If you’re old enough, you probably remember the lines.

In the late 1970s, cars stretched around city blocks waiting for gasoline. Drivers slept in their cars overnight. I recall the fun we as kids had playing in the gas lines with perfect strangers ignorant of the macro consequences going on. Some states rationed fuel by license plate numbers — odd days for odd plates, even days for even plates. The Iranian Revolution had disrupted the global oil supply and Americans suddenly realized how dependent the economy was on energy flowing through a narrow stretch of water halfway around the world.

It felt like the system might break.

But history tells a different story. The economy adapted. Energy markets have diversified. New technologies emerged. The decade that followed ultimately delivered a period of significant innovation and economic expansion.

Moments of panic often look very different in hindsight.

Which brings us to this week.

A Narrow Strait with Global Consequences

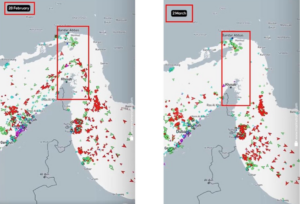

Over the past several days markets have been rattled by increased tension around the Strait of Hormuz, the narrow shipping lane connecting the Persian Gulf to the rest of the world. Nearly one-fifth of global oil supply passes through this corridor.

When something disrupts traffic there, markets pay attention quickly.

Satellite tracking shows a clear shift in tanker movements in the region over just a few days. When ships hesitate to pass through the world’s most important oil chokepoint, traders price in the risk immediately.

Oil did exactly what it tends to do in moments like this. Energy markets are often the fastest to react to geopolitical uncertainty. Over the past week, crude prices moved sharply higher. In fact, historically it’s one of the most dramatic moves in such a short period of time.

When supply risk appears, oil prices move before anything else. Energy prices often react quickly to geopolitical developments and can reflect changing risk perceptions in global markets.

But the implications of rising oil today are very different from what they were decades ago. That’s because the global energy map has changed.

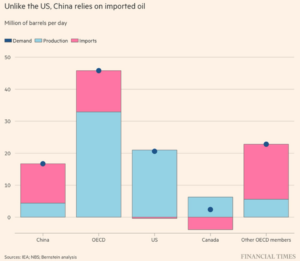

The Energy Divide: America vs China

Over the past fifteen years, the United States quietly went through an energy transformation. The shale revolution turned America from a major importer of oil into one of the largest producers in the world.

China did not have that luxury. China remains deeply dependent on imported energy. When oil prices rise, American consumers might feel it at the pump in the short run.

But China feels it everywhere. Manufacturing margins compress. Shipping costs rise. Industrial production becomes more expensive. Energy shocks ripple through their entire economic system much more quickly.

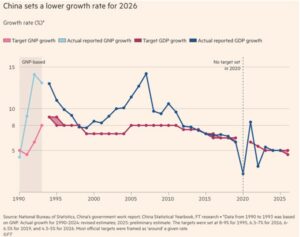

And this is happening at a moment when China’s growth engine is already slowing.

For decades, China grew at extraordinary rates — often above 8% annually. Those days are fading. Beijing recently set one of its lowest growth targets in modern history as demographics, property market weakness, and export pressures weigh on the economy.

Higher oil prices are not catastrophic for China. But they are not helpful either. It’s hard to tell at this stage what the impact will be on global growth with this small slowdown, but it’s a noteworthy episode to monitor.

Meanwhile in the U.S.: A Softer Jobs Report

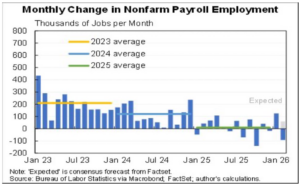

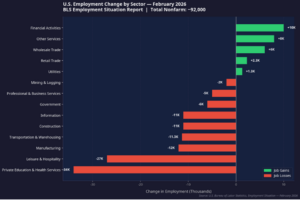

Back in the United States, the economic headline this week was the February employment report, which came in weaker than expected.

At first glance, the number looked concerning. Payroll growth stalled, and the headline print came in negative with a loss of 92,000 jobs in February.

But the more interesting story is where the weakness actually appeared.

Most of the job losses were concentrated in a handful of industries:

- Private education and healthcare

- Leisure and hospitality

- Manufacturing

- Transportation and logistics

Meanwhile, several sectors continued to add jobs, including financial services and wholesale trade. This is an important reminder that the economy rarely slows evenly.

Think of it less like a light switch turning off and more like traffic being redirected through a busy city. Some roads clog. Others open up. Over time, the system finds a new flow.

Economic change is rarely smooth, but it is constantly adaptive.

Markets Feel the Fear Faster Than the Data

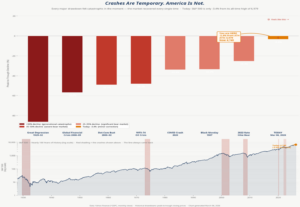

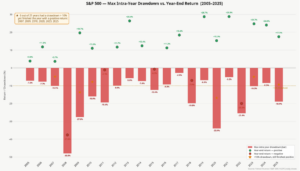

When you combine geopolitical tension, rising oil prices, and a softer jobs report, it’s not surprising that markets feel uneasy. But when we zoom out, something interesting appears.

Despite all of the headlines, the market is currently down only a few percent from its highs. That’s barely a correction.

Yet historically, markets experience drawdowns of 10% or more almost every year. And many of those same years still finish with positive returns.

Several of the most memorable downturns — 2009, 2010, 2020 — were followed by strong recoveries.

At the darkest moments in markets, some of the most respected investors in history tend to say remarkably similar things.

Market history often follows a familiar emotional cycle: uncertainty → fear → adaptation → recovery.

The Difference Between Feeling and Reality

The real lesson this week may simply be this:

Markets often feel riskier than they actually are. A potential oil disruption sounds dramatic. A weak jobs report sounds recessionary. Geopolitical tensions sound destabilizing.

But has the actual market decline so far? Small.

It just doesn’t feel that way when the news cycle is loud.

A Final Thought

One of the quiet truths of investing is that the feeling of risk almost always arrives before the reality of it. Headlines stack up — oil shocks, economic worries, geopolitical tension — and they make the present feel fragile. But history rarely remembers how nervous people felt in the moment. It remembers what happened next. And more often than not, what happens next is adaptation, recovery, and progress that only looks obvious in hindsight.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources:

International Energy Agency (IEA), U.S. Energy Information Administration (EIA), U.S. Bureau of Labor Statistics (BLS), National Bureau of Statistics of China, Financial Times, Bernstein Research, FactSet, Yahoo Finance, Berkshire Hathaway Annual Letters, Oaktree Capital Memos.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.