NowCasts on GDP growth, as we have been discussing in prior posts (here), have come to fruition with the official reporting of U.S. GDP for Q1 2016.

The U.S. Economy grew at a paltry 0.5% in Q1 2016, consistent with prior Q1 reports of the past. [i]

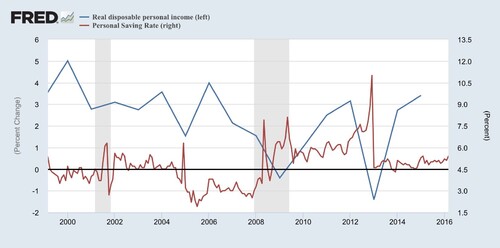

While real wages continue to grow for American workers, the U.S. Consumer just doesn’t seem ready to spend. [ii]

As you can see from the chart above, prior to the Great Recession, consumers would spend down their savings even when real incomes were dropping. However, since incomes have risen following the Great Recession, so have personal savings.

It appears the consumer lacks trust in the economy. Even with rising incomes, consumers are not spending. Peak experience bias is a difficult thing to shake. In this example, the financial pain and fear felt during the Great Recession is perhaps still with the U.S. consumer.

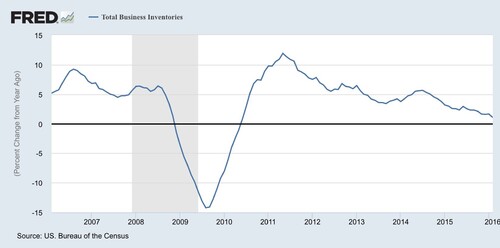

Consequently, it’s not just the consumer. Business seems more reluctant to invest. Just take a look at their inventory levels. [iii]

Businesses have been shrinking their inventories, and that’s not something you do if you’re confident in the U.S. consumer.

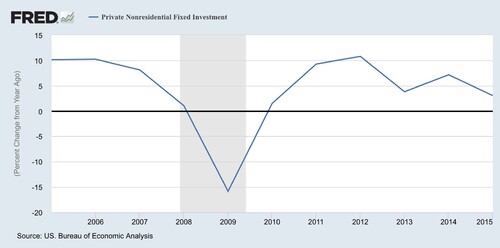

Businesses are also not willing to invest in productivity improvements either, as you can see in the chart below. [iv]

This is starting to look a little structural, in my opinion. However, consensus calls for a reversal of trends in fixed investment and inventory in the quarters to come.

For now, it would appear the Fed will need to stay on hold until we get a better grip on what’s holding back spending, consuming, and investing by both consumers and businesses.

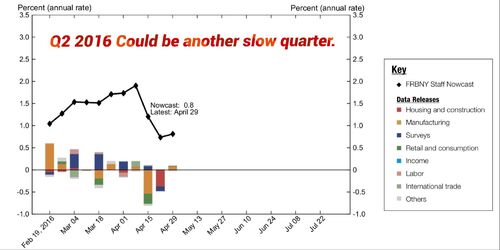

Especially since Q2 NowCasts call for a weak second quarter. [v]

Needless to say, there’s a lot to track for the remainder of Q2.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Chris Porter, Senior Investment Analyst – Phillips & Company

References:

[i] http://www.zerohedge.com/news/2016-04-28/us-economy-grew-just-05-q1-missing-expectations-lowest-growth-rate-two-years

[ii] https://research.stlouisfed.org/fred2/graph/

[iii] https://research.stlouisfed.org/fred2/graph/

[iv] https://research.stlouisfed.org/fred2/graph/

[v] https://www.newyorkfed.org/medialibrary/media/research/policy/nowcast/nowcast_2016_0429.pdf?la=en