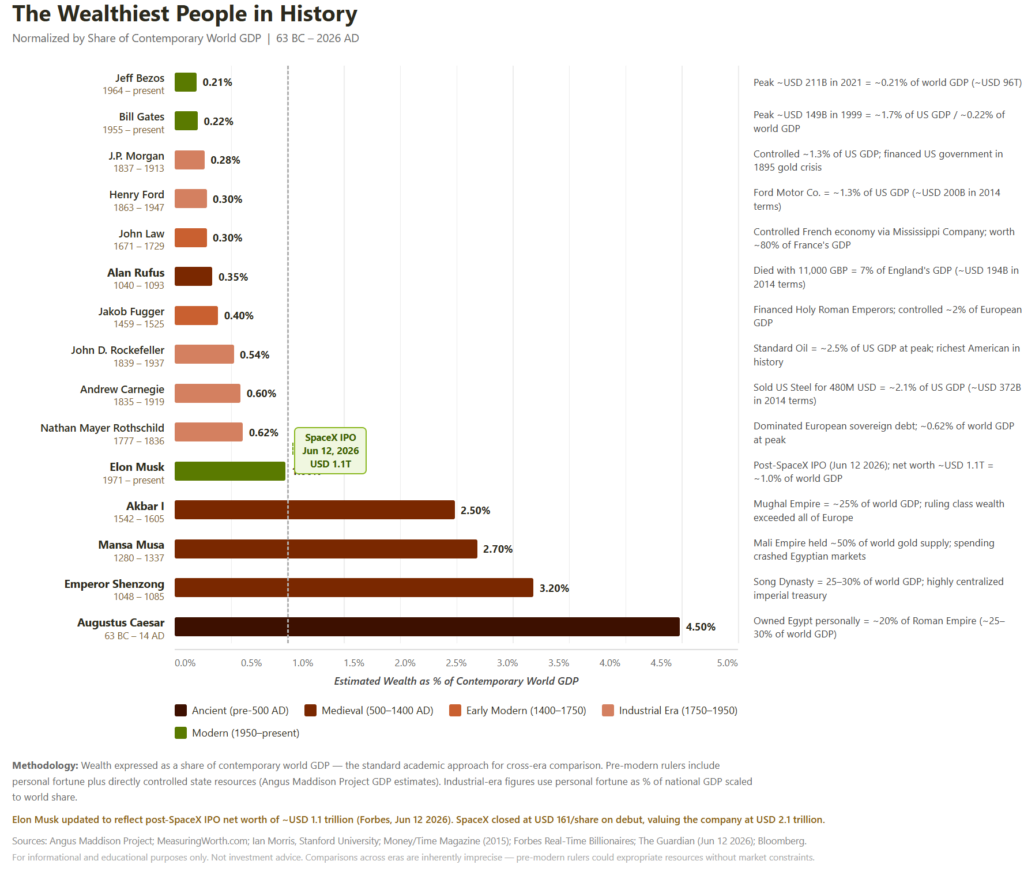

The headline last week was difficult to miss. SpaceX completed one of the largest IPOs in market history, and Elon Musk’s net worth surged toward levels once thought impossible. The result was a new publicly traded company valued at $2.1 trillion and the world’s first trillionaire. No one in the modern era has owned more wealth.

Taken together, it’s understandable why so many investors feel uncomfortable: markets appear expensive. And by some traditional measures, they are. The question is whether expensive automatically means overvalued.

I’m not convinced it does.

Let’s start with the concern.

The market’s valuation today is above its long-term average. Investors are paying more for a dollar of earnings than they have historically. That alone doesn’t prove a bubble, but it does warrant attention.

Valuation remains one of the most reliable predictors of long-term returns. The higher the price paid relative to earnings, the lower the future return potential tends to be. This is the part most investors hear, and it is not wrong.

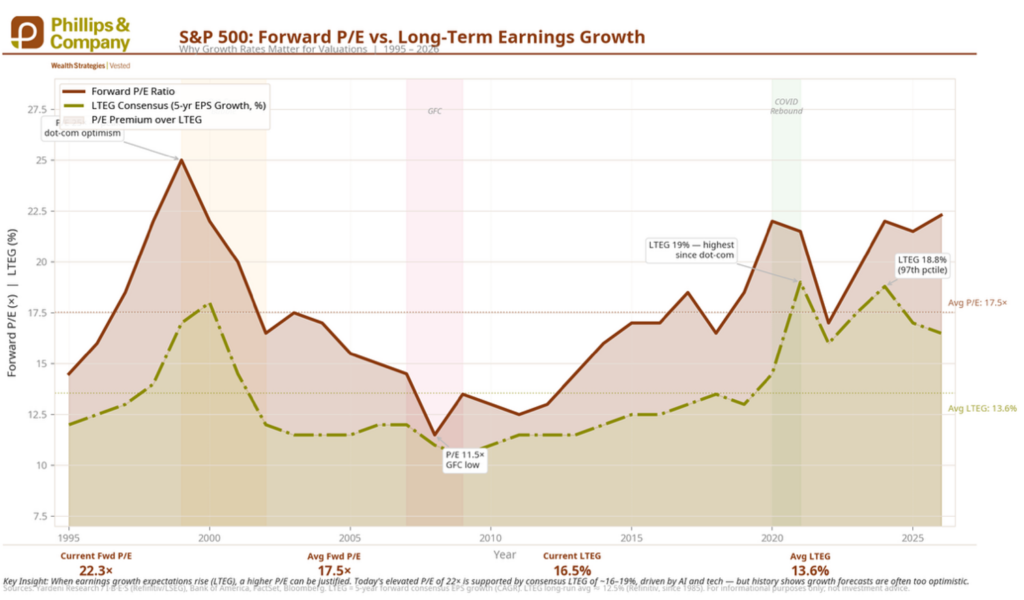

What often gets lost is why investors are willing to pay those higher valuations. Most financial headlines stop at the P/E ratio. The market trades at roughly 22× forward earnings versus a historical average closer to 17×.

Stocks are expensive.

Except markets do not value current earnings. They value future earnings.

Today’s long-term earnings growth expectations are among the strongest we’ve seen in decades. Analysts expect earnings growth approaching 17% to 19% annually over the coming years, levels that would rank near the highest readings outside of the late-1990s technology boom.

Whether those forecasts prove accurate remains to be seen. But the market is not paying a premium for average growth. It is paying a premium for what it believes will be above-average growth.

The valuation discussion becomes much more nuanced once both sides of the equation are considered.

The next question naturally follows. If earnings are expected to grow that quickly, where will the growth come from?

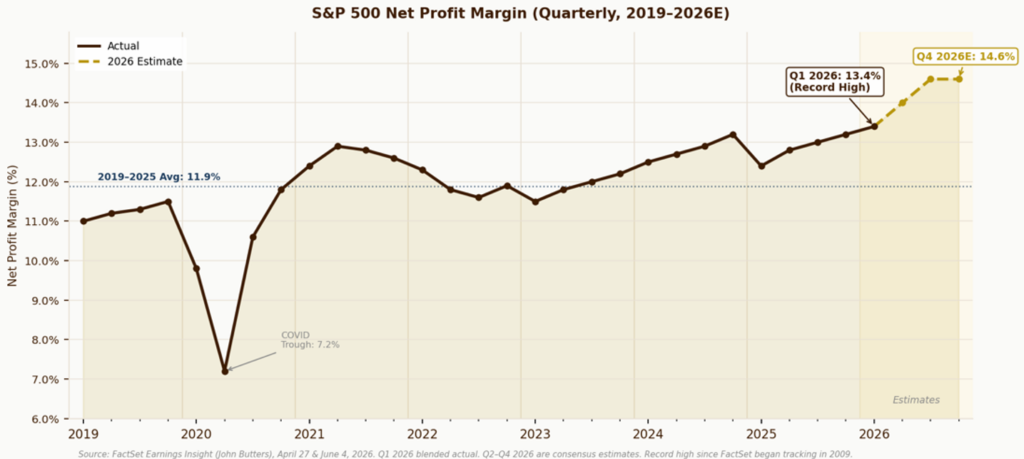

Part of the answer is profit margins.

Consensus estimates suggest S&P 500 profit margins could reach the highest levels ever recorded over the next year. That is a remarkable assumption.

For much of the past several years, investors worried about wage pressures, inflation, supply chains, and higher interest rates compressing margins.

Instead, many companies have become more efficient. The market’s optimism today is rooted less in revenue growth and more in the belief that companies can generate more profit from every dollar of revenue.

Whether that proves correct will likely determine whether current valuations ultimately look justified.

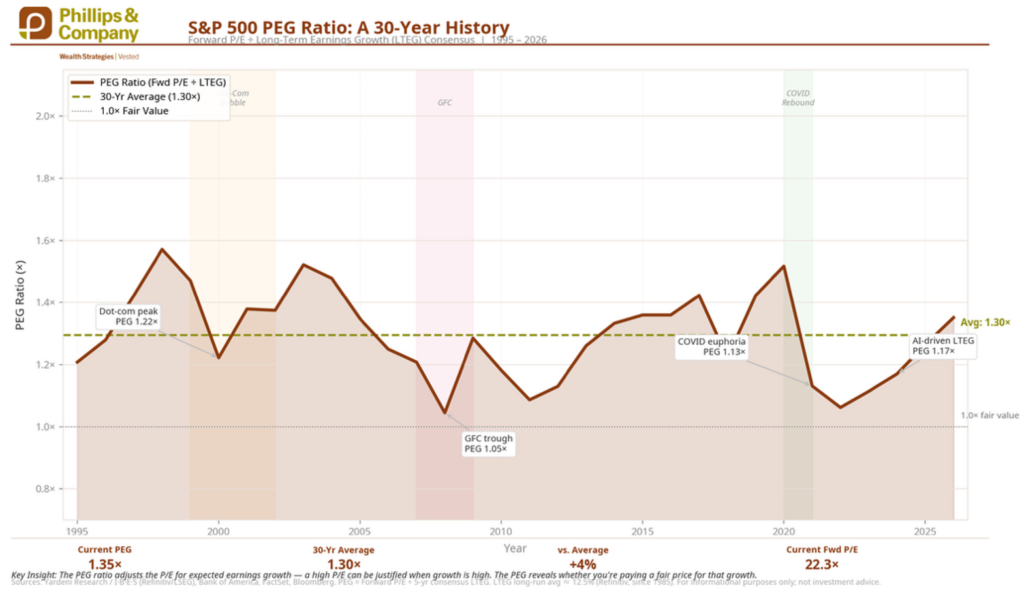

Looking strictly at P/E ratios, that argument is understandable. Looking at valuation relative to expected growth tells a somewhat different story.

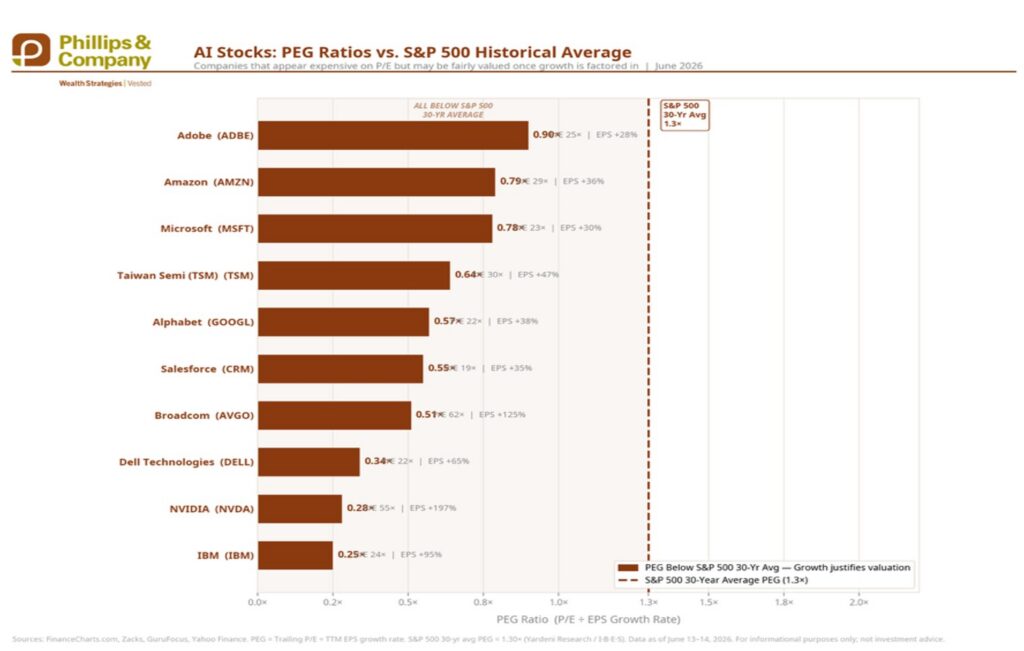

While the S&P 500 is trading at high P/E multiples, the associated growth rates tell a different story. Investors are paying more for earnings, but they are also expecting those earnings to grow much faster than normal. The P/E-to-growth ratio is only slightly above historical averages.

Again, the debate is less about today’s valuation and more about tomorrow’s earnings.

This dynamic becomes even more apparent when looking at the companies driving today’s market. Many investors see NVIDIA, Microsoft, Amazon, Broadcom, or Taiwan Semiconductor and immediately conclude they are excessively valued. Yet based on their growth rates, they may be undervalued.

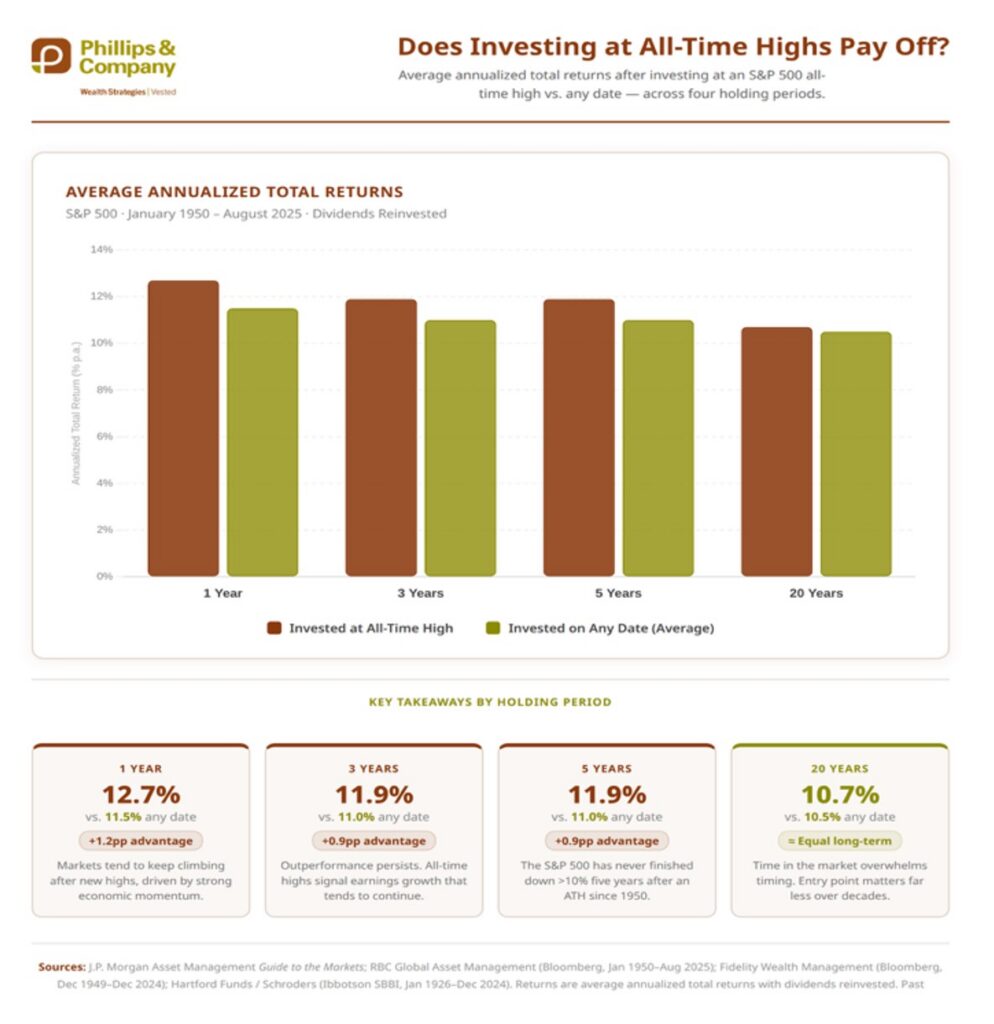

Buying at all-time highs never feels comfortable. In fact, if investing feels comfortable, it often means the opportunity has already passed. But investing at all-time highs also proves to be at no disadvantage to investing at all other times. It’s hard to believe, but the data doesn’t lie.

What history consistently shows is that markets frequently reach new highs because earnings are expanding, businesses are creating value, and economic conditions remain supportive. All-time highs are often a symptom of strength rather than excess.

That doesn’t prevent corrections from occurring. It simply reminds us that new highs, by themselves, have never been a particularly reliable timing signal.

SpaceX may ultimately prove to be a brilliant investment. It may prove to be an overpriced one, trading at over 95 times revenue. Who really knows?

What we do know is that investors tend to focus on stock price in isolation, particularly when markets are making new highs. But earnings growth matters too.

The market today is making a fairly straightforward bet: that AI, productivity gains, and expanding profit margins will allow earnings to grow faster than they have historically.

If that growth materializes, today’s valuations may look far more reasonable in hindsight than they appear today. If it doesn’t, investors will likely conclude they paid too much.

For now, I think the more interesting question is not whether markets are expensive.

The more interesting question is whether the earnings growth embedded in today’s prices can be delivered.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

Phillips & Company Advisors; Bloomberg; FactSet; Yardeni Research; Refinitiv/LSEG I/B/E/S; J.P. Morgan Asset Management; Fidelity Wealth Management; Hartford Funds; RBC Global Asset Management; Reuters. Data as of June 2026. Past performance is not indicative of future results. Forecasts, estimates, and forward-looking statements are inherently uncertain and may not be realized.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.