Last week, I wrote (Can Fear Fuel The Next Rally?) that the tone of the news had become so negative that it was beginning to create the conditions for a rally, rather than setting up another leg down. That is often how markets work. They bottom or rebound not when the headlines improve—although they sometimes do, albeit temporarily—but when investors have already spent weeks adjusting to the worst versions of those headlines. We got that rally.

The move was fast enough to make people uncomfortable, which is usually the point. It feels like something that cannot be trusted. But markets do not wait around for emotional closure. They move when positioning is offside, fear has already done its damage, and the underlying profit cycle remains strong enough to justify a reset higher.

That is what makes this recent move worth paying attention to. An 11-day rally of more than 10% is not typical market behavior. It represents a genuine shift in tone. And while these bursts do not guarantee a straight line higher, the history is better than many people assume. The table on similar episodes shows that once these kinds of rallies take hold, forward returns over the next three, six, and twelve months have tended to be better than average. That does not mean risk disappears. It means that markets often have more room than our instincts allow, especially right after fear may have peaked.

There is an important distinction here. A rally like this can start with short covering, repositioning, and a simple absence of sellers. But it does not continue on technicals alone. At some point, fundamentals have to step in and do their part. That brings us to earnings season.

One of the more interesting aspects of this setup is that, when you compare the market’s recent path to its closest historical analogs, the forward outlook remains constructive. Again, that is not a forecast in the precise sense. Markets do not repeat cleanly enough for that. But it reinforces the idea that, once a market absorbs a shock, shakes out weak positioning, and begins to recover, the path forward is often better than the mood would suggest.

The chart setup suggests the market is recovering from a mid-cycle correction. If current earnings remain resilient and the AI/tech capex cycle continues to drive productivity—mirroring the 1996–1999 internet buildout— the base rate strongly favors the bullish continuation seen in the three positive analogs. However, if inflation remains sticky and profit margins compress, the 2022 peak-cycle template becomes the primary risk.

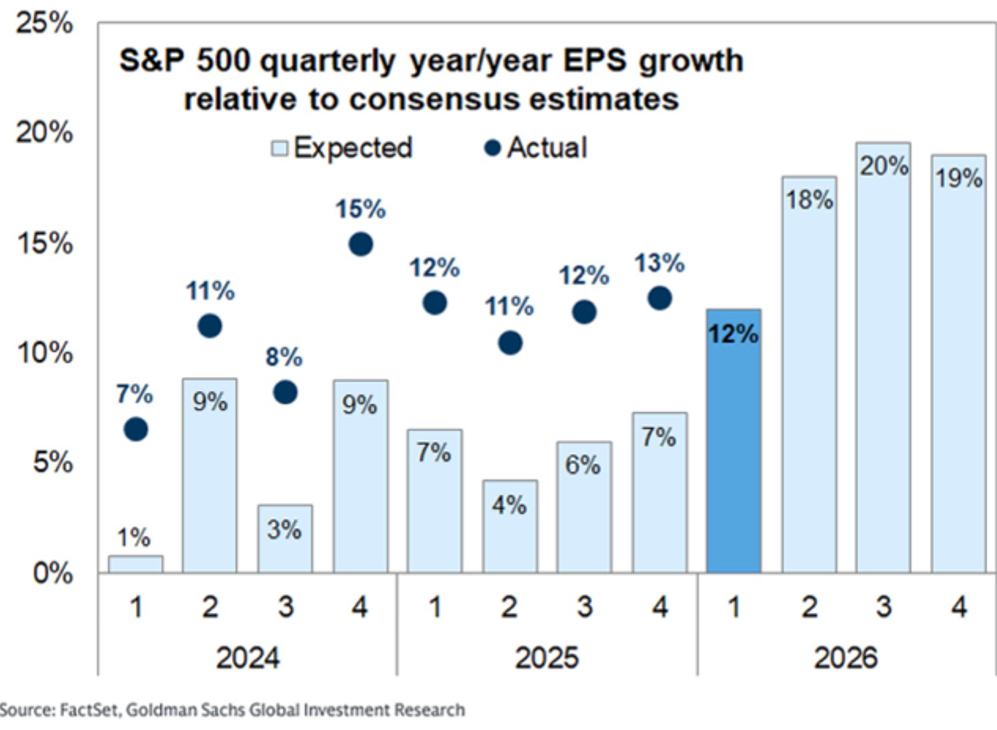

The primary focus is an earnings backdrop that still looks strong. Consensus expects S&P 500 earnings growth of roughly 12% year over year in the first quarter, with the back half of the year still expected to show even stronger numbers. It is the kind of setup that can support higher equity prices if companies deliver something close to what is being penciled in today.

To me, that is the key issue for the next few weeks. The rally itself has already happened. The easy part—or at least the emotional part—was the bounce off fear. The harder part is whether corporate America validates what the market is trying to price in. If earnings come in reasonably well, guidance remains intact, and margins hold up better than expected, then this market has a decent foundation under it.

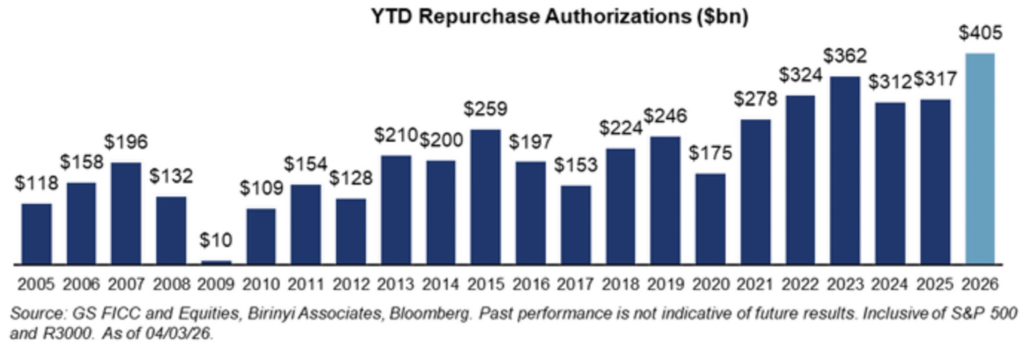

There are a few reasons to think companies still have support. One is that corporate America continues to behave as though business conditions are strong enough to return capital aggressively. Buyback authorizations this year are running at a record pace. That is a bullish indicator that companies find their equity valuations favorable relative to their earnings. Perhaps we should too.

That point is especially important in a market where skepticism still runs beneath the surface. We have spent so much time talking about geopolitical risk, sticky inflation, deficits, and whether the AI trade has run too far that it is easy to miss the simpler truth: many businesses are still growing, still earning, and still generating excess capital. Markets can climb in that kind of environment even when the news remains noisy. In fact, they often do.

That is really the broader message of the moment. Last week’s rally did not come out of nowhere. It came from a market that had already priced in a lot of fear and was ready to move on from the worst of it. We will certainly know how “ready” investors are to move based on the resurfacing of geopolitical risks. But after a move like this, the burden shifts. The next phase will not be driven just by relief. It will be driven by delivery. Earnings need to hold up. Guidance needs to remain respectable. Capital spending needs to remain credible. The biggest secular themes in the market need to keep proving they are more than stories.

For now, the setup still looks constructive to me. History suggests these moves can have more life than most investors assume. Earnings expectations remain solid. Corporate buybacks remain a meaningful tailwind. None of that means the path will be smooth, and it certainly does not mean every theme in the market is fully grounded in present-day reality. But it does mean the market has moved beyond pure fear and is now asking a more useful question: Are profits there to support what prices imply?

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

- Bespoke Investment Group, The Bespoke Report (April 17, 2026)

- Goldman Sachs Global Investment Research

- FactSet; Birinyi Associates

- Bloomberg; Financial Times

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.