The Tale of Two Bubbles in America’s Economy

We’re living through one of the most talked-about investment booms of our lifetime. Everywhere you turn, investors, companies, and commentators are fixated on the same thing:

AI, data centers, and the cap-ex wave powering it all.

It’s the rare moment when Wall Street, corporate America, and the public are all staring at the same shiny object. And to be fair—what’s happening in AI and capital spending is remarkable. Companies are investing real dollars in capacity, software, chips, and productivity tools at a pace we haven’t seen in decades.

But as we race to debate whether AI is a bubble, we’re missing the far bigger, quieter story happening right underneath us.

It’s a story that shows up in county-level income, federal spending, and household dependency—yet almost never in headlines. It turns out the biggest bubble in America today isn’t in technology.

It’s in transfer payments—and unlike AI, almost no one is talking about it, and that’s usually the first sign of a real bubble.

The “Loud” Bubble: AI and CapEx

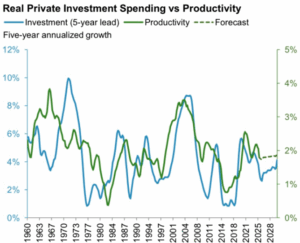

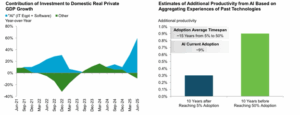

Let’s start where everyone else is looking. Investment in AI infrastructure and related cap-ex isn’t simply hype—it fits into a historical pattern we’ve seen many times before. Investment reliably drives productivity, and I expect that to be the case this time around.

There’s a roughly five-year lag between investment spikes and productivity gains. The wave of investment we’re seeing today is right on schedule for productivity tailwinds later this decade.

AI adoption is still early and that should only grow as more companies and individuals learn the power of using AI. Real economic growth can accelerate as we adopt the tool being built. Sure, companies are spending a trillion dollars to capture this trend but the payoff to the overall economy is exponential. At ~9% adoption, the biggest productivity gains historically come long before adoption hits 50%.

Investment is filling the gap left by slow income growth. When wages stagnate, investment—not labor—becomes the growth engine.

So yes, AI is loud, but that doesn’t make it reckless. It’s simply not where the real bubble is forming—we’re only in the first quarter of a long game.

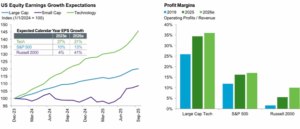

Earnings expectations justify the spend.

Tech earnings are expected to grow 27% in 2025, and 21% in 2026—hardly “bubble-like” when the top-line numbers support it.

Profit margins tell the same story. With large-cap tech margins above 35%, companies aren’t speculating—they’re reinvesting.

The “Quiet” Bubble: Transfer Payments

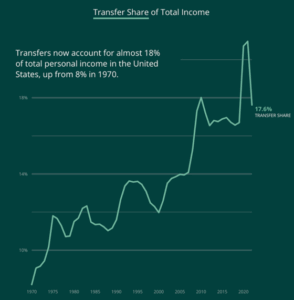

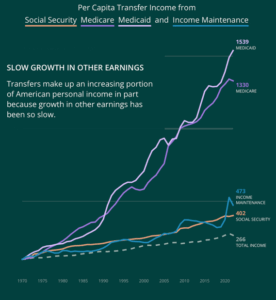

Now let’s turn to the part of the economy where the real risk lies. Transfers have doubled as a share of personal income. Transfer payments are simply payments made to individuals from the government to cover things like healthcare, food support, and retirement programs, just to name a few.

From 8% in 1970 to ~18% today, transfers are no longer a backstop—they’re a foundation.

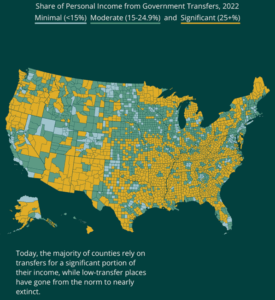

County-level reliance has grown dramatically

In 1970, only isolated distressed areas depended heavily on transfers. Today, most U.S. counties do.

The shift is structural, not cyclical and the trend is unmistakable. Half a century ago, low-transfer counties dominated. Now they’re nearly extinct.

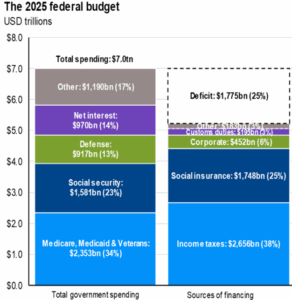

Federal spending confirms the picture.

Social Security, Medicare, Medicaid, and veterans’ benefits now represent 57% of all federal outlays, while the deficit consumes another 25%. The $1.8 trillion in borrowing required to fund these transfers is the evidence.

Transfers aren’t the side story—they are the story.

Why it’s happening

Transfers rise because:

- Wage growth is slow

- Productivity has lagged (until recently)

- Healthcare costs are high

- Population is aging

- Income maintenance has outpaced total income growth

None of this is political. It’s simply math catching up with demographics and policy choices made over decades. That’s the risk no one wants to discuss.

This brings us back to the real danger.

AI and corporate cap-ex aren’t the kind of bubbles that blow up an economy.

They’re the kind that correct, consolidate, and continue.

But the transfer bubble is different.

It’s embedded in consumption, local economies, and the federal budget. It’s woven into household income across more than half the country.

If the government ever attempts to rein it in—whether by necessity or policy—there are only two mechanical outcomes:

- Consumption falls

- Local economies contract

Not because of ideology but because of arithmetic.

The silent bubble is the one that hurts when it pops

We’re living in a two-bubble economy:

- The loud bubble—AI and capital-expenditure growth—supported by earnings, margins, and early-stage adoption.

- The quiet bubble—transfer payments—supported by little more than habit, necessity, and silence.

The loud bubble gets all the attention because it’s exciting.

The quiet bubble gets ignored because it’s uncomfortable.

But as I say:

“It’s only a bubble if no one is talking about it.”

And on this one, almost no one is.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.