A few days ago, I was standing in line at a convenience store somewhere in rural Oregon. The guy in front of me bought gas, a sports drink, beef jerky, and a can of ZYNs. The cashier read him the total and he paused for a second, looked down, and quietly put the beef jerky back.

Five minutes later, I passed a brand-new lifted pickup truck pulling into the parking lot next door.

That’s the economy right now. One consumer is still making choices. The other is making trade-offs. And the strange part is that both can exist at the same time while economic growth still looks reasonably healthy on paper.

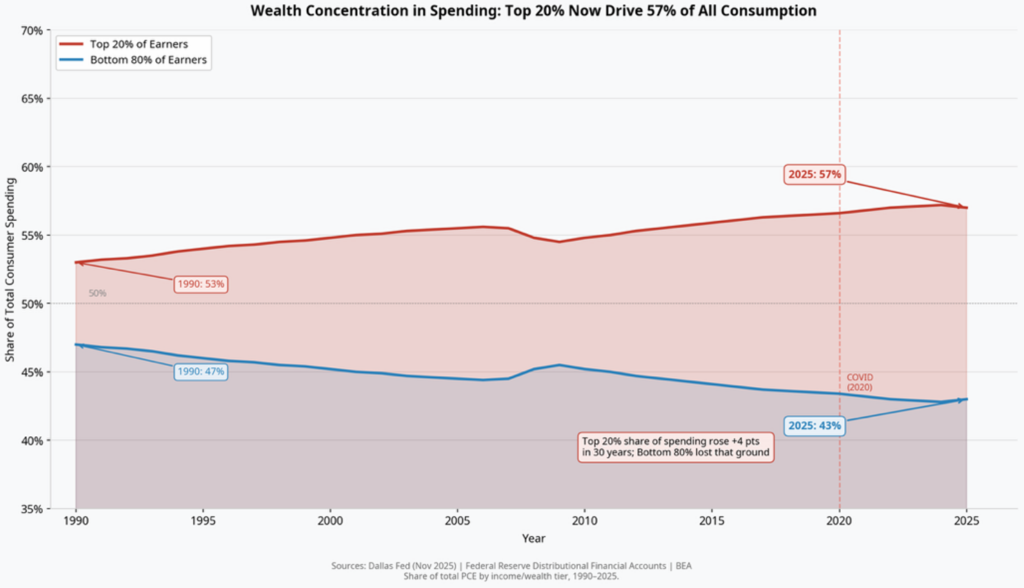

The top 20% of earners now account for roughly 57% of all consumer spending in the United States. That shift over time represents trillions of dollars of purchasing power moving toward a smaller share of households.

If you own assets in America, the last decade has generally treated you well. Your stocks and 401(k) rose along with your home value. Private businesses appreciated, and cash finally earns something again.

Inflation is irritating when you have assets; it’s downright destabilizing when you don’t. That distinction matters more than most headline economic data right now.

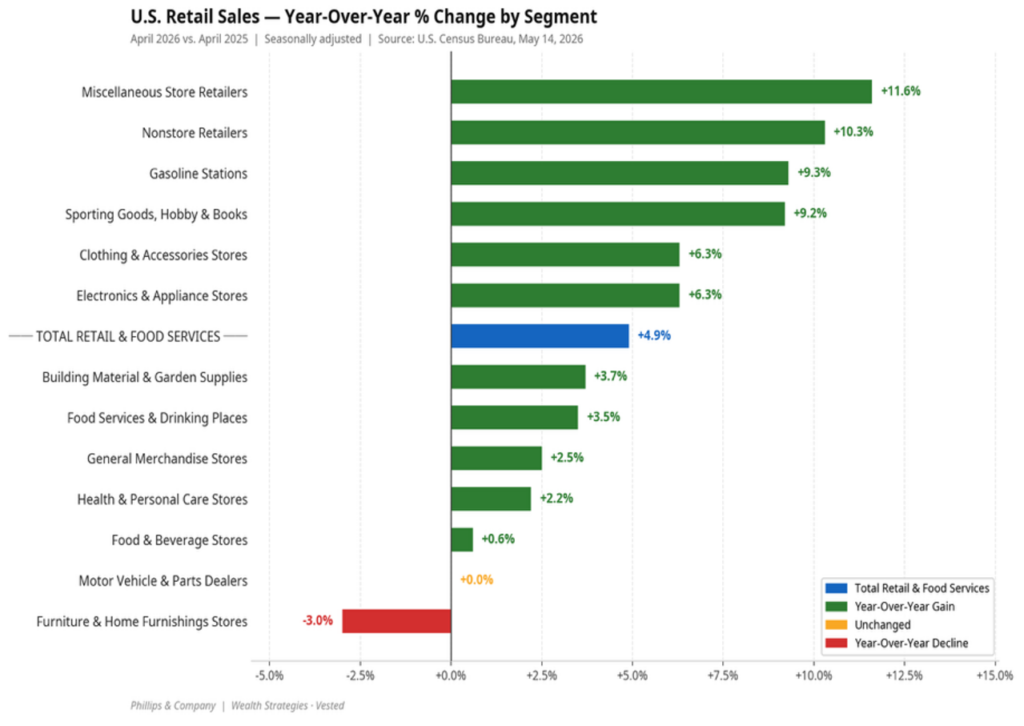

You can actually see this split inside the retail sales data just released by the government.

Higher-end discretionary categories continue holding up surprisingly well. Online retail remains strong. Sporting goods and specialty retail are healthy. Travel-related spending has remained resilient for much longer than most economists expected.

At the same time, lower-end consumers are becoming increasingly selective. Furniture sales are weak and auto affordability is strained. Basic necessities are eating up a larger percentage of household income. Consumers are still spending, just spending differently depending on which side of the balance sheet they live on.

And corporate America has adapted beautifully to that reality.

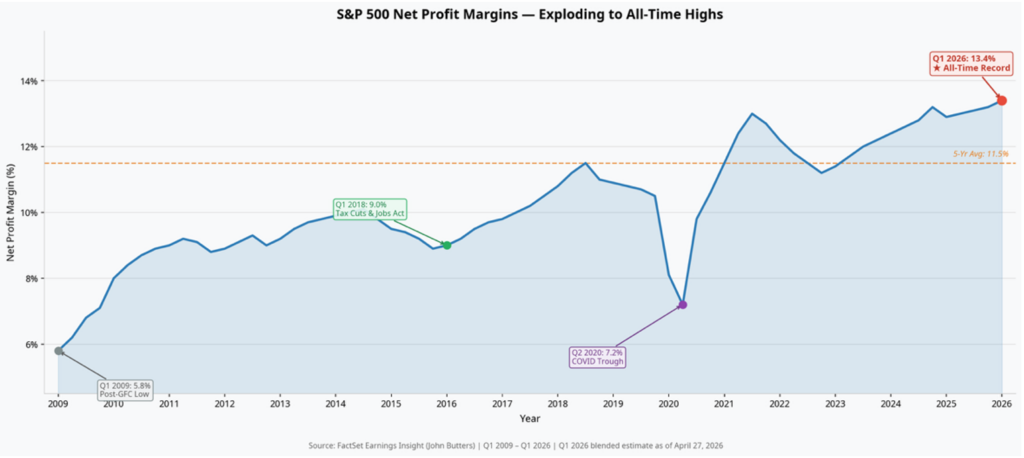

One of the most remarkable stories of the last several years has been the persistence of corporate profit margins.

Normally inflation creates pressure on businesses. Costs rise faster than revenues and margins compress. Companies struggle to pass everything through.

Instead, many large companies discovered they had far more pricing power than expected. Some of that was legitimate cost recovery, and a lot of it was simply learning that higher-income consumers would tolerate higher prices if everyone raised prices together.

If the upper-end consumer kept paying, companies kept expanding margins. We now sit near record corporate profitability despite years of inflation, higher labor costs, and higher interest rates. Companies have tremendous pricing power, and that’s driving equity prices higher and also driving more wealth and more consumption.

But pricing power eventually collides with consumer fatigue. The question is when, and that’s what we have to watch. I’m looking at a few early indicators.

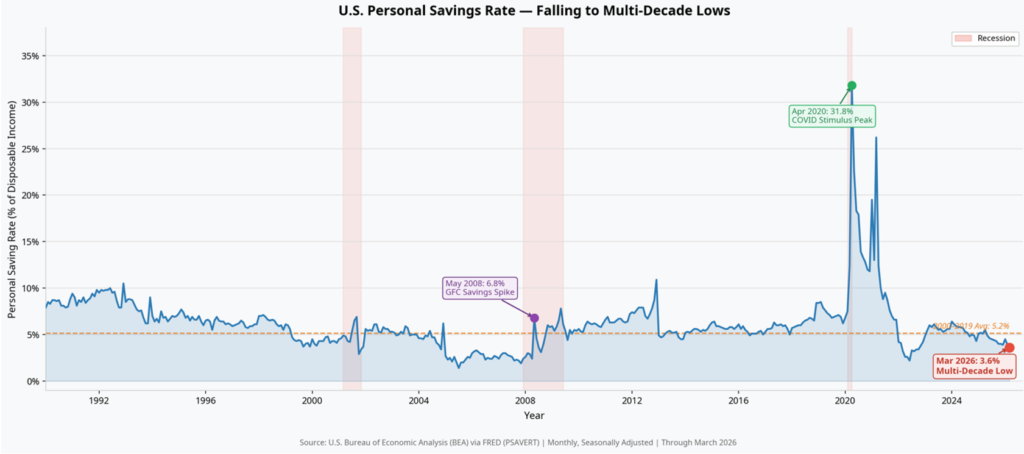

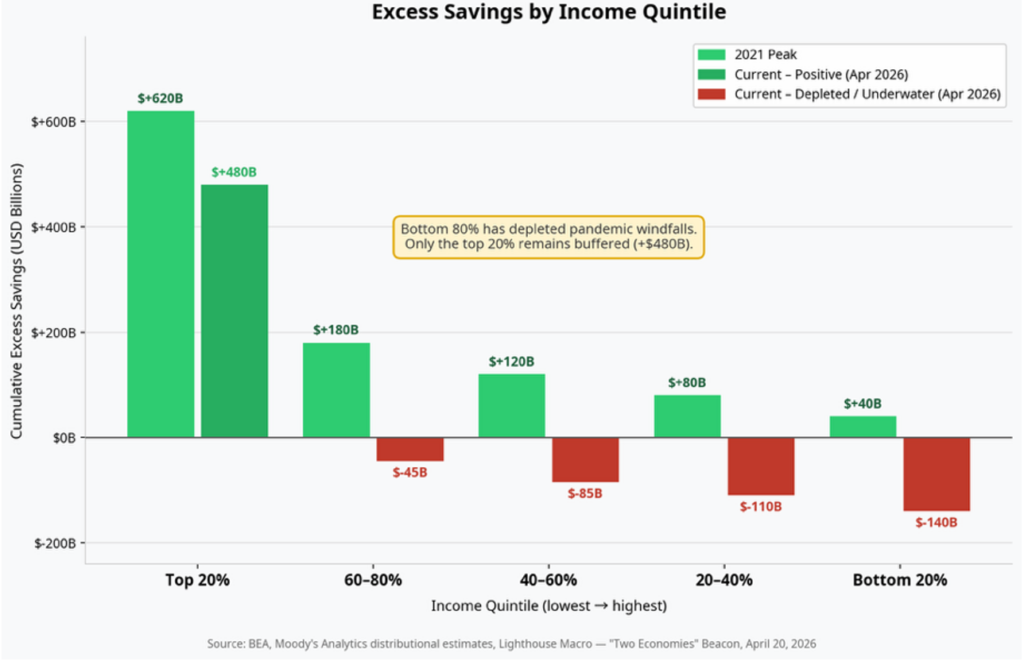

The personal savings rate has now fallen back toward multi-decade lows. However, it’s again a tale of two consumers. Among the top 20% of income earners, savings have held up, while the rest of the income cohorts have spent down their savings.

That statistic matters because savings are what absorb economic stress before credit does. Once savings disappear, households start borrowing to maintain the same lifestyle.

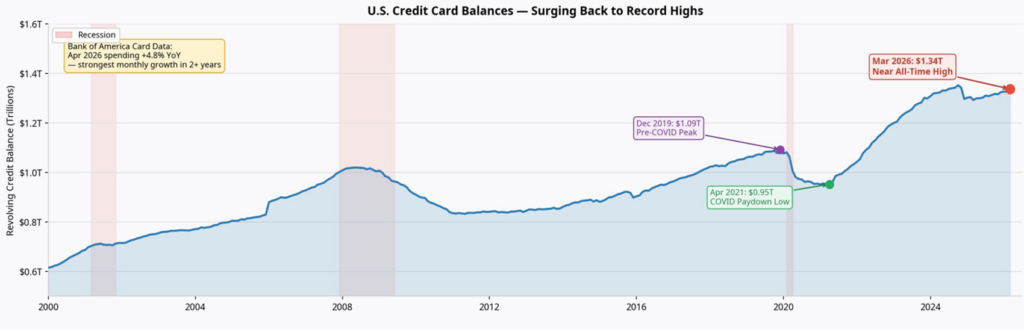

Which is exactly what we’re seeing now.

Credit card balances are near record highs again, probably driven by the mix of consumption we saw in the earlier retail sales chart. More is being spent on gas and groceries.

Nobody wakes up one morning and decides to finance groceries at 22% interest because they feel financially liberated. They do it because monthly cash flow stopped stretching as far as it used to. Think about my beef jerky guy.

The top end of the consumer base can still carry the economy for a while. In fact, they probably are right now.

That’s why parts of the economy still feel remarkably strong despite so much public frustration about affordability.

Both things are true simultaneously. The upper end still has spending power. The lower end increasingly has monthly payment fatigue.

That creates an economy where aggregate spending can still look healthy even while financial stress underneath the surface keeps building.

It reminds me a bit of owning my older commercial building that houses Phillips and Company.

At first, deferred maintenance barely shows up. The lobby still looks fine.

But underneath the surface, little things slowly start stacking up. HVAC systems strain. Roof leaks get ignored. Deferred repairs compound quietly for years, until suddenly the entire building needs far more work than anybody expected.

Consumer stress often works the same way. It accumulates slowly… and then all at once.

That doesn’t mean recession is around the corner. I don’t think the data says that today. Employment is still decent. Higher-income balance sheets remain healthy. Corporate earnings are strong.

But it does suggest we’re probably approaching a point where the lower-end consumer is going to need some relief. Perhaps in this order: Energy prices need to come down, mortgage rates need to come down, and food prices need to stabilize.

Economically and politically, it becomes harder to run an economy where one group absorbs higher prices comfortably while another increasingly finances basic consumption on revolving credit.

There will be changes to the consumption mix and political landscape. That happens when we have these supply shocks. The real winner is the corporate titans that have expanded margins and figured out that the upper-bound consumer is not as price sensitive… yet!

For now, the economy keeps moving because the upper end still has capacity and they don’t have to decide to put the beef jerky back.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

Data sourced from the U.S. Census Bureau, Bureau of Economic Analysis (BEA), Federal Reserve, Federal Reserve Distributional Financial Accounts, FactSet, Moody’s Analytics, Bank of America Institute, Minneapolis Federal Reserve, Dallas Federal Reserve, and Bloomberg, as of May 2026.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.