Every quarter I sit down to write our Look Ahead. It has become one of my favorite exercises because it forces me to step away from the noise and ask a much simpler question:

What is the data actually telling us?

Recently I read a fascinating paper on the origins of our federal economic statistics by Hugh Rockoff. What surprised me was that unemployment, inflation, GDP, and many of the reports we rely on today weren’t created because economists simply wanted more information. They were created because Americans couldn’t agree on what was actually happening in the economy.

In the late 1800s, workers believed they were being exploited and business owners argued workers had never been more prosperous. Politicians debated whether tariffs were raising prices, immigration was depressing wages, or financial panics were destroying jobs. Everyone had a different narrative. What they lacked was a common set of facts.

That struck me because it sounds remarkably familiar.

Today we’re surrounded by headlines telling us consumers are exhausted, markets are overvalued, interest rates are too high, and uncertainty is everywhere. Depending on which news source you follow, you can find convincing arguments that we’re either headed for a recession or another market melt-up.

The debates haven’t changed much in 150 years. What has changed is the quality of the data available to us.

So instead of asking what everyone thinks, I prefer to ask what the numbers actually say.

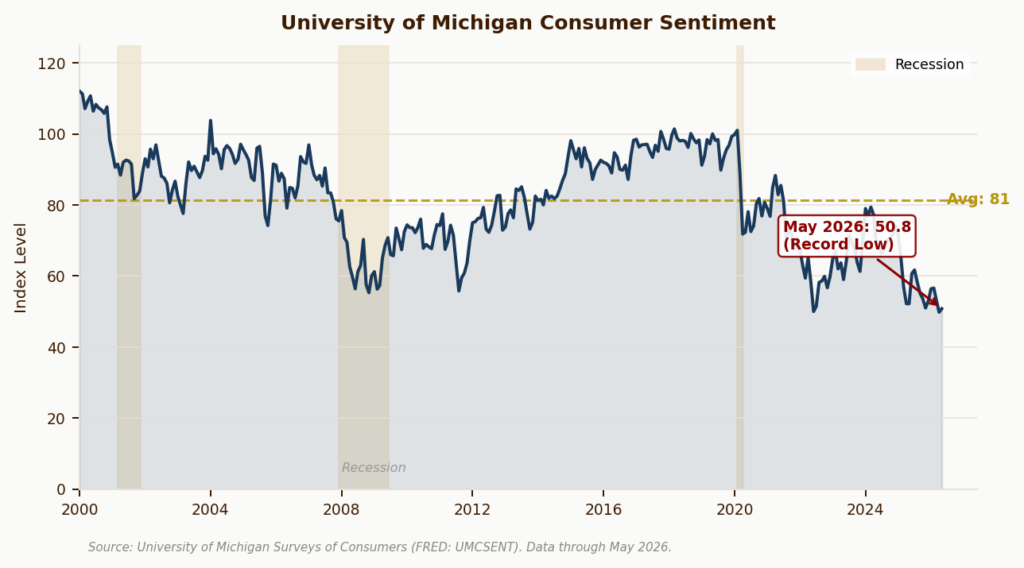

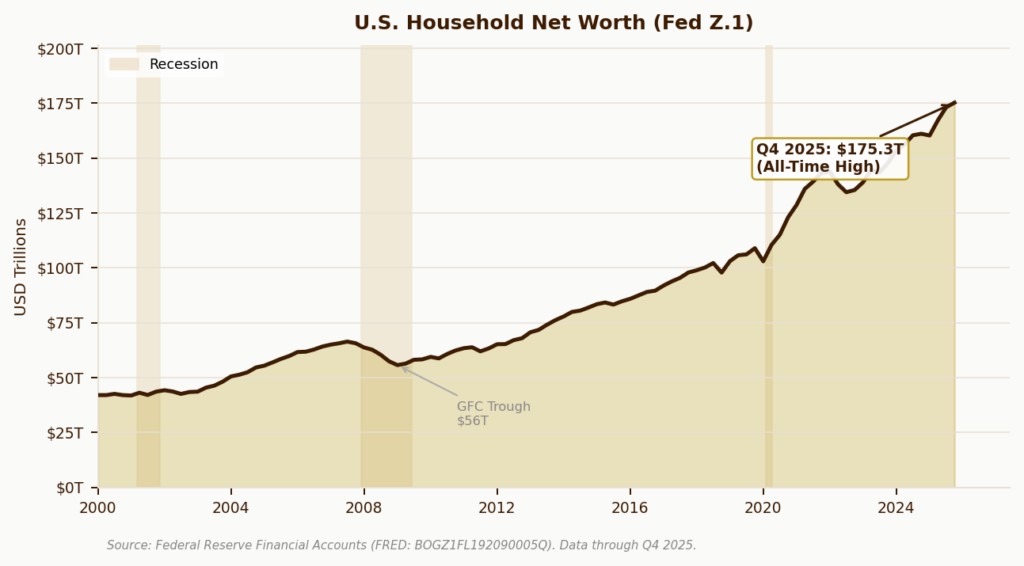

Consumer Sentiment vs. Household Net Worth

This may be the greatest contradiction in today’s economy.

Consumers continue telling surveyors they feel pessimistic, yet household wealth remains near record highs. It’s a reminder that feelings and financial reality don’t always move together.

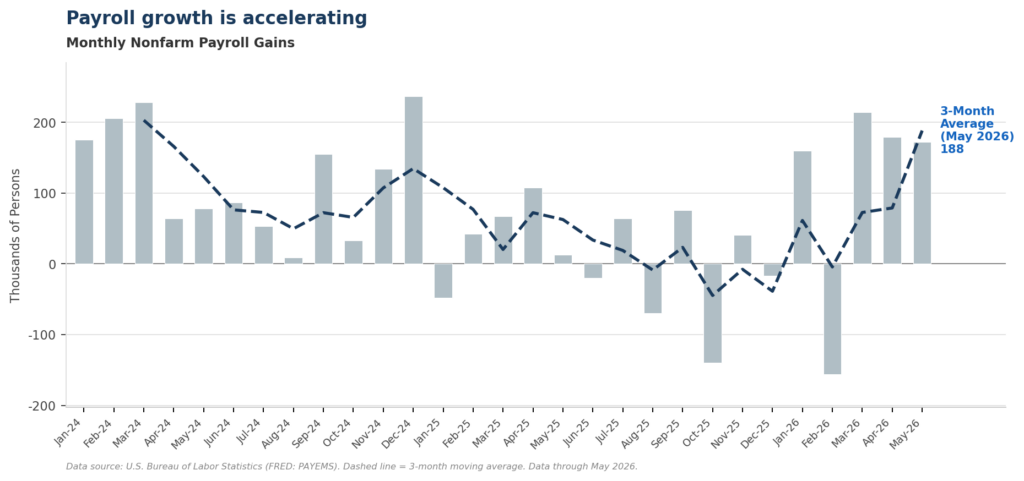

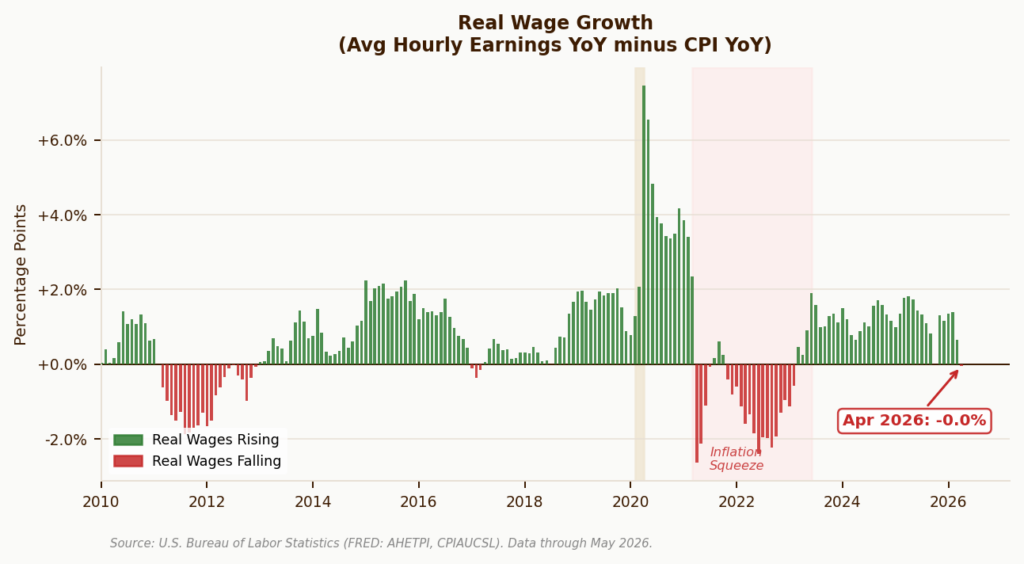

Employment, Job Openings & Wage Growth

If consumers are going to keep spending, jobs matter.

Despite years of recession predictions, employment has remained remarkably resilient. Wage growth has moderated without collapsing, and the labor market continues to support consumer spending better than many expected.

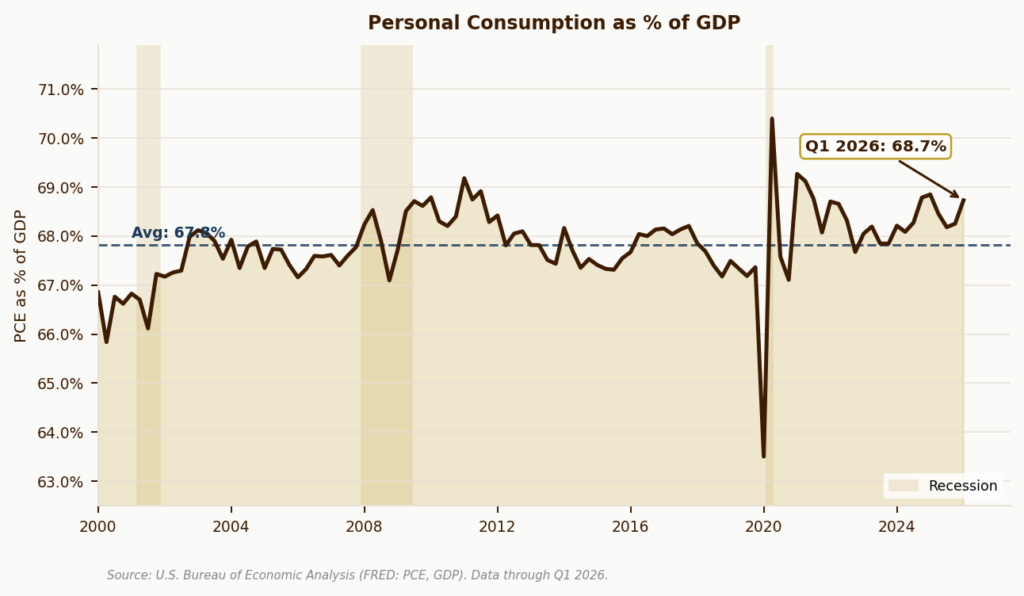

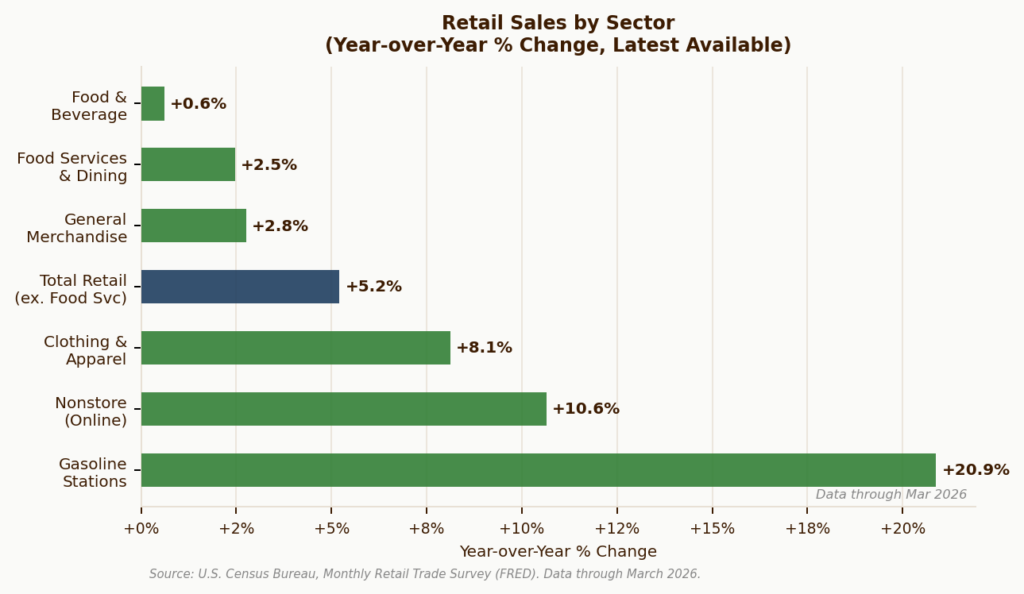

Consumption & Retail Sales

The headlines suggest consumers are tapped out yet the spending data tells a more balanced story.

Americans continue finding ways to spend, and because consumer spending drives roughly 70% of our economy, that resilience continues to support both GDP growth and corporate earnings.

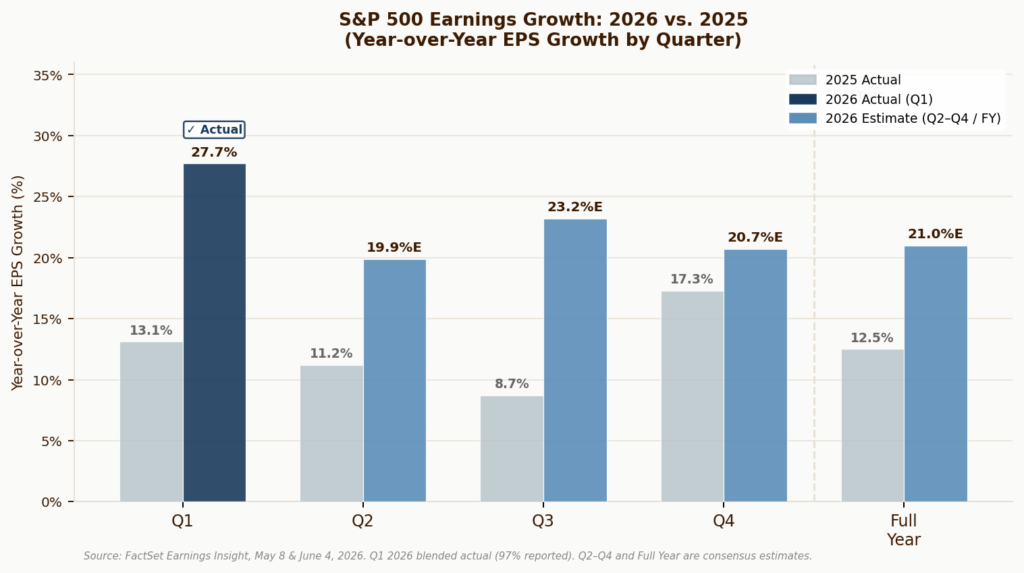

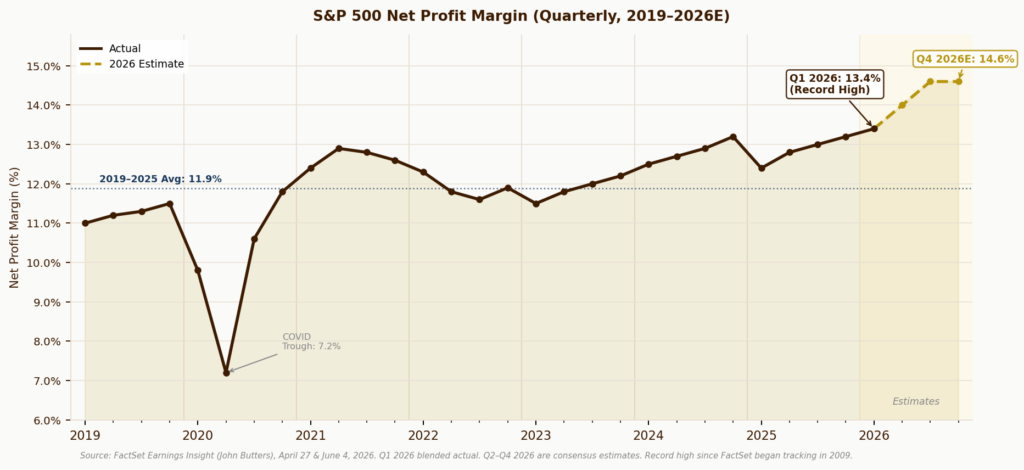

Earnings Growth & Profit Margins

High valuations dominate financial headlines.

What receives far less attention is that corporate America continues producing historically strong earnings and profit margins. Markets may be expensive, but they’re also being supported by businesses that continue to execute at a remarkably high level.

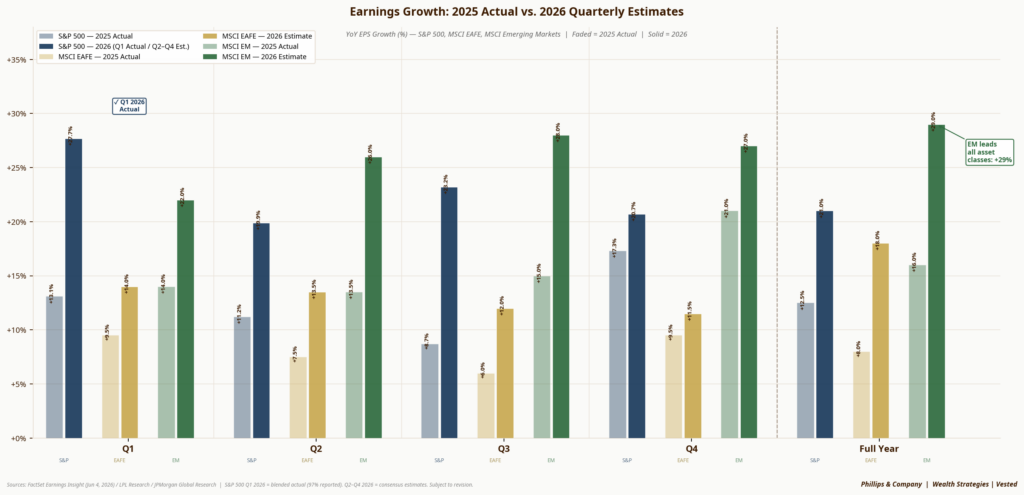

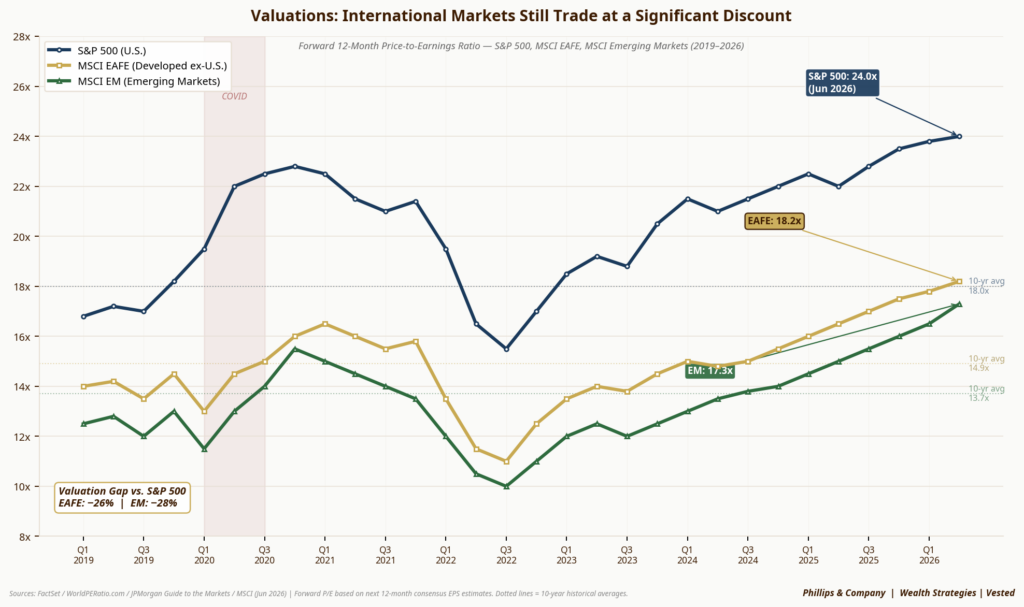

International Earnings vs. Valuations

One of the more interesting developments I’m watching is that opportunities may finally be broadening. After years of U.S. leadership, improving earnings overseas combined with more attractive valuations may be creating opportunities investors haven’t had in quite some time.

The Rockoff paper ends with an observation that I think applies just as much today as it did a century ago. Economic statistics haven’t eliminated disagreements about the economy. But they have made those debates more thoughtful because they give us a common set of facts from which to start.

That’s exactly what I hope to accomplish every quarter.

Not to predict the future or tell you how to feel, but to simply step back from the headlines and ask one question:

What do the numbers actually say compared to what we feel?

If you’d like to see the complete analysis, including how we’re interpreting these trends and positioning client portfolios for the second half of the year, I invite you to read or watch the Q3 2026 Look Ahead.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.