Every summer, millions of people do something that would make a rational economist scratch their head. They log onto Amazon and fill a virtual cart with things they didn’t know they needed 15 minutes earlier, because interest rates fell that morning. It isn’t because they suddenly became wealthier overnight.

They buy because life goes on. The economy isn’t driven by one grand decision. It’s built on millions of ordinary decisions made by ordinary people who keep moving forward.

That’s why I spend far more time watching what consumers do than what they say.

The headlines over the past few months have painted a cautious picture. Consumer confidence remains subdued. Yet consumers continue to do what they’ve done throughout most of this expansion: they find ways to spend.

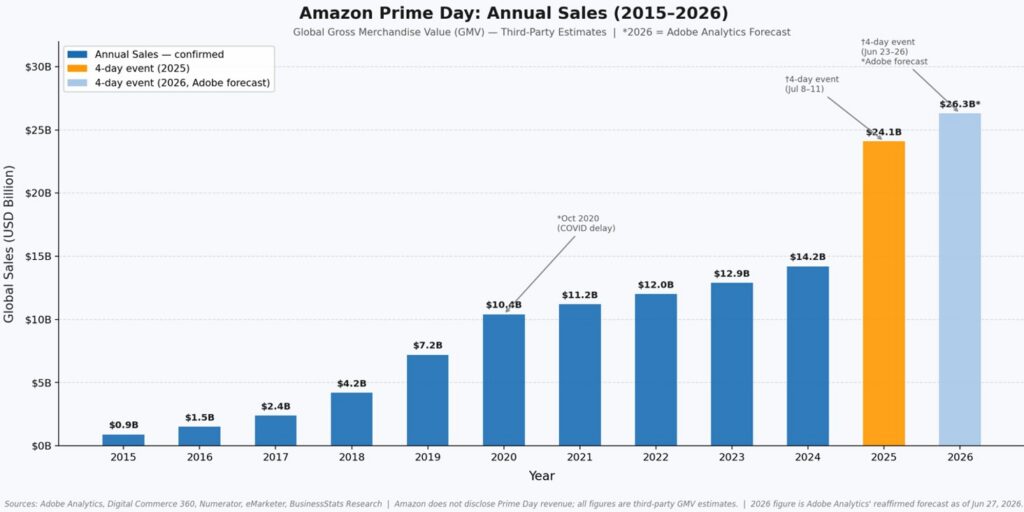

Adobe is forecasting Amazon Prime Day sales of roughly $26.3 billion this year, another record despite already enormous scale. That’s remarkable because Prime Day has become less about bargain hunting and more about a real-time measure of household willingness to open the wallet.

The same story is showing up well beyond Amazon.

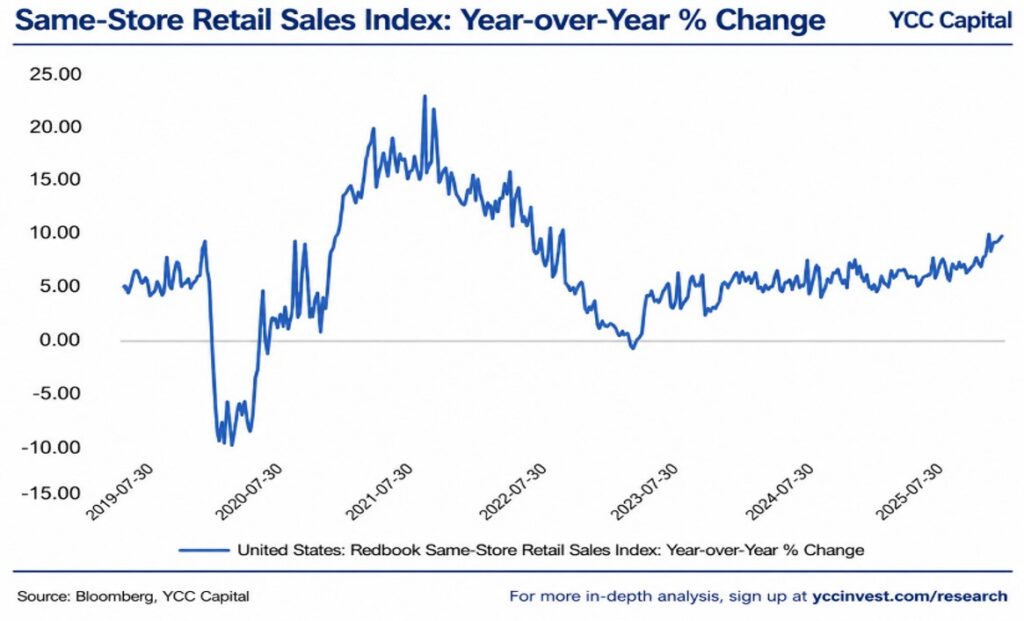

Redbook’s same-store retail sales have accelerated back toward 10% year-over-year, suggesting retailers continue to see healthy traffic despite years of inflation and elevated borrowing costs.

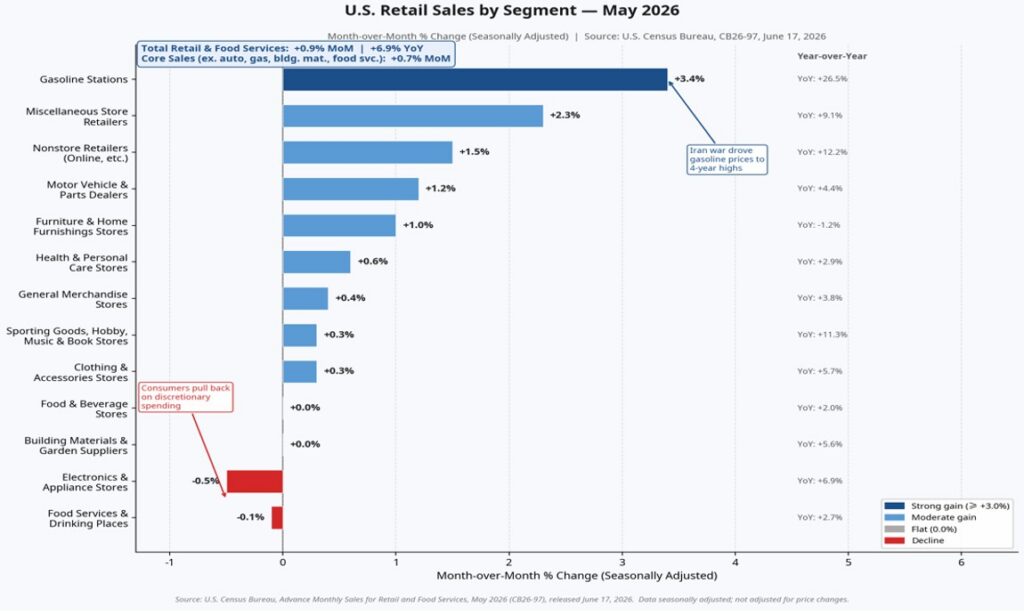

May retail sales reinforce that picture. Overall spending rose 0.9% month over month, with particularly strong gains in online retailers, autos and general merchandise. Some categories, like restaurants and electronics, softened modestly, but consumers didn’t stop spending—they simply shifted where they spent.

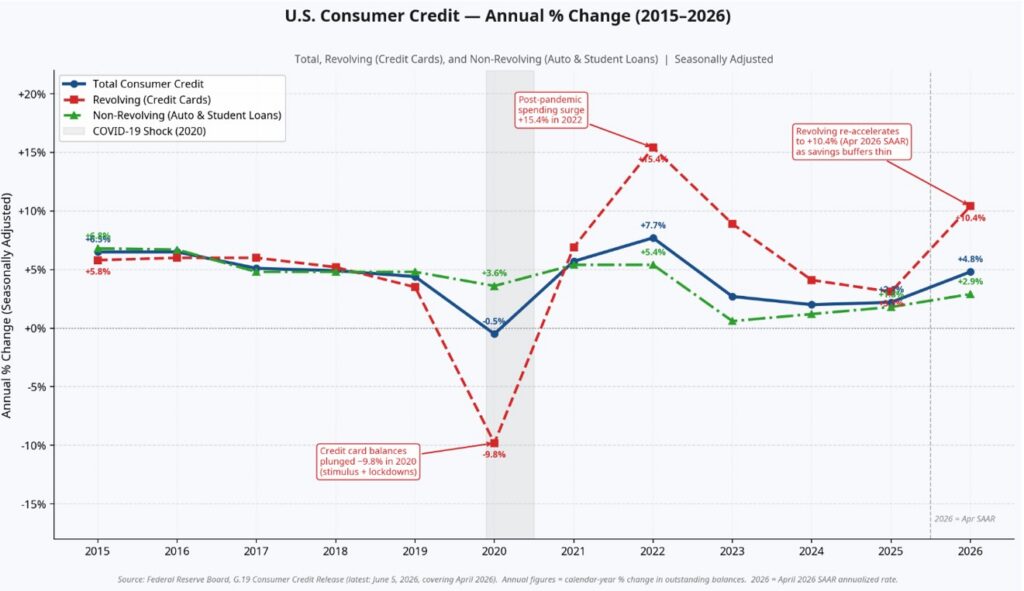

One concern I hear frequently is that consumers are simply financing this spending with credit cards. That’s partially true but not completely so.

The data tells a more balanced story.

Credit card balances have accelerated this year, but total consumer credit growth remains well below the post-pandemic surge. Revolving credit is rising and that is a point of concern, but as I said I’d be looking at overall consumer credit (blue line), vs revolving credit (red line).

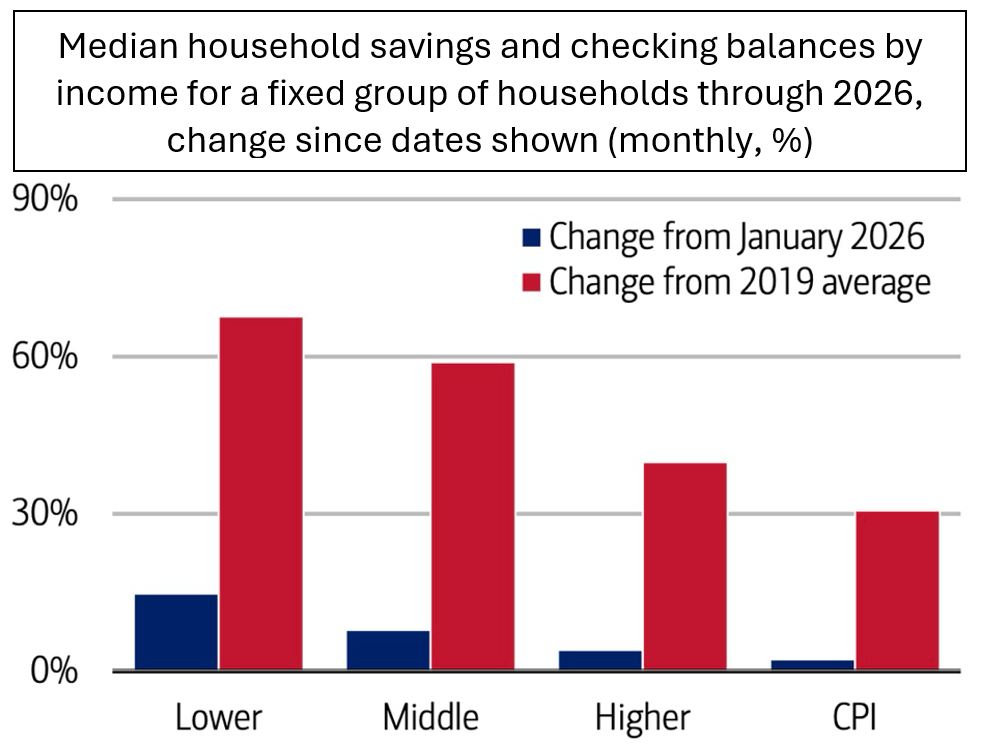

In fact, one of the more overlooked charts this month came from Bank of America. Even after several years of inflation, median checking and savings balances remain well above 2019 levels across every income group. Lower-income households have seen the greatest drawdown recently, but cash balances are still materially higher than before the pandemic.

Consumers are spending because they still have resources available, not simply because they’re borrowing recklessly.

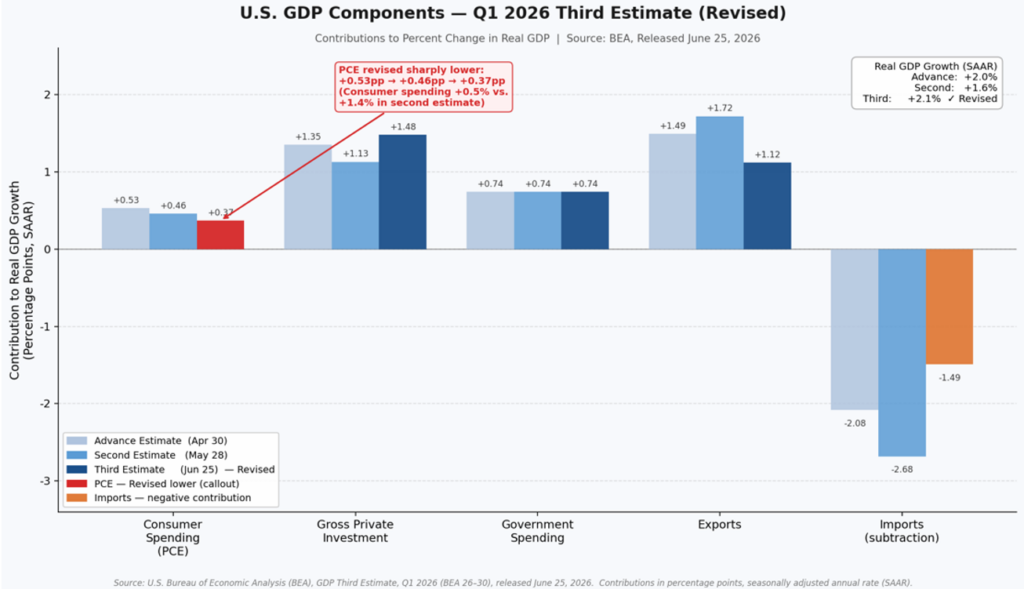

That matters because consumer spending accounts for roughly two-thirds of U.S. GDP. The latest GDP revision illustrates this relationship perfectly. Consumer spending was revised lower for the first quarter but only slightly. It’s my expectation that consumer spending will revise higher in Q2, especially if the April retail-sales data and Amazon Prime Day data persist.

This is also why corporate earnings have remained surprisingly resilient.

Companies cannot grow revenues indefinitely without customers willing to spend. Despite persistent recession forecasts over the last two years, consumers have continued supporting sales, allowing companies to protect margins and deliver stronger earnings than many expected.

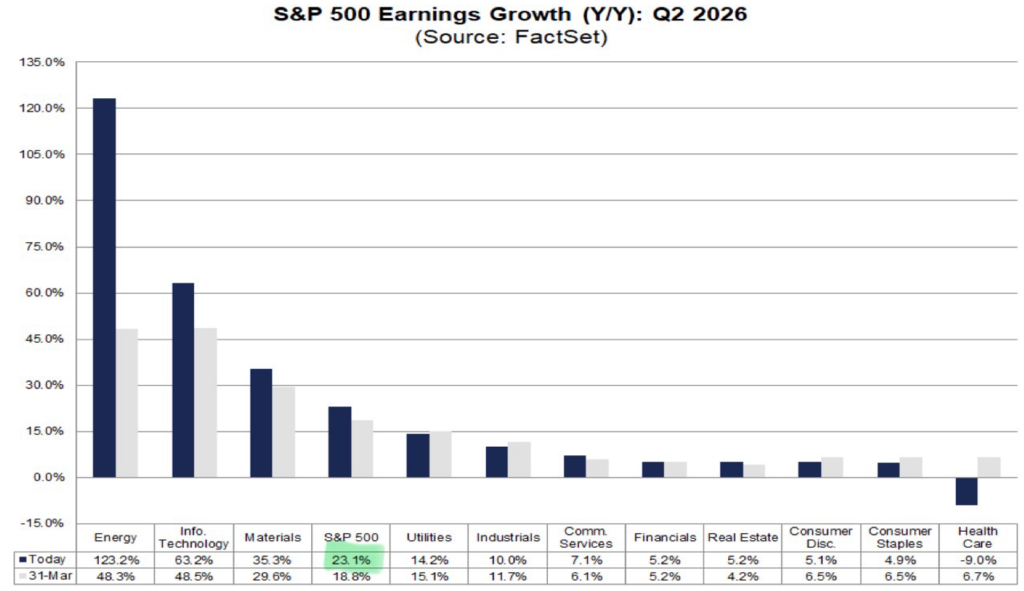

As we enter the second-quarter earnings season, expectations remain constructive. Current forecasts call for approximately 23% year-over-year earnings growth for the S&P 500, led by Energy and Technology but supported across most sectors.

Markets rarely move because the headlines sound good. They move because reality turns out better, or worse, than investors expected.

For much of the past two years, expectations for the U.S. consumer have been remarkably low. Yet month after month, households continue to spend, businesses continue to invest, and corporate America continues to earn.

That doesn’t eliminate risks. Consumer credit deserves monitoring. Lower-income households are feeling more pressure than higher-income households. Valuations remain elevated. None of those concerns should be ignored.

But investing has always required separating the narrative from the evidence.

Right now, the evidence continues to suggest the American consumer hasn’t quit. And as long as consumers keep finding reasons to spend, they remain one of the strongest foundations supporting GDP growth, corporate earnings, and ultimately equity markets.

If you have questions or comments, please let us know. You can contact us via X and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Sources & Data References:

Sources: Data referenced in this commentary includes Adobe Analytics, Amazon Prime Day historical sales estimates, U.S. Census Bureau Retail Sales Report, Federal Reserve G.19 Consumer Credit Report, Bank of America Institute consumer spending and deposit data, U.S. Bureau of Economic Analysis GDP (Third Estimate), Redbook Research, FactSet Earnings Insight, Bloomberg, YCharts, and Phillips & Company Advisors’ analysis.

The charts and data presented are sourced from a combination of public domain materials and licensed data providers. Their use is intended solely for educational and analytical commentary and falls within the scope of fair use. For a representative list of sources, please click here.

The material contained within (including any attachments or links) is for educational purposes only and is not intended to be relied upon as a forecast, research, or investment advice, nor should it be considered as a recommendation, offer, or solicitation for the purchase or sale of any security, or to adopt a specific investment strategy. The information contained herein is obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed. All opinions expressed are subject to change without notice. Investment decisions should be made based on an investor’s objective.