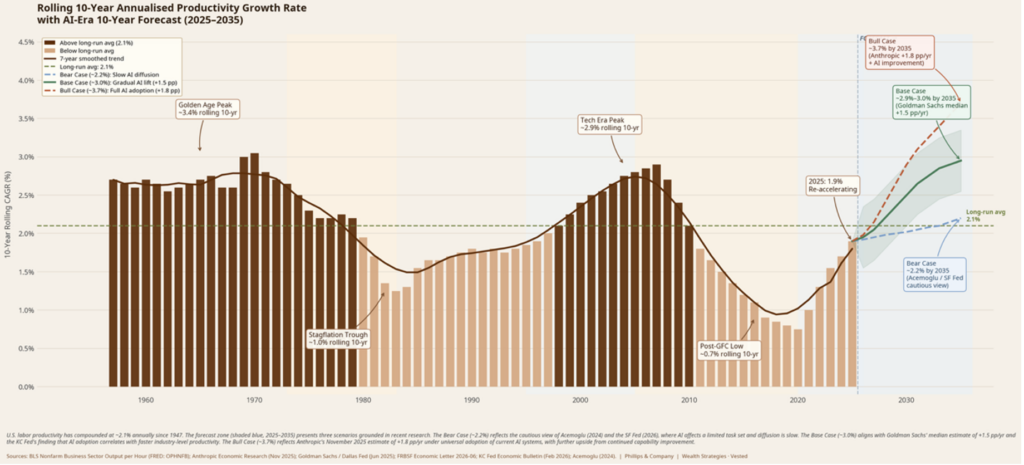

Productivity is the prize, but it is also the part we should be careful not to oversell. Long-run U.S. productivity growth has been about 2.1%. The post-financial-crisis period was weak, bottoming near 0.7% on a rolling 10-year basis. The tech era helped, but it took time. Even the earlier Golden Age peak was a long process, not a quarterly event.

The AI scenarios show a wide range. The cautious case gets productivity only slightly above trend by 2035. The base case moves closer to 3%. The bullish case gets into the high-3% range. That range is the honest answer. AI could lift the economy’s speed limit, but the path from tool adoption to national productivity is never clean.

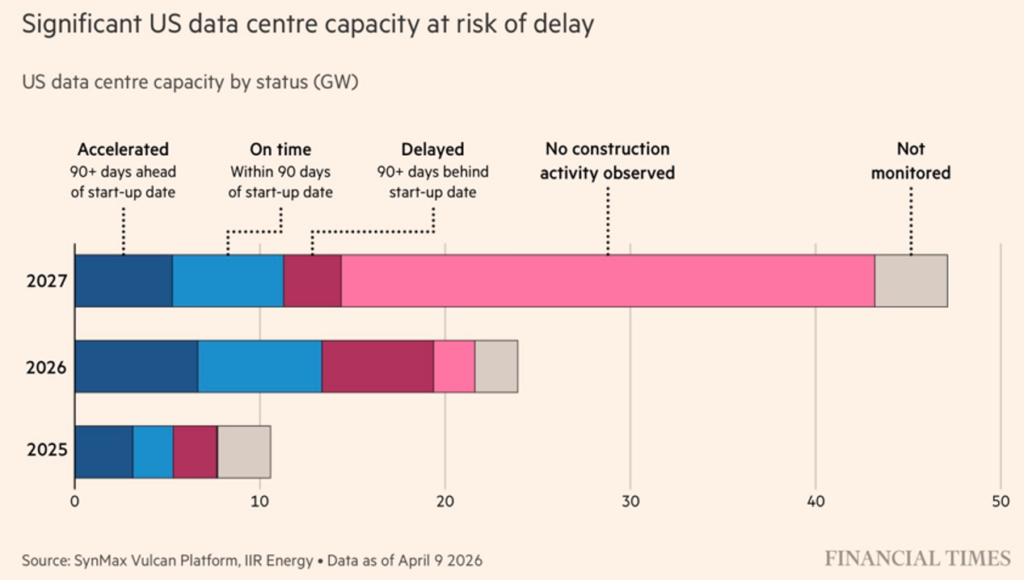

The bottlenecks are already visible. A meaningful amount of planned U.S. data center capacity for 2026 and 2027 is delayed, not yet under construction, or not fully monitored. Power availability is becoming a gating item. So are transformers, interconnection queues, cooling systems, land, labor, water concerns, and local approval.

This is the part of the AI story that gets less attention because it is not as exciting as a new model release. But it may matter more. Software can scale quickly. Power plants, substations, and transmission lines do not.

That is the tension of the moment. AI adoption is moving like software. AI infrastructure is moving like construction. The market wants to know whether all this spending becomes a productivity boom. The economy first must answer a simpler question: can we actually build it? This is what I will be keenly watching in the coming years.

That is why this shift from shopping centers to data centers is so important. A consumption-led economy depends on household income, confidence, credit, and the willingness to spend. An investment-led economy depends on planning, permits, supply chains, financing, and execution. One is driven by millions of daily decisions at the cash register. The other is driven by large capital commitments that take years to complete.

The consumer still matters. They always do. But the marginal driver of growth is changing. The next phase of the economy may be less about how much people are willing to buy and more about how much companies are willing and able to build.

For investors, that means the AI story should be treated less like a theme and more like a capital cycle. Capital cycles create winners, excesses, bottlenecks, and delays. They also create infrastructure that later feels obvious. We are probably building some excess. We are probably also building something useful.

That is usually how these periods work. The spending comes first, the skepticism comes with it, the bottlenecks slow it down, and the productivity shows up later than promised.

From shopping centers to data centers may not be a straight line. But it is becoming one of the more important handoffs in the economy.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

References: Bureau of Economic Analysis GDP contribution data; Bureau of Labor Statistics nonfarm business productivity data via FRED; Federal Reserve research on AI adoption by businesses and individuals; Gallup workplace AI usage survey; company-reported capital expenditure data for Amazon, Alphabet/Google, Meta, Microsoft, and Oracle; Financial Times analysis of U.S. data center capacity delays using SynMax Vulcan Platform and IIR Energy data as of April 9, 2026; Epoch AI and company reports on data center capex compared with historical megaprojects; Phillips & Company Advisors analysis.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.