There is a strange split in the economy right now.

Consumers say they feel terrible as sentiment is scraping along near historic lows. If you just looked at survey data, you would assume the economy was already rolling over and the stock market should be struggling.

But that is not what is happening.

People may feel lousy, but they are still spending. And that spending is feeding into revenue, margins, and, ultimately, earnings. That is the part of the story the market seems to understand better than the headlines do.

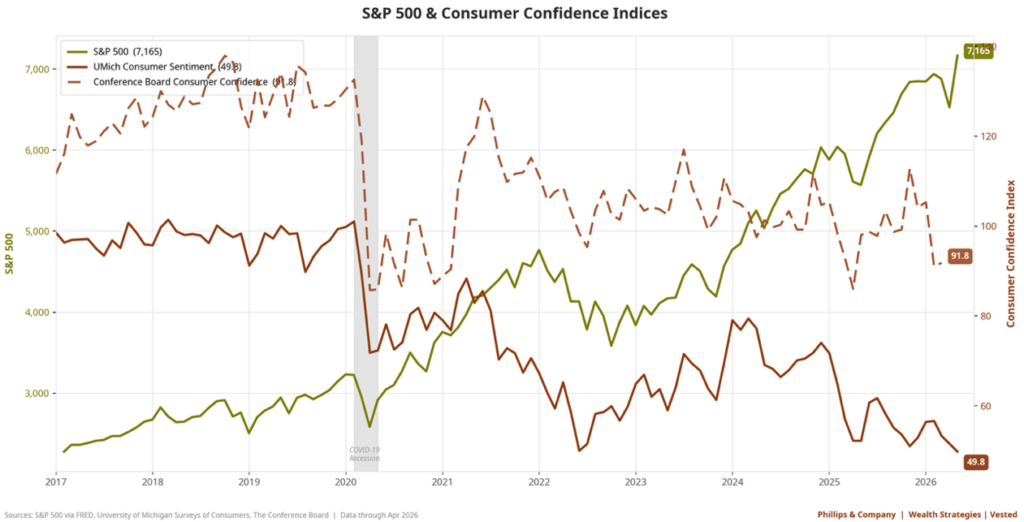

This is the paradox in one picture. Consumer sentiment is sitting near an all-time low, while the S&P 500 is at an all-time high. At first glance, that looks irrational. But it is really a reminder that feelings and behavior are not the same thing. Consumers can be frustrated by prices, worried about geopolitics, and irritated by day-to-day costs, while still showing up at restaurants, taking trips, and making purchases.

That is not as contradictory as it sounds. People answer sentiment surveys based on how they feel about inflation, politics, and uncertainty. They spend based on their paycheck, their balance sheet, their tax refund, and whether they still think they can afford what they want. Right now, the mood is sour, but the spending has held together much better than the mood would suggest.

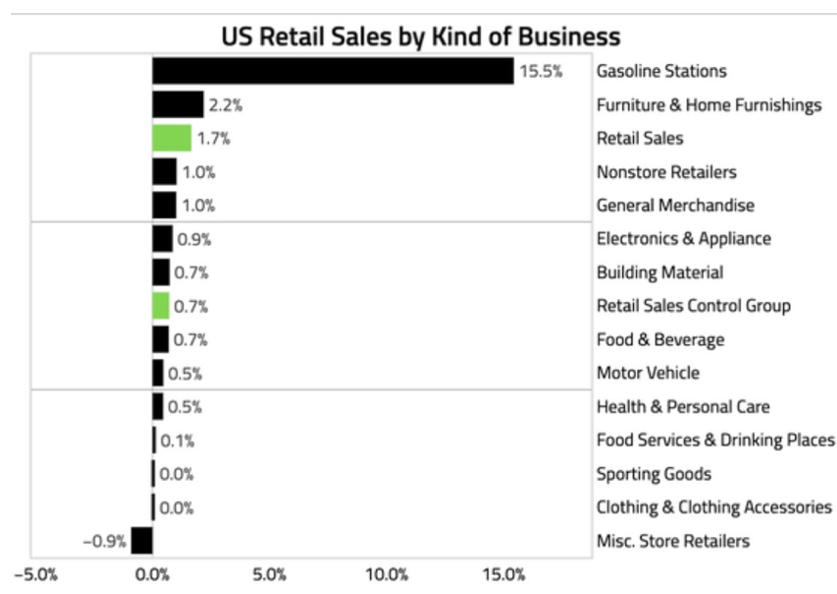

You can see part of that in the retail sales data. The consumer has still been spending, but the mix matters. Some of the recent strength came from a jump in gasoline sales and some temporary support from tax refund season. In other words, the spending data was not weak, but not all of the strength was organic either.

That matters because it helps explain why the consumer has looked stronger than sentiment. Households got a bit of help from refund-related cash flow and other temporary factors, even as they continued to complain about prices. That is a very normal human response. People can say things feel expensive and still keep spending if cash is available.

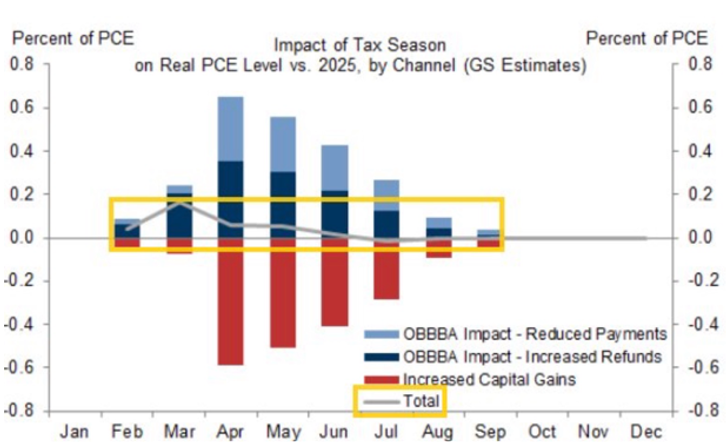

The next question is whether the gas price shock starts to pinch more meaningfully.

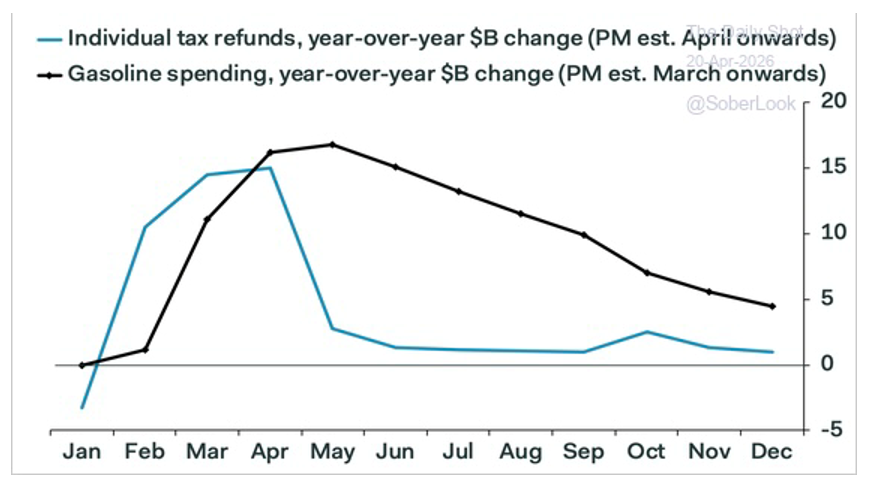

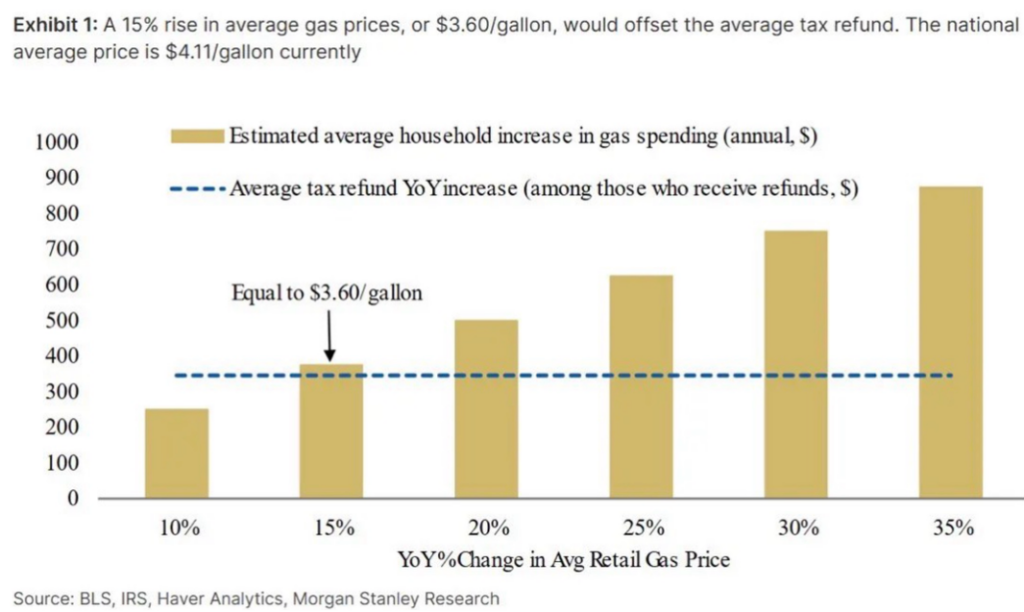

This chart makes the timing issue clear. The cash-flow lift from refunds is coming just in time to offset the high costs at the pump. But time is of the essence as those refunds will wear off and gas prices might not.

That does not mean the consumer falls off a cliff. It just means the support gets a little less helpful as the year moves along.

This is another good way to frame it. It does not take an extreme move in gas prices to eat into the benefit of a typical refund. If gasoline stays elevated long enough, a good part of that springtime cash-flow cushion gets absorbed at the pump.

Again, that is not an argument for immediate collapse. It is just a reminder that there is a difference between a short-term spending boost and a durable tailwind. This is where the timing becomes especially important.

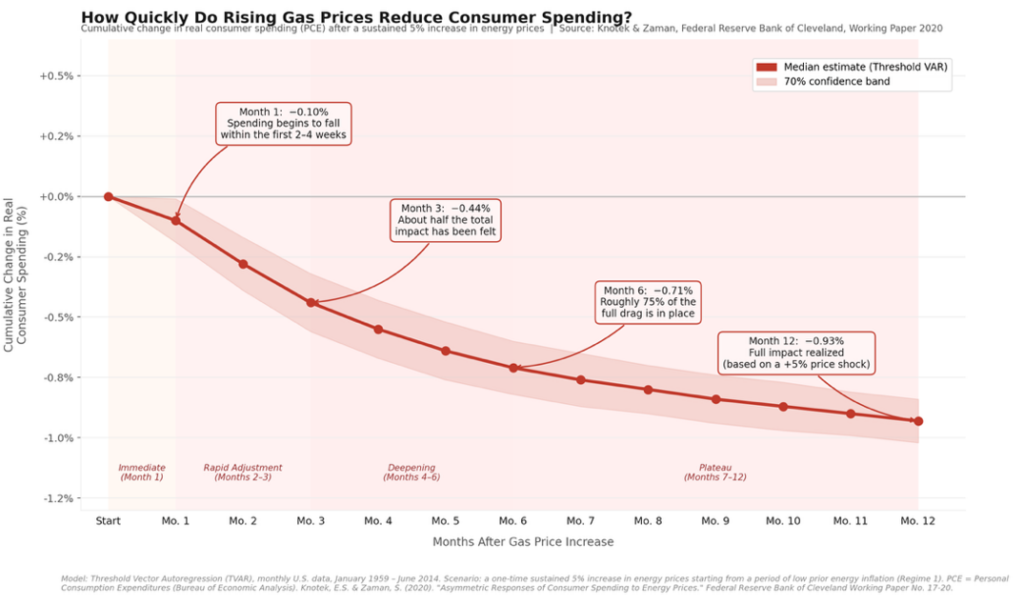

Higher gas prices do hurt spending, but they do not typically crush it all at once. The Cleveland Fed work shown here suggests the drag builds over time. The first month impact is modest. By month three, a meaningful share of the effect has shown up. By month six, much of the drag is in place. By month twelve, the full effect is felt.

That matters for investors because markets do not trade off the headline alone. They trade off the path. If the consumer is getting squeezed, but the squeeze shows up gradually; there is still time for wage income, balance sheet support, or policy relief to offset part of the damage. There is also time for companies to keep delivering earnings growth even while the macro debate feels uncomfortable.

That is the heart of the paradox. Consumers can feel bad and still spend. Spending can remain decent even as gas prices rise. And earnings can keep moving higher while everyone insists the backdrop feels awful.

That last part is what the market seems to be focusing on.

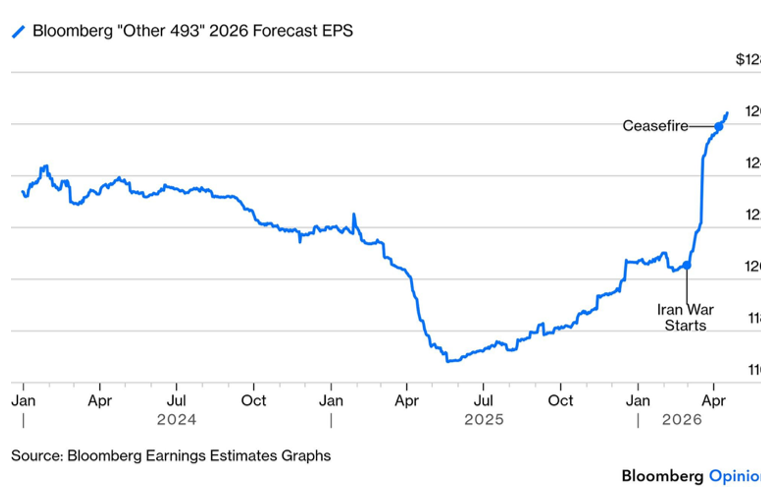

This is the simplest summary of the whole setup. While the war period and oil shock have dominated the narrative, earnings expectations for the broad market have moved higher. That is not supposed to happen if the economy is immediately rolling over. It is happening because the underlying spending and profit backdrop has remained firmer than the sentiment data would suggest.

Now comes the test.

On Wednesday alone, roughly $13 trillion of market cap reports earnings, including some of the largest companies in the index. That is why this week matters. The market is not just debating sentiment anymore. It is about to hear directly from the companies carrying a large share of the index’s earnings power.

And importantly, this is not just a story about a few mega-cap companies carrying the index. The earnings revisions have broadened out.

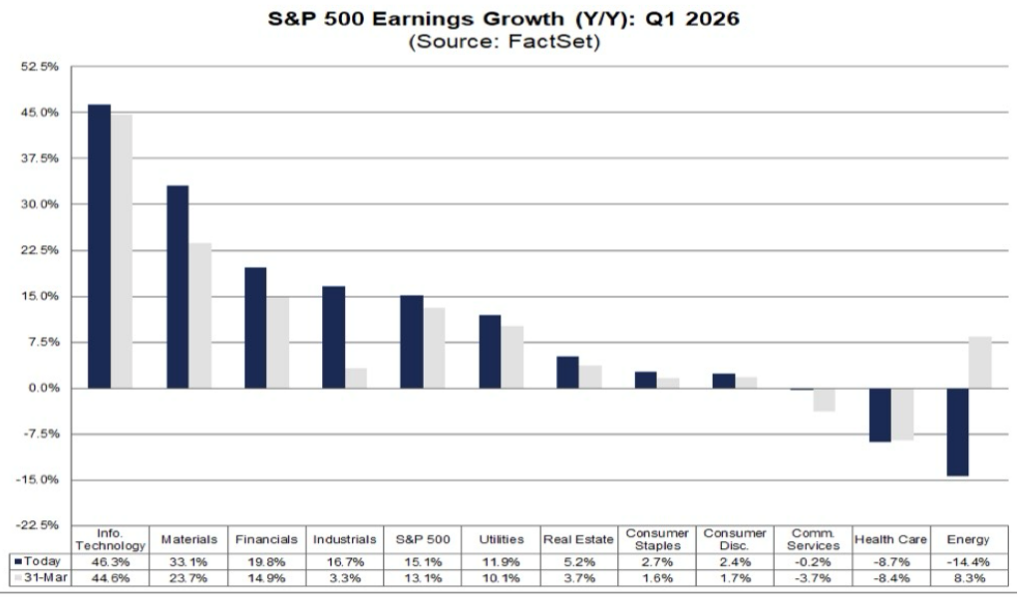

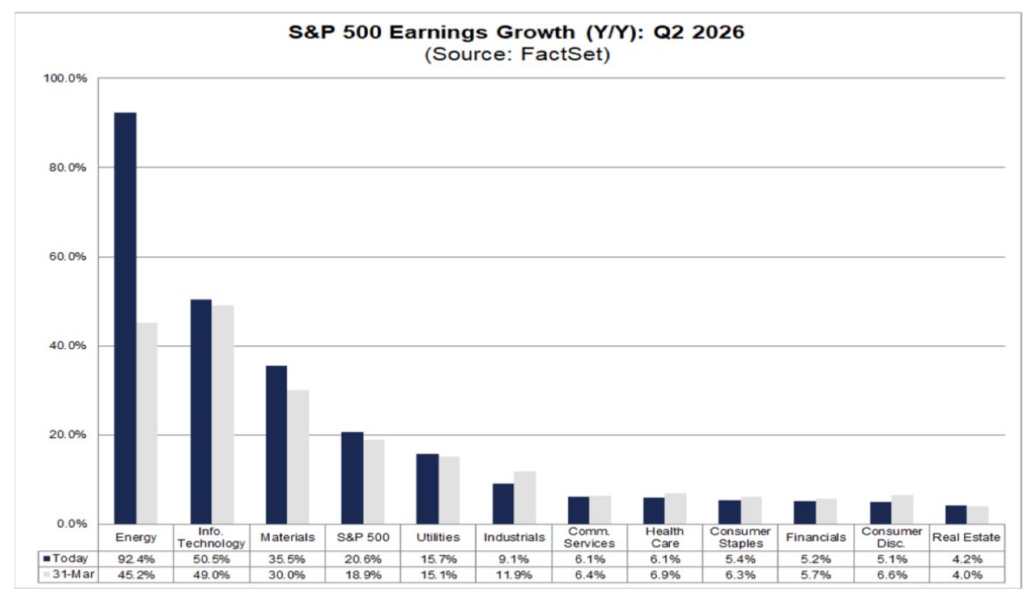

Q1 helped establish that base. Earnings expectations have risen from 13% to 15% EPS growth. Expectations and realized momentum have been strongest in areas like technology, materials, and financials, while weakness has been more sector-specific. The bigger point is that the earnings engine did not stall. It kept running.

Now Q2 expectations are moving higher as well from 19% to nearly 21% EPS growth. Yes that’s right 21% EPS growth-remarkable. Analysts are not simply recognizing what already happened. They are revising forward numbers up. Energy is a large part of that, of course, but technology and materials remain strong, and the broader S&P 500 earnings picture has improved too.

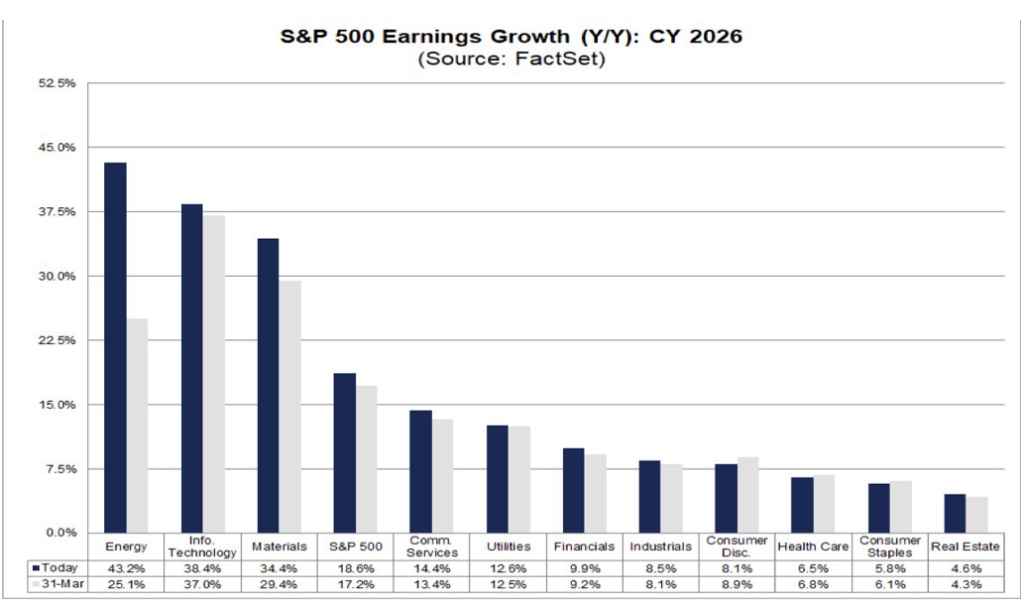

The full-year view tells the same story. Earnings expectations for calendar year 2026 have continued to rise. That is the fundamental support underneath the market. When investors are willing to look through uncomfortable news flow, it is usually because the earnings math still works. Right now, it still does.

So if we step back, the paradox is not really a paradox at all.

Consumers feel bad because prices are still irritating, the geopolitical backdrop is noisy, and confidence is fragile. But they have continued to spend because the pocketbook damage has been slower and more uneven than the headlines imply, and because some near-term cash-flow support has helped bridge the gap. That spending is showing up in corporate results. And those results are pushing earnings expectations higher.

For now, the market is making a fairly simple bet: consumers may not be happy, but as long as they keep spending, earnings can keep surprising to the upside.

And in this market, it is still the earnings that matter most.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

References: S&P 500 vs. Consumer Sentiment: Creative Planning / Charlie Bilello, YCharts, April 19, 2026; U.S. Retail Sales and Retail Sales by Kind of Business: The Daily Shot, March 2026 retail sales data, underlying data from U.S. Census Bureau; Tax Refunds vs. Gasoline Spending: The Daily Shot / Sober Look, using IRS refund data and gasoline spending estimates; Gas Price Increase Offset to Average Tax Refund: Morgan Stanley Research, using BLS, IRS, and Haver Analytics data; Gas Prices and Consumer Spending Impact: Knotek & Zaman, Federal Reserve Bank of Cleveland Working Paper, 2020, “Asymmetric Responses of Consumer Spending to Energy Prices”; Bloomberg “Other 493” 2026 Forecast EPS: Bloomberg Earnings Estimates Graphs / Bloomberg Opinion; S&P 500 Earnings Growth Q1 2026, Q2 2026, and Calendar Year 2026: FactSet, sector-level year-over-year earnings growth estimates.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.