Two investors tell us almost everything we need to know about bubbles.

The first was one of the smartest people who ever lived: Isaac Newton. In 1720, he got caught up in the South Sea Bubble. He reportedly made money early, sold, watched others keep getting richer, and then bought back in near the top. The stock collapsed, and Newton lost a meaningful part of his fortune. The lesson was not that Newton was dumb. The lesson was that intelligence does not immunize anyone against envy, momentum, or the fear of missing out.

The second investor was Ronald Read, a Vermont gas station attendant and janitor. He did not have a trading desk, a PhD, or a Bloomberg terminal. He lived below his means, bought quality companies, collected dividends, and let time do the heavy lifting. When he died in 2014, he left behind an estate worth roughly $8 million, including major gifts to a local hospital and library. His advantage was not prediction. It was patience.

That is the tension investors feel today.

Nobody wants to be Newton, buying back in at the wrong time. But nobody wants to abandon a long-term plan just because the market looks expensive, either. So, the question I get most often is simple:

Are we in a bubble?

I think the better question is: How much good news are we already paying for?

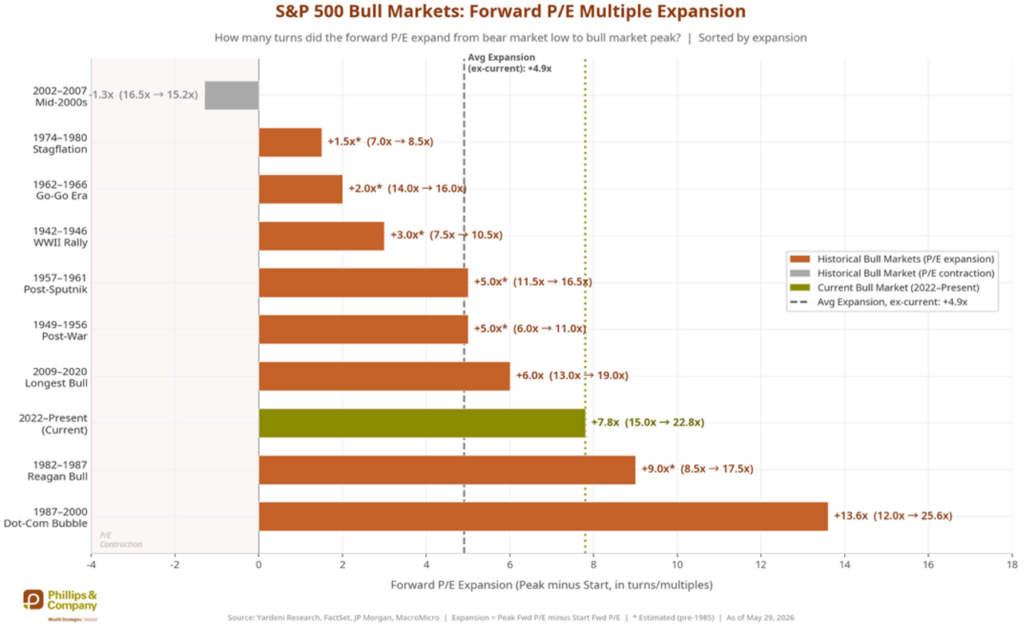

This chart is the cleanest way to frame the issue.

The current bull market began in October 2022 with the S&P 500 trading at about 15.0x forward earnings. Today, it trades at approximately 22.8x. That is a 7.8-turn expansion in the forward P/E multiple.

That matters because the average bull market multiple expansion, excluding the current cycle, is about 4.9 turns. In other words, this market has already had roughly three more turns of multiple expansion than the historical average.

In plain English, investors are not just being paid by earnings growth. A meaningful part of this bull market has come from investors deciding they are willing to pay more for the same dollar of future earnings.

That is not automatically a bubble. But it is no longer cheap.

The dot-com bubble was still more extreme. That bull market saw the forward P/E expand from about 12.0x to 25.6x, or 13.6 turns. The 1982–1987 Reagan bull market expanded by about 9.0 turns. The current cycle, at 7.8 turns, is below those extremes, but it is clearly above normal.

So my first conclusion is this:

We are not at dot-com valuation madness, but we are in a high-expectation market.

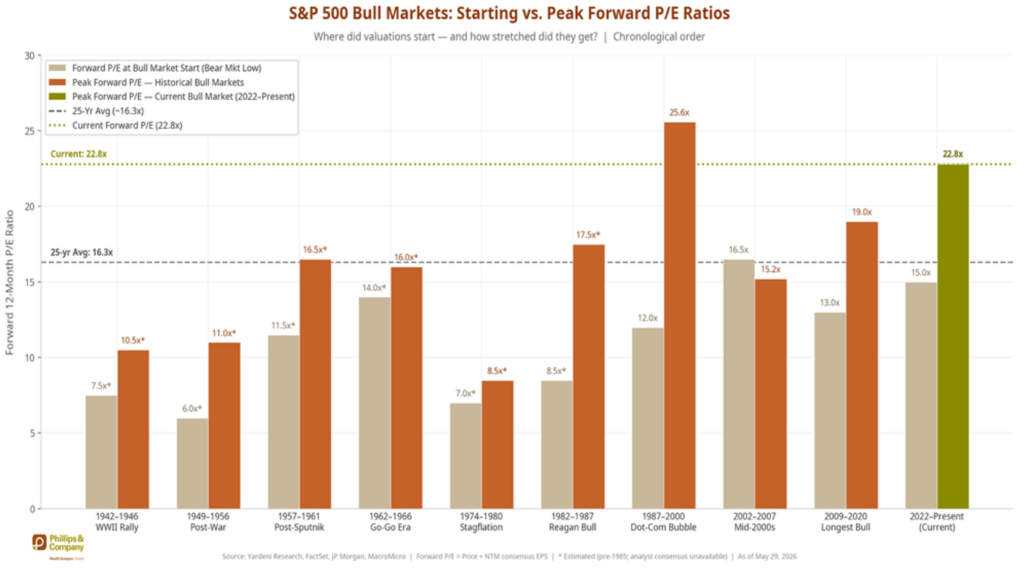

The second chart makes the same point another way.

The 25-year average forward P/E is about 16.3x. Today’s forward P/E is about 22.8x. That means the market is trading about 6.5 multiple points above its 25-year average, or roughly 40% above normal.

That is a big premium.

At 15x earnings, the market can absorb some bad news. At almost 23x earnings, it needs more things to go right. Earnings need to keep growing. Margins need to hold. Rates need to behave. Inflation cannot reaccelerate. AI needs to translate into productivity, not just a press release. And the consumer probably needs to keep showing up.

Maybe that happens. Some of it is happening now. But the higher the price, the thinner the margin of error.

That is the real point. A market does not have to be a bubble to become vulnerable. Sometimes it just has to be expensive.

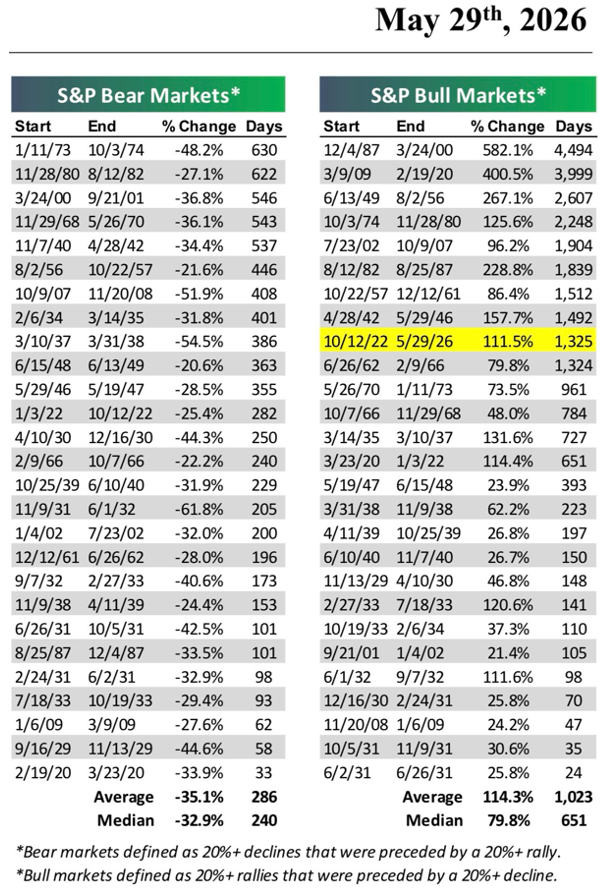

The cycle data is a little more balanced.

This bull market is up about 111.5% from the October 2022 low and has lasted about 1,325 days. The average bull market in the chart gained 114.3% and lasted 1,023 days. The median bull market gained 79.8% and lasted 651 days.

By return, we are basically near the historical average. By time, this bull market is older than average and much older than the median. But it is not ancient. The 1987–2000 bull market lasted 4,494 days. The 2009–2020 bull market lasted 3,999 days. The 1949–1956 bull market lasted 2,607 days.

That keeps me from getting too dramatic. This market is mature and expensive, but not automatically a bubble. It is strong, but not unprecedented.

The bubble question usually tempts investors into making one big heroic decision. Get out. Stay in. Call the top. Call the next leg higher.

I do not think that is the right approach.

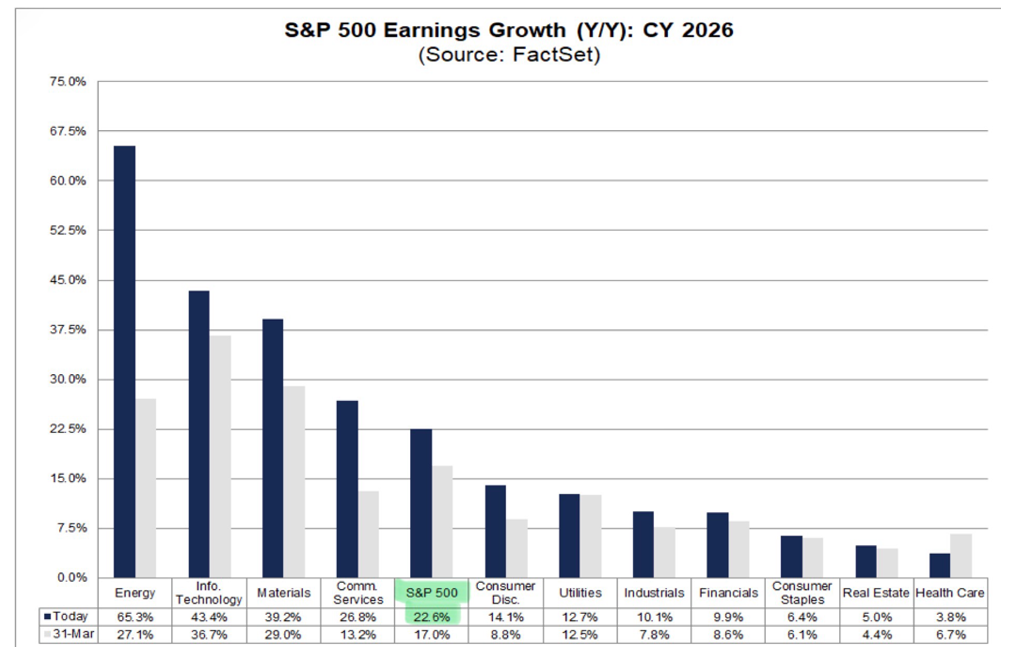

The right approach is to recognize that the easy money from multiple expansion may already be behind us. The S&P has gone from 15.0x to 22.8x forward earnings. That is a large re-rating. From here, future returns probably need to come more from earnings growth and less from investors simply paying a higher price for those earnings. That’s exactly what is expected for the rest of this year: earnings growth of around 20%.

That means discipline matters more now.

Be careful paying any price for a good story. And do not confuse an expensive market with a market that must immediately fall.

My answer to the bubble question is this:

No, I do not think we are in an obvious, market-wide bubble. But yes, I do think we are in a market priced for a pretty good outcome.

Newton reminds us that even brilliant people can get pulled into the wrong part of a cycle. Ronald Read reminds us that wealth is often built by doing sensible things for a very long time.

That is probably the right mindset today.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

Yardeni Research, FactSet, J.P. Morgan, MacroMicro, Smithsonian Magazine, and Reuters, Bespoke Investment Group

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.