2014 Q1 Earnings Season Scoreboard

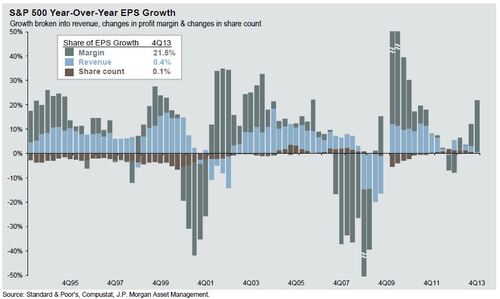

In the Phillips & Company 2014 Q2 Look Ahead, I noted that while year-over-year earnings per share (EPS) growth was strong in 2013 Q4, most of it came from margin expansion as opposed to revenue growth.[i] Companies grew profits mainly by controlling expenses.

While efficient operations are important, cost controls can only go so far as a driver of earnings. Future EPS growth will depend on higher revenues. So how are companies doing so far in 2014 Q1? Let’s take a look at the Q1 scoreboard.

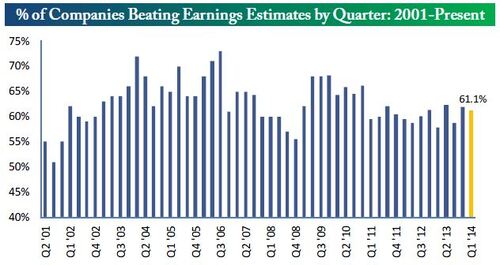

According to FactSet, of the 240 S&P 500 companies that have reported earnings, 73% have reported earnings above their mean estimate.[ii] This is in-line with recent averages. Looking beyond the S&P 500, Bespoke Investment Group found that 61.1% of around 700 companies reporting so far have beaten earnings estimates, just slightly below the 62% rate from last quarter.[iii]

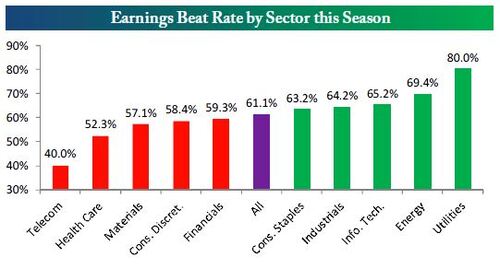

At the sector level, the Utilities, Energy, Info Tech, and Industrials sectors had the highest percentage of outperformers, while Telecom and Health Care had the highest percentage of underperformers.[iv]

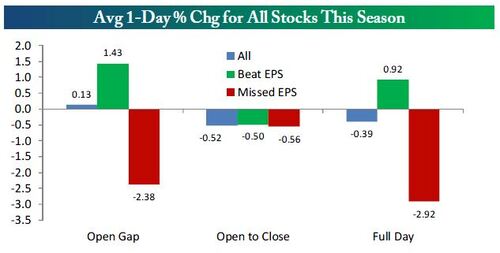

Investors have rewarded companies that beat earnings expectations a little and punished those that came up short. Interestingly, on average, share prices drifted down during the day regardless of whether the company beat or missed earnings expectations.[v]

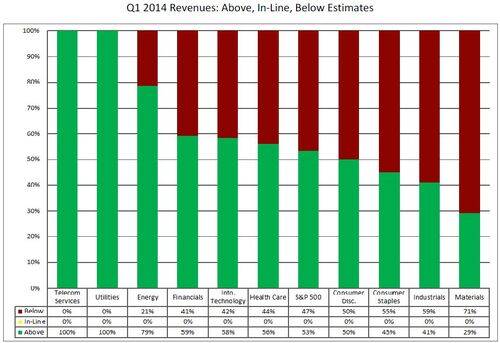

While earnings have been strong overall, revenues are not faring as well. Of the 240 S&P 500 companies that have reported, 53% have beaten sales estimates, which is below the 1-year average of 54% and the 4-year average of 58%.[vi] The Telecom, Utilities, and Energy sectors had the highest percentage of outperformers, while Materials, Industrials, and Consumer Staples had a higher percentage of revenue misses.[vii]

Two common factors mentioned for the revenue misses were the unusually cold and stormy winter weather during the first quarter and unfavorable foreign currency exchange rates caused by a strengthening US dollar.[viii] While the currency issue could continue into the future, the weather-related impact should be lifted for Q2 and perhaps even contribute a positive bump from delayed purchases.

Without higher sales, corporate earnings growth will eventually slow, as margin expansion through cost cutting can only go so far. Larger companies seem to be factoring this concern into forward guidance. FactSet reported that 36 of 51 (70%) S&P 500 companies have issued negative EPS guidance for Q2 so far, above the 5-year average of 65%.[ix] Analysts are projecting higher double-digit earnings growth in the second half of the year for an annual growth rate of 7.8%.[x]

For this strong second half finish to occur, companies will need to grow their top line sales. We will be on the lookout for signs of improving sales and indications, such as increased wages or consumer credit, that suggest the consumers’ ability to spend more and support the next leg of the economic recovery. The Q2 scoreboard in July will be an important update on the strength of our economy and the ability to grow corporate earnings.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Jeff Paul, Senior Investment Analyst – Phillips & Company

Tim Phillips, CEO – Phillips & Company (Editor)

[i] JP Morgan Asset Management (April 2014). Guide to the Markets. p. 9.

[ii] Butters, J. (Apr 25, 2014). Earnings Insight – S&P 500. FactSet. p. 3.

[iii] Bespoke Investment Group. (Apr 25, 2014). The Bespoke Report. p. 11.

[iv] Ibid. p. 14.

[v] Ibid. p. 13.

[vi] Butters, J. (Apr 25, 2014). Earnings Insight – S&P 500. FactSet. p. 3.

[vii] Ibid. p. 9.

[viii] Ibid. p. 5-6.

[ix] Ibid. p. 7.

[x] Ibid. p. 7.