Economic expansions are strange because investors expect them to feel obvious while they’re happening, and they usually feel fragile.

There are always reasons to be cautious. Oil prices, interest rates, and political headlines create uncertainty. Economists debate recession probabilities on television as if downturns arrive on scheduled calendars. Yet underneath all that noise, the actual economic data often tells a far steadier story.

I think that’s where we are today.

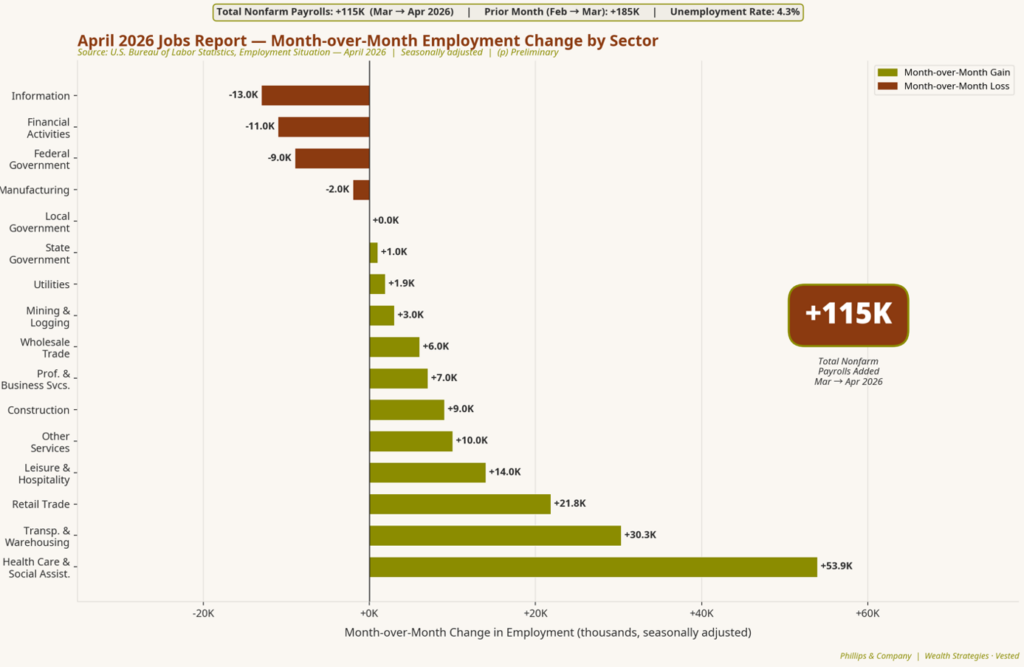

The latest jobs report showed the U.S. economy continuing to add jobs while unemployment remains historically low. The overall economy added 115,000 jobs in April across a host of private sectors.

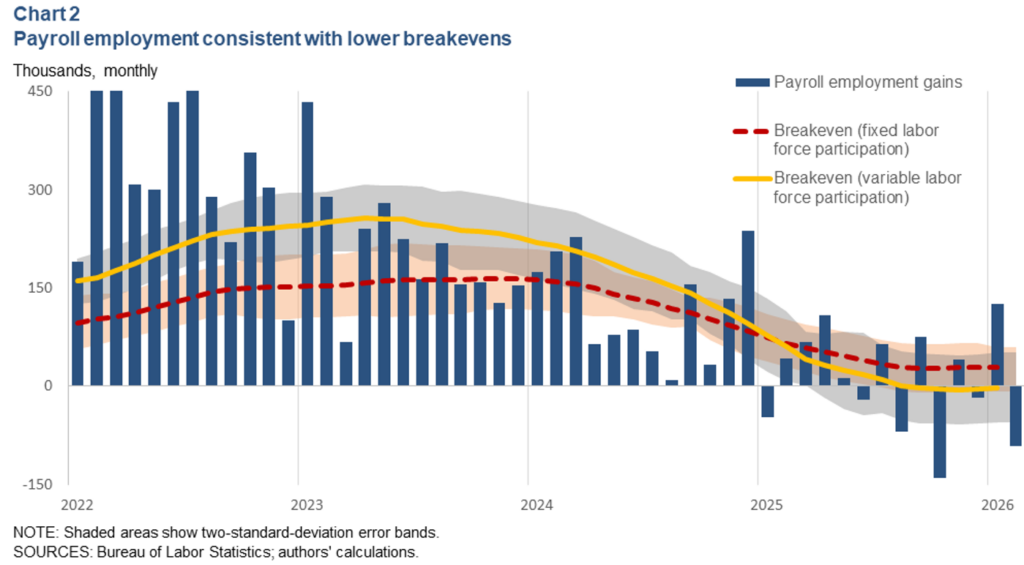

For years, investors became conditioned to believe the economy needed monthly payroll growth north of 150,000 to remain healthy. But demographics, slower labor-force growth, immigration shifts, and an aging workforce have all changed the equation. According to recent Dallas Fed research, the current breakeven level for payroll growth may now sit closer to 50,000 jobs per month depending on participation assumptions.

In other words, the economy no longer needs 250,000 monthly job reports to remain stable. It simply needs enough growth to keep the labor market intact. And so far, that is exactly what we continue to see.

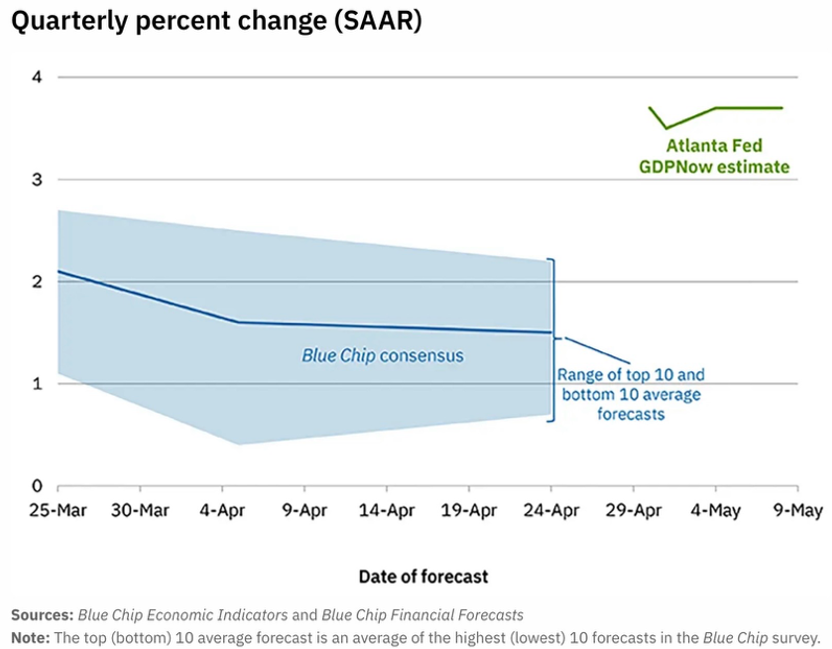

At the same time, the Atlanta Fed GDPNow model is currently tracking second quarter GDP growth near 4%, a level that points toward continued economic expansion rather than contraction.

What matters about GDP growth today is not just the level itself, but what is driving it. This cycle increasingly appears to be transitioning toward investment-led growth. Corporate America is spending aggressively on AI infrastructure, data centers, energy systems, electrical upgrades, semiconductor capacity, logistics, and automation. See last week’s blog.

Those investments do not always create immediate headlines, but they tend to create long-duration economic productivity and ultimately, productivity is what sustains earnings growth.

In the meantime, corporate earnings matter a lot.

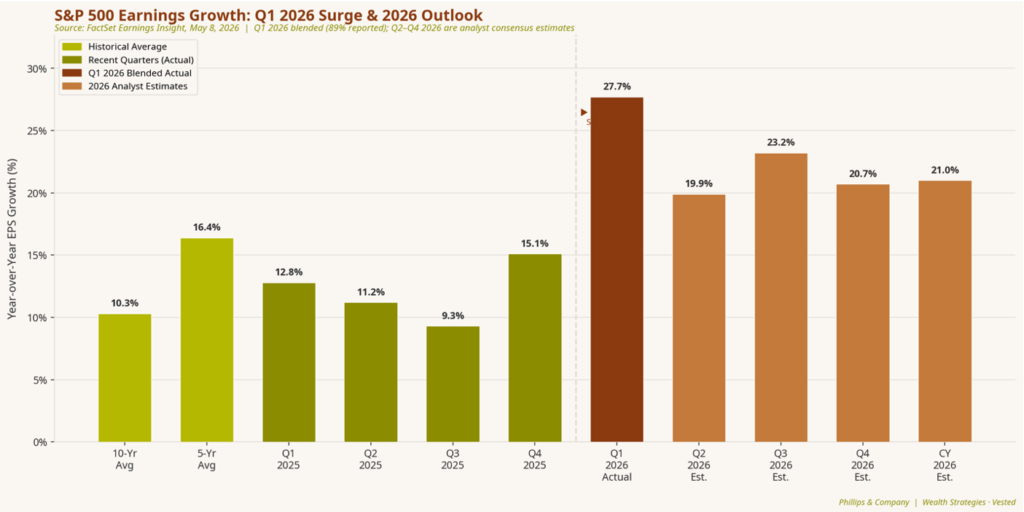

Q1 2026 S&P 500 earnings growth came in at 27.7%, dramatically above both the 5-year and 10-year historical averages. Analysts still expect earnings growth above 20% for the full year.

These are massive expansion-level earnings numbers. Just look at the 10-year average on the far left compared to Q1 2026. Wow!!!

There’s an old story about a man who watched workers build a cathedral. He asked three different stonecutters what they were doing.

The first said he was laying bricks.

The second said he was earning a paycheck.

The third said he was building something that would outlive him.

All three were technically correct. But only one understood the long-term significance of the work.

Markets function similarly.

In the short run, investors tend to focus on daily headlines, Fed commentary, elections, tariffs, or geopolitical shocks. But over longer periods, markets are largely shaped by the slow construction of earnings power underneath the economy. That process rarely looks exciting in real time.

It looks like factories being built. Software being deployed. Infrastructure being upgraded. Productivity improving one percentage point at a time.

But over years, those small gains compound into meaningful economic growth. And markets tend to follow earnings growth far more closely than they follow headlines. The challenge for investors is that markets do not reward patience in smooth, predictable increments.

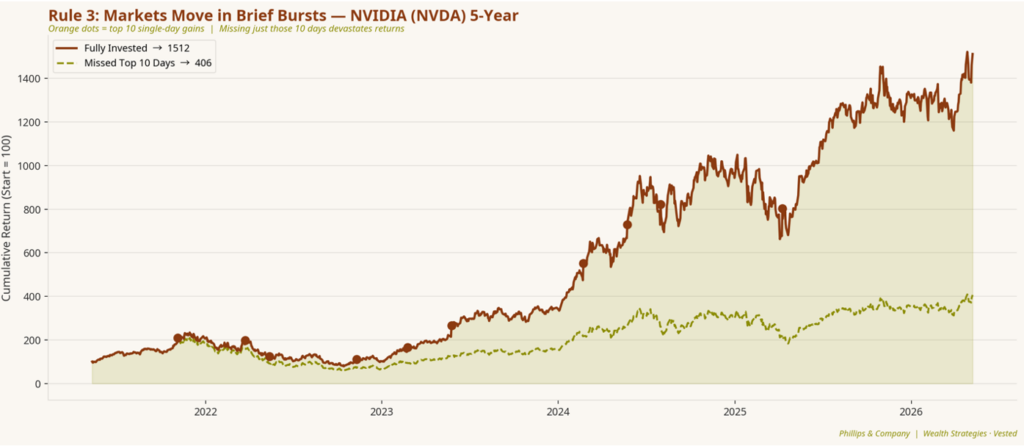

They reward it violently and all at once. Markets move in brief bursts, and if you miss just a few days you lose a lot of the advantage. Just look at NVIDIA returns (green line) if you missed just 10 days in 5 years.

A famous poker story tells of a player who folded hand after hand for hours waiting for the perfect opportunity. Someone at the table eventually asked how he tolerated the boredom.

He responded, “Because the money isn’t made playing every hand. It’s made staying at the table long enough for the odds to matter.”

Investing works much the same way. Long-term returns are often driven by a surprisingly small number of trading days. Miss those days and the mathematics of compounding change dramatically.

The problem is that many of those best days occur during periods that feel deeply uncomfortable. Markets tend to recover before economic certainty arrives. They reprice future growth quickly, unpredictably, and often when investors least expect it.

That reality creates one of the hardest emotional challenges in investing:

The moments that feel safest are often not the moments that produce the best long-term returns.

Time itself is what eventually resolves much of that uncertainty.

There’s another old story about a farmer who planted apple trees knowing they would not fully mature for years. When asked why he bothered, he simply said, “Because eventually time does most of the work for you.”

Long-term investing is remarkably similar.

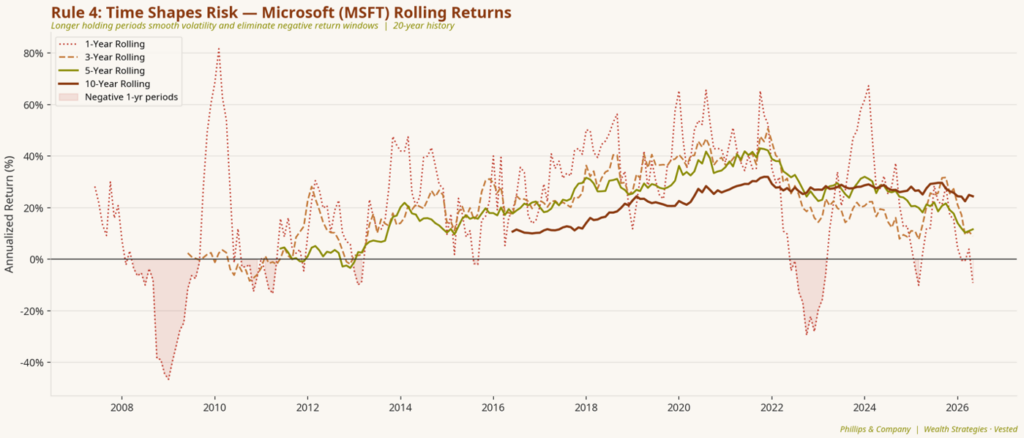

Over one-year periods, markets can appear chaotic and random. Returns swing sharply. Volatility dominates the experience. Fear and optimism alternate constantly. But as holding periods extend, something important begins to happen: Time starts overwhelming noise.

The short-term volatility that once felt enormous gradually matters less as earnings growth, innovation, productivity, and compounding begin doing the heavy lifting. Microsoft is a great example. 1-year rolling returns look volatile, but 5-year and 10-year rolling returns are all positive.

And that may be the most important investing lesson in today’s environment.

The economy continues to grow. Employment growth remains above breakeven levels. Corporate earnings continue to be surprisingly higher. Businesses continue investing aggressively into future productivity.

Yet many investors remain hesitant because uncertainty still surrounds the headlines. But uncertainty is not an abnormal condition for markets. It is the permanent condition.

The investors who tend to struggle most are often the ones waiting for the moment when everything finally feels clear.

Historically, that moment rarely arrives before the market has already moved.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

FactSet Earnings Insight, May 2026; Bureau of Labor Statistics Employment Situation Report; Federal Reserve Bank of Dallas; Atlanta Fed GDPNow; Phillips & Company analysis and charts.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.