There’s an old investing lesson that says consumers vote twice: first with surveys, then with their wallets.

Usually, those two things eventually line up, but right now they couldn’t be further apart.

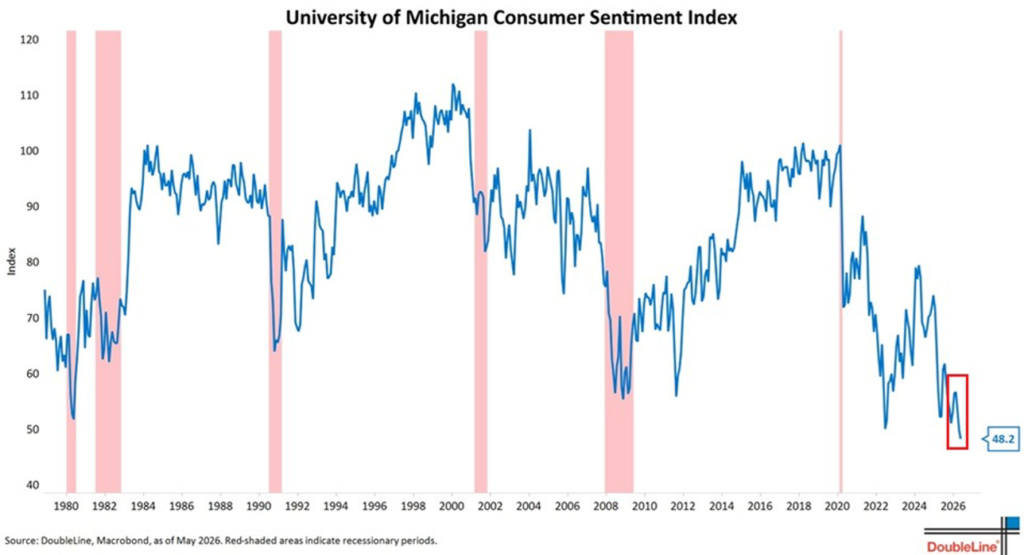

Consumer sentiment has collapsed to levels normally associated with recessions, financial crises, or major unemployment shocks. The latest University of Michigan survey is now sitting at its lowest level since it began keeping score in the 1950s.

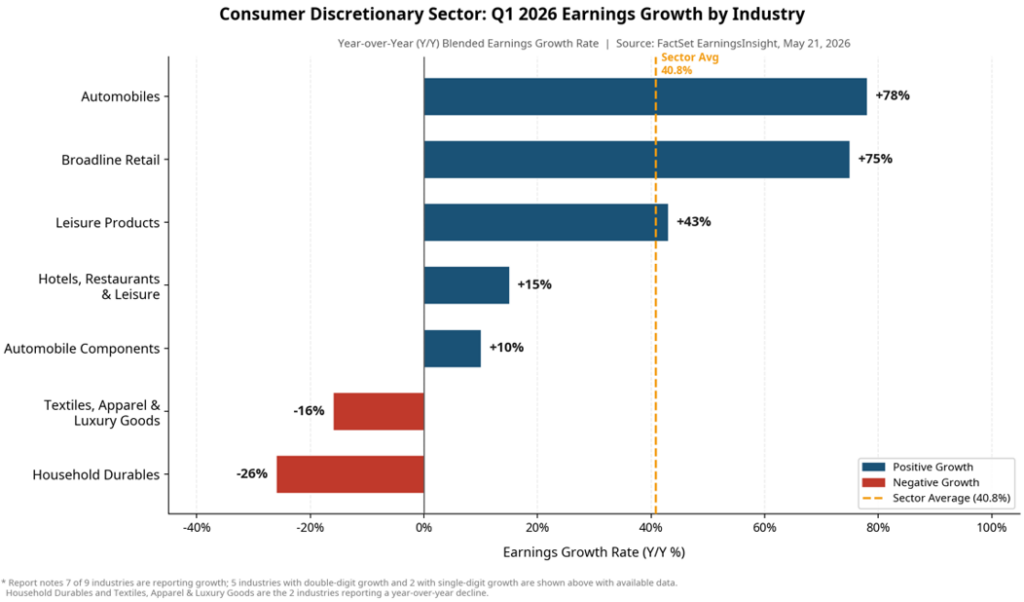

The remarkable part is what’s happening at the exact same time, underneath the surface of the economy. Many of the companies most directly exposed to consumer spending are still producing very strong earnings growth.

Automobiles up 78%.

Broadline retail up 75%.

Leisure products up 43%.

Hotels, restaurants, and leisure still positive despite years of inflation fatigue.

That doesn’t look like a consumer that’s stepped away from the economy, which lines up with what we’re seeing in the survey data. At the same time, keep in mind most of the earnings we’ve seen are Q1 numbers, with very limited impact from the Iran conflict reflected yet.

Historically, those eventually converge one way or the other. Either consumers regain confidence, or spending behavior weakens enough to validate the pessimism. My guess is that the administration knows this and will resolve the conflict and restore a normal ‘order,’ especially to oil and gas prices.

But this cycle may be getting distorted by something different entirely: fear about the future rather than stress about the present.

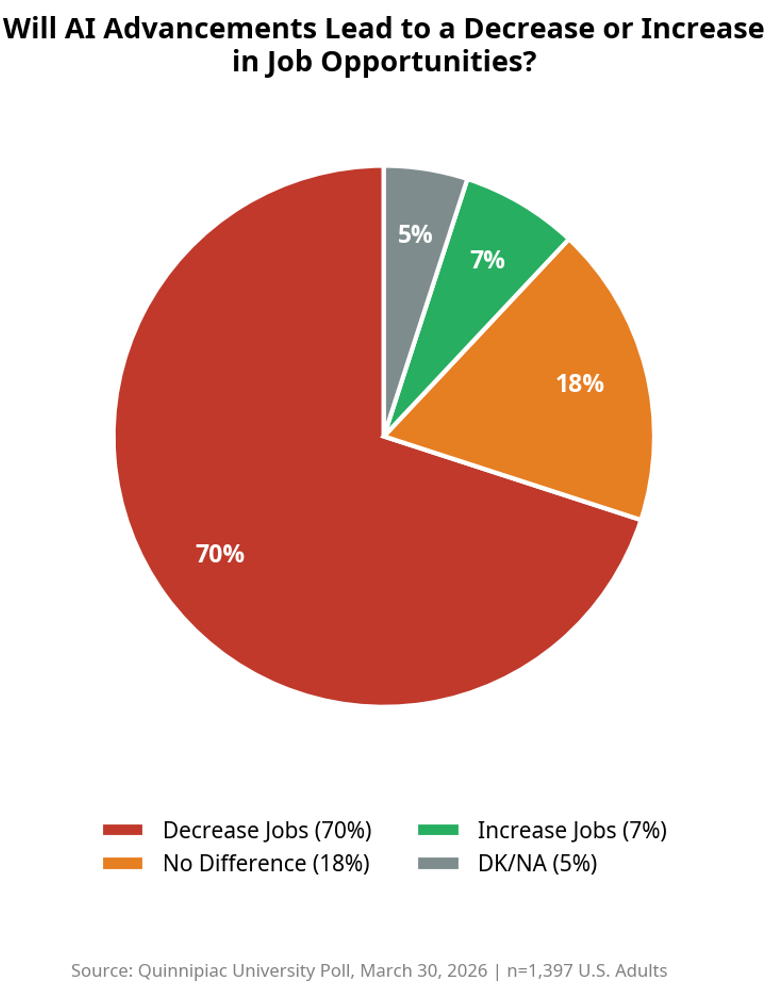

Consumers increasingly seem worried about where the economy is heading, even while their current spending behavior remains intact. And AI may be emerging as one of the clearest examples of that divide.

Roughly 70% of Americans now believe AI will reduce job opportunities over time, while only 7% believe it will increase them.

That’s an extraordinary number when you think about it.

Not because AI will or won’t create jobs eventually. History suggests new technologies usually do drive enormous productivity and entirely new industries over time.

The blacksmith probably didn’t feel optimistic watching the first automobile drive through town.

Kodak employees probably didn’t celebrate the first digital camera.

The first ATM machine probably didn’t feel like “innovation” to a bank teller.

Technology often feels threatening before it feels productive.

And consumers may be emotionally processing that disruption long before it fully shows up in the economic data.

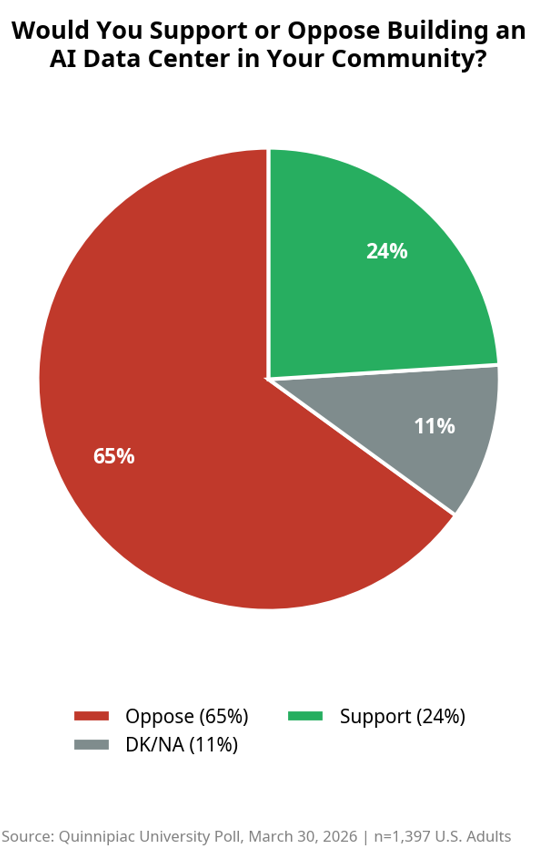

You can even see it in attitudes toward the physical infrastructure supporting AI growth itself.

Most Americans now oppose building AI data centers in their own communities.

Yes, their opposition is about electrical bills, water usage, and noise in their communities, but it’s also a statement about their uncertainty around whether AI will benefit their lives.

That’s another fascinating contradiction in this economy.

Consumers continue buying products and services from companies aggressively investing in AI productivity while simultaneously expressing growing discomfort about what that technology may ultimately mean for employment, local communities, and long-term economic stability.

In many ways, this may explain why sentiment surveys and earnings reports currently look like they belong to two entirely different economies.

Corporations are pricing in a huge win for productivity and profit margin expansion, while the consumer is pricing in the threats all of this could mean for their lives. Both can exist at the same time.

And until employment materially weakens or spending behavior finally cracks, corporate earnings may continue looking far stronger than consumer psychology suggests they should.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

University of Michigan Surveys of Consumers (May 2026 consumer sentiment data and historical comparisons); FactSet Earnings Insight Q1 2026 (Consumer Discretionary earnings growth by industry including automobiles, broadline retail, leisure products, hotels/restaurants/leisure, apparel, and household durables); Quinnipiac University Poll (March 2026 AI employment opportunity and AI data center community sentiment surveys); The Conference Board Consumer Confidence Survey (labor market differential and consumer expectations data); Federal Reserve Bank of New York research on consumer confidence and spending relationships; Federal Reserve Board research on inflation expectations and consumer behavior

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.