What can history teach us about obvious opportunities?

On Friday, the markets sold off after a stronger-than-expected employment report pushed interest rates higher. At least that’s what the headlines read.

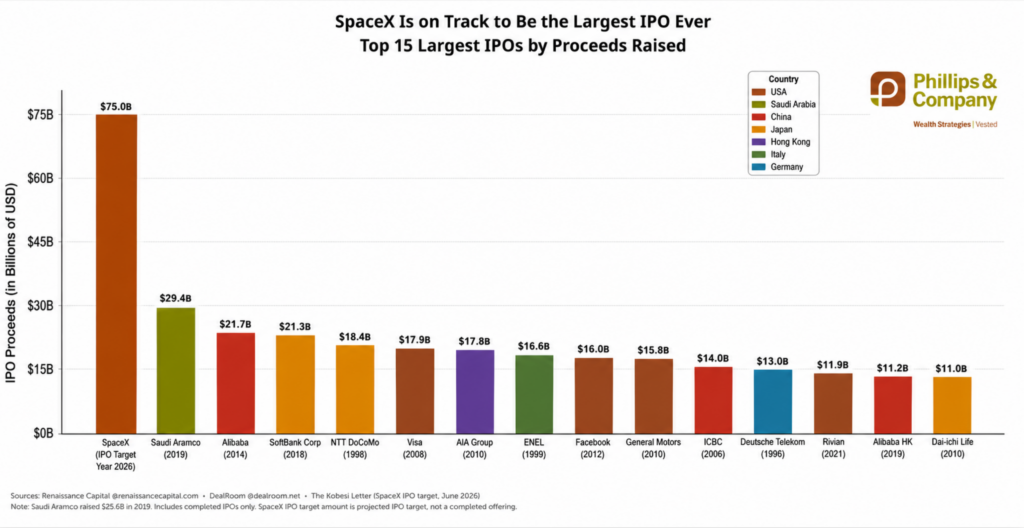

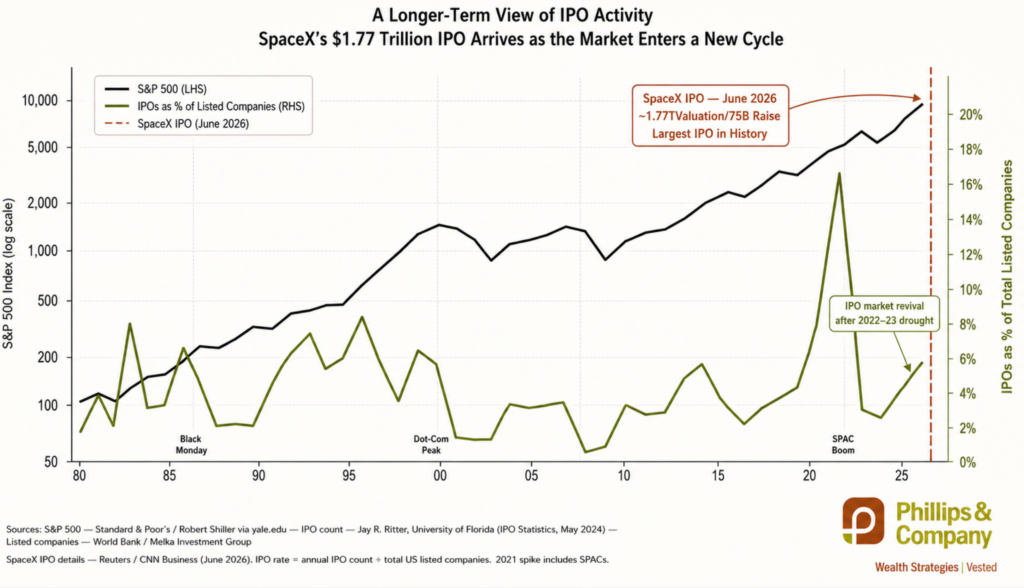

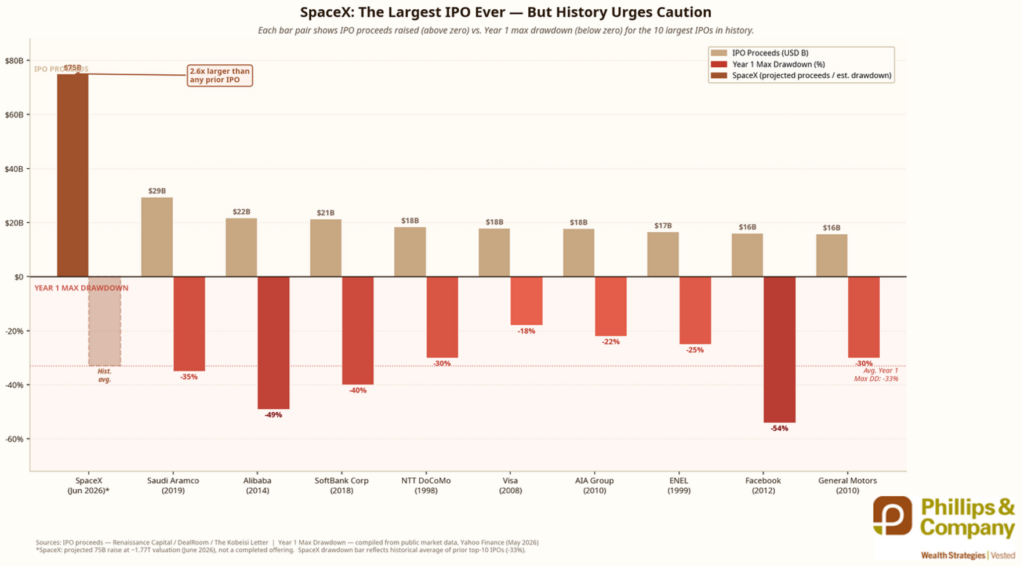

But I have another theory. This week, investors may be preparing for the largest IPO in history. At roughly $75 billion of expected proceeds and a valuation approaching $1.8 trillion, SpaceX would dwarf every IPO that came before it.

Whenever an opportunity becomes this obvious, I think about other transformational moments in our history, like the railroad boom of the 1800s. Railroads changed the world. They connected cities, lowered transportation costs, accelerated commerce, and helped create modern America.

Railroads as a technology won the day, but many investors lost money.

Both things were true.

That distinction matters because investors often assume that if a technology changes the world, buying a specific company must be a great investment. Think Northern Pacific Railway. That was an epic collapse in the 1870s.

SpaceX may very well become one of the most important companies of our generation, and I wouldn’t bet against it.

But every great IPO arrives with two separate questions:

- Is this a revolutionary company?

- Is today’s price a revolutionary opportunity?

Those are not the same questions, and investors frequently confuse them.

The IPO market has been largely dormant since 2022, and now it is reopening.

SpaceX is arriving precisely as investors have regained confidence, stocks sit near all-time highs, and risk appetite has returned.

Historically, companies don’t rush to go public when investors are fearful. They go public when demand is plentiful. If you owned one of the most valuable private companies in history, you would probably choose the same moment.

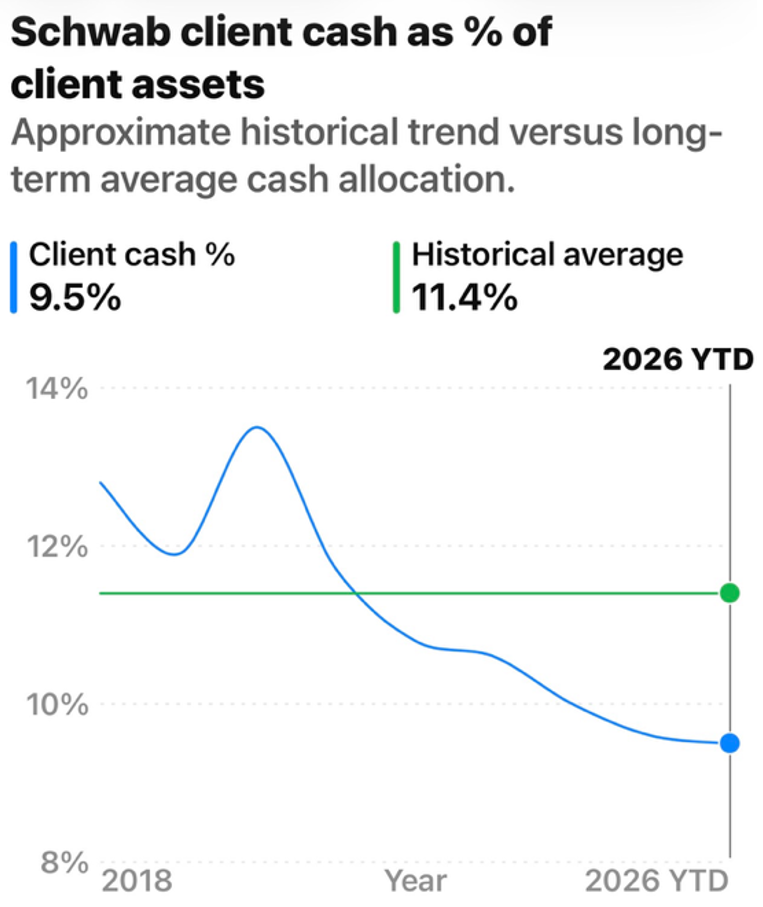

So the question begs where the $75 billion is coming from to fund the SpaceX IPO. One place it’s not coming from is cash.

For example, Schwab client cash allocations have fallen below long-term averages as investors have steadily redeployed cash into markets.

Investors aren’t hiding in cash; they are already leaning into risk. That matters because every IPO requires buyers and those buyers need funding.

Sometimes that funding comes from new money, and sometimes it comes from selling something else.

That’s why I’m not entirely convinced that Friday’s selloff was solely about interest rates.

A $75 billion IPO doesn’t happen in a vacuum.

Large institutions and individual investors don’t find billions of dollars under couch cushions. They raise liquidity by selling other assets, like stocks. Mutual funds, hedge funds, advisory firms, and retail investors are all in search of new money to make a buy in SpaceX.

Somebody sells something to buy something; that’s simply how the IPO market works.

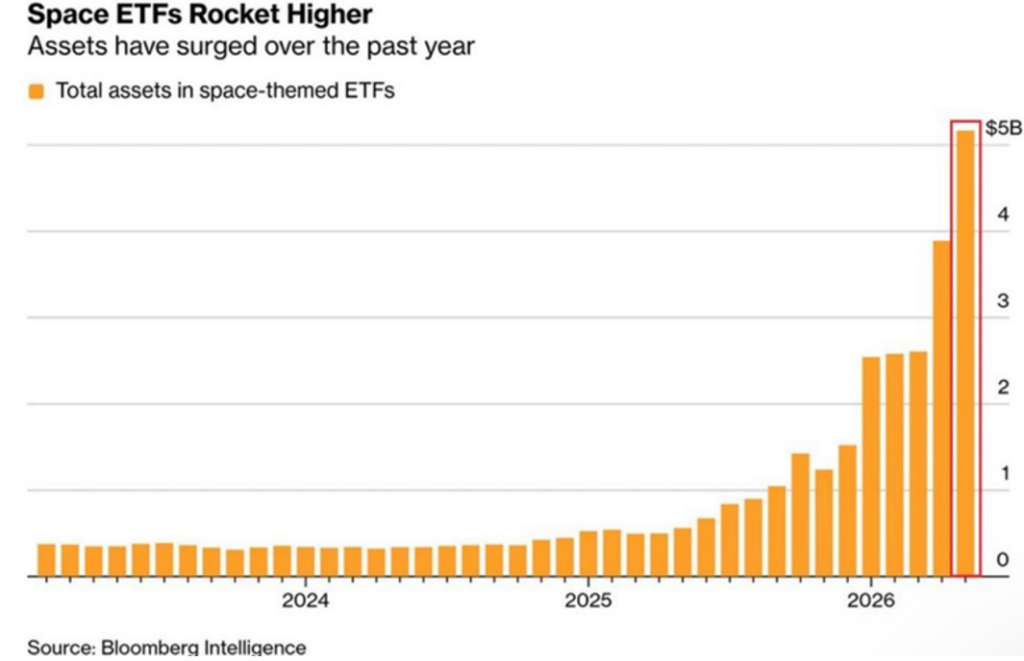

And there is evidence that enthusiasm is already building. Assets in space-themed ETFs have exploded higher over the past year.

Whenever investing starts feeling obvious, I become more curious.

Retail participation is also approaching historically elevated levels. More evidence that they need to sell things to buy things.

Retail investors have correctly identified many great companies over the last decade.

But elevated participation often signals that a story has moved beyond institutional investors and into the public imagination. And once a story enters the public imagination, expectations begin rising rapidly.

That’s where history becomes useful.

Looking at some of the largest IPOs ever completed, the average first-year drawdown has been approximately 33%.

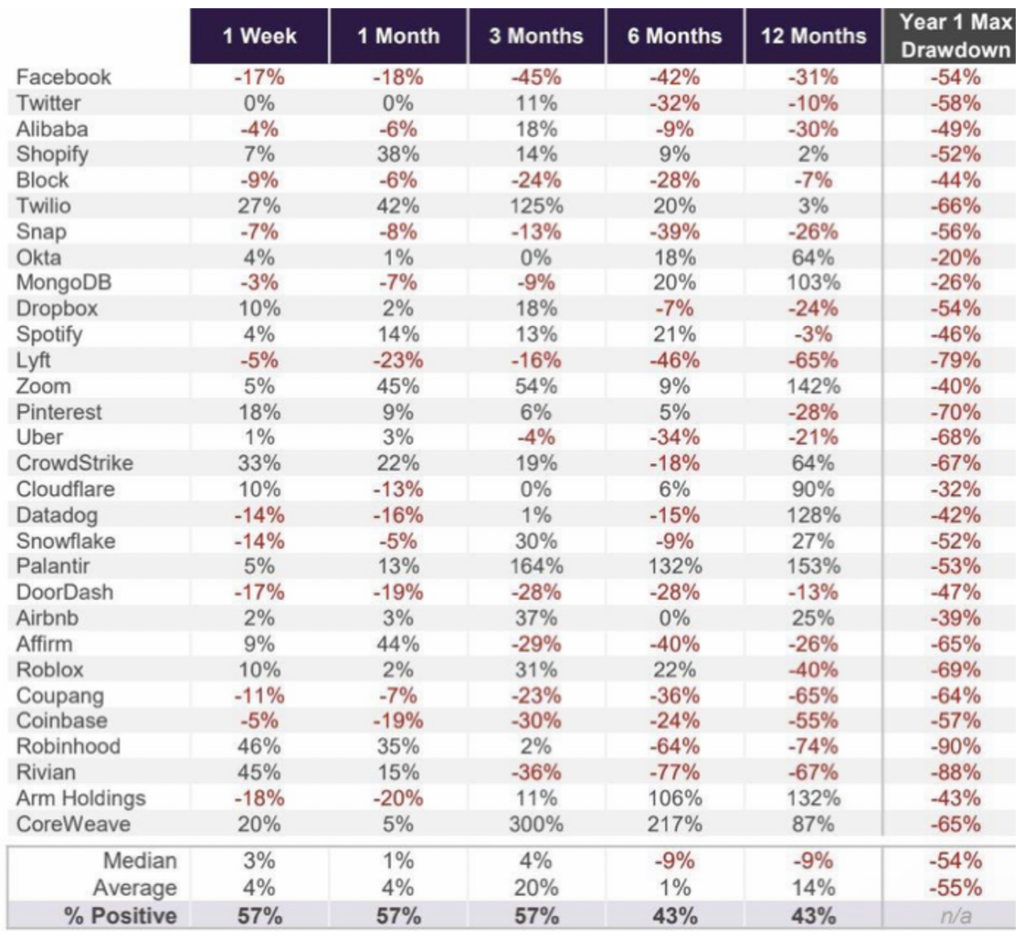

Among more recent technology IPOs, the average first-year decline becomes even more dramatic. Many of the most successful companies of the last decade experienced drawdowns of 40%, 50%, or even 70% shortly after going public.

Think about that for a moment. Many eventually became successful investments and generated tremendous shareholder wealth.

Yet investors who bought during the initial excitement often experienced significant pain first.

Again, both things can be true. The company can be extraordinary, and the stock can still become temporarily overvalued.

That’s the lesson investors have learned repeatedly throughout history.

Railroads. Telegraphs. Automobiles. Airlines. The internet. Artificial intelligence. And now commercial space.

The technology wins, and society wins.

The question investors must answer about SpaceX is whether today’s price already assumes all of that success.

As we head into what may become the largest IPO ever completed, I find myself less interested in whether SpaceX is a great company.

That answer seems obvious.

I’m more interested in whether the excitement surrounding SpaceX has already become part of the price. Because once an opportunity becomes obvious to everyone, the story itself often becomes part of the valuation.

And that’s where investing gets difficult.

SpaceX may ultimately become one of the greatest companies ever built. History simply reminds us that buying a great company and buying a great theme or investment are not always the same thing.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

Renaissance Capital; DealRoom; Bloomberg Intelligence; Charles Schwab; University of Florida IPO Database; Yahoo Finance; S&P Dow Jones Indices.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.