A Stair Case Maze of Confusion

(Earnings Recessions, Inverted Yield Curves, and Economic Recessions)

Every few years I repurpose some old themes and remind our readers that, although past performance is not always indicative of future performance, cycles do repeat themselves.

Through 2015 and much of 2016, the United States was facing an earnings growth recession amid an economic boom. We wrote about that situation in May 2016, and you can read that post here.

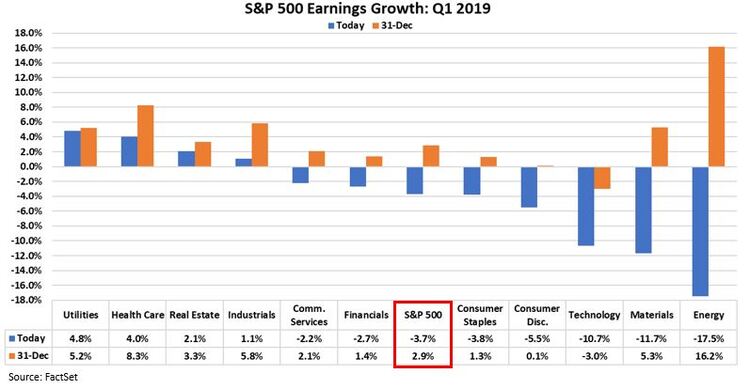

Now, five trading days from the end of Q1 2019, we face a similar predicament. Earnings growth for S&P 500 companies, according to FactSet, are anticipated to decline by 3.7 percent. [i]

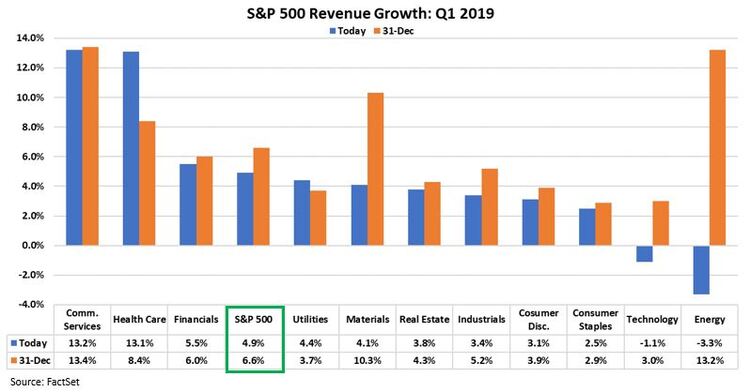

Oddly enough, with earnings growth anticipated to decline, S&P 500 companies are anticipated to grow revenues by 4.9 percent. [i]

That oddity has much more to do with year-over-year earnings comparisons versus some mysterious underlying issues within consumer demand, wages, or actual corporate profits.

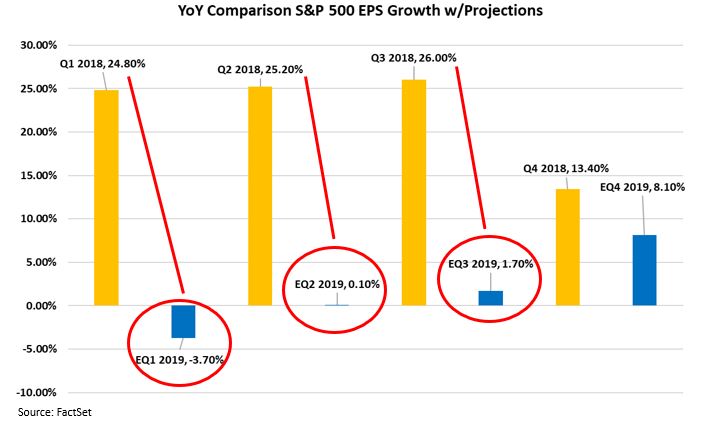

Simply review the year-over-year comparisons shown below.

You can see the corporate earnings hurdles to beat, except for Q4 2018, are all over 24 percent. Those are large numbers to beat considering the long-term average earnings per share growth rate for S&P 500 companies is 6.49 percent. [i] [ii] [iii]

Now, as we roll forward to Q2 2019 and beyond, you can start to see some analysts’ expectations for positive earnings growth resume. Those expectations follow: [i]

- Q2 2019, expectations for +0.10 percent earnings growth

- Q3 2019, expectations for +1.70 percent earnings growth

- Q4 2019, expectations for 8.10 percent earnings growth

- Full-year 2019, expectations for 3.80 percent earnings growth

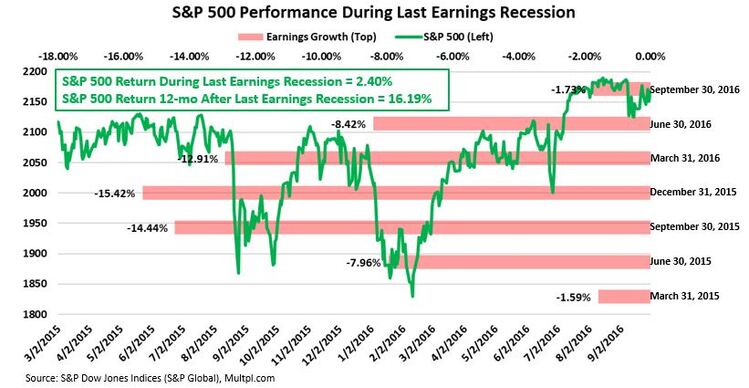

Based on those analysts’ current expectations, it’s certainly possible to see two consecutive quarters of declining earnings coming up. But markets don’t always respond negatively to such a condition, as many investors would think: look no further than the last earnings recession beginning in Q1 2015 and ending in Q3 2016. [iii] [iv]

During that time stock market returns increased 2.40 percent, while the returns for the following twelve months increased at a hefty 16.19 percent. [iv]

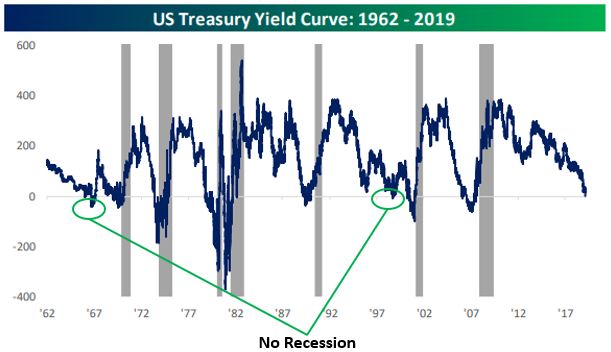

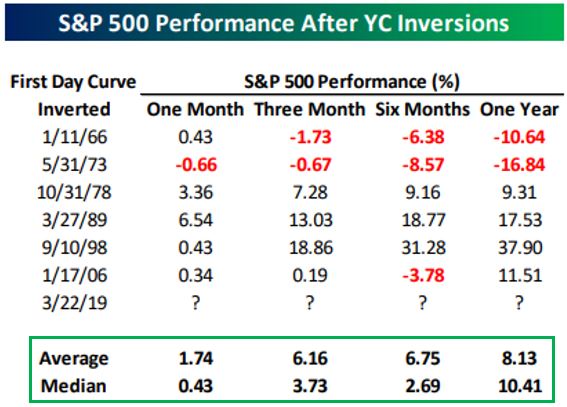

I also know that many are hearing buzz about an inverted yield curve, which typically has preceded U.S. recessions. Although that is true, according to our friends at Bespoke, not every yield curve inversion has led to a recession. [v]

On Friday, March 22, 2019, as the market was digesting the prior day’s dovish comments on the Fed’s lowered economic expectations, we saw the yield curve between the three-month treasury and the ten-year treasury invert for the first time in 3,030 days – the longest stretch on record without an inversion since 1962. But that doesn’t mean poor performance for the stock market is just around the corner. In fact, on average, one, three, six, and twelve months following a yield curve inversion, stocks are positive. [v]

With the Fed on hold for further interest rate increases (for now) along with the first signs of an inverted yield curve, many investors may be tempted to overreact to a potential earnings recession in Q1 and Q2 2019. But as the data would indicate, forward returns following such events have been positive. Any overreaction by market participants may be a great buying opportunity for long-term investors.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_032219.pdf

ii. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_122118.pdf

iii. https://www.multpl.com/s-p-500-earnings-growth/table/by-quarter

iv. https://us.spindices.com/indices/equity/sp-500

v. https://www.bespokepremium.com/get/The_Bespoke_Report_032219.pdf (Subscription Required)