China Syndrome

In today’s investment landscape, the specific focus on China has leapt to the top of the list. The nonstop trade-war rhetoric between the United States and China is driving this focus. Those talks are ongoing but are expected to conclude before the end of March.

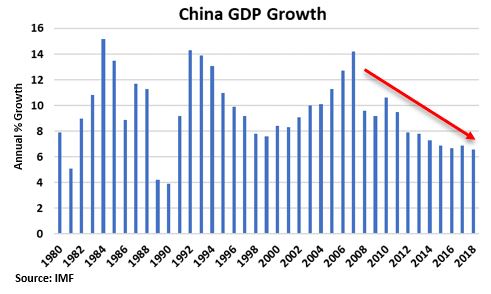

In the meantime, China has been experiencing a significant slowdown in its rapid pace of economic growth. Some call it the largest slowdown in the past thirty years. [i]

Before we go on, it’s important to note a few critical facts about China’s economy.

First, China is the world’s second largest importer behind the United States. [ii]

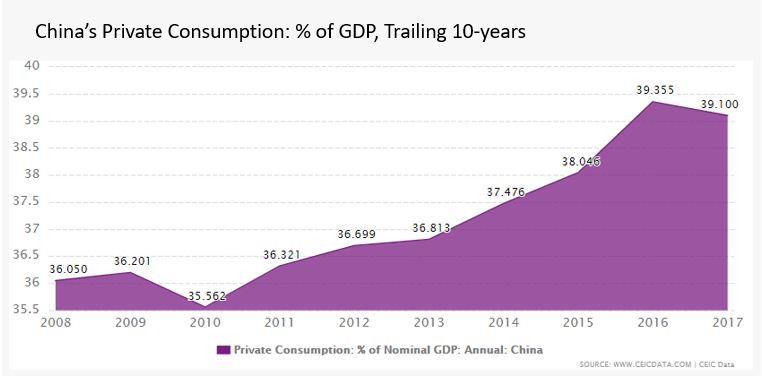

Second, China is in the process of systematically converting its economy from a large capital-expenditure-focused economy to an American-style, consumption-driven economy. [iii]

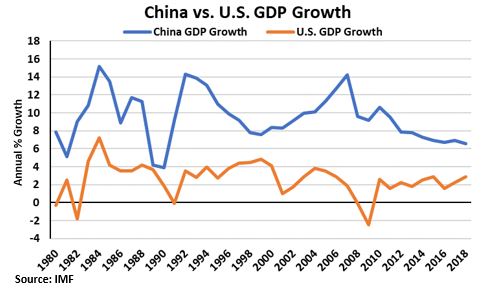

And third, China’s GDP growth is still twice that of the United States. [i]

China’s slowing growth is a critical issue for investors to pay attention to, and perhaps, profit from.

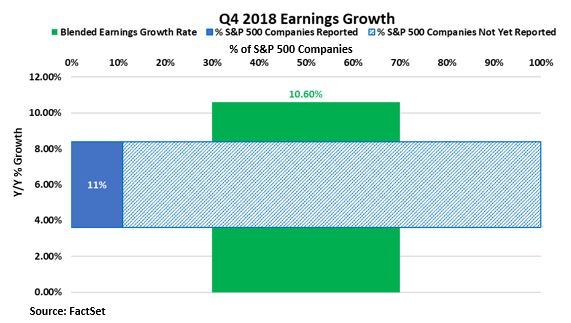

As of Friday, January 18, 2019, 11 percent of S&P 500 companies have reported their Q4 2018 earnings numbers. The blended earnings-per-share growth rate so far is coming in at 10.6 percent. [iv]

And according to FactSet, this would mark the fifth consecutive quarter of double-digit earnings growth. [iv]

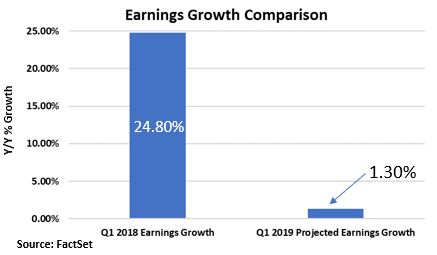

However, be aware that Q1 2019 earnings expectations call for 1.3 percent growth. [iv]

This is being compared with Q1 2018, which posted one of the strongest earnings growth rates ever at 24.80 percent. [iv] [v]

Nonetheless, China appears to be having an impact on earnings growth for many major companies. Look no further than companies like Apple and Ford Motors.

Based on a New York Times article, Apple stock has had one of its worst months since 2014, citing the primary contributor as weaker-than-expected demand for its iPhones in China. The same article also stated that Ford Motors cut output at its Chongqing joint venture by 70 percent in November, in what Ford says was a move to reduce inventories of unsold cars. [vi] [vii] [viii]

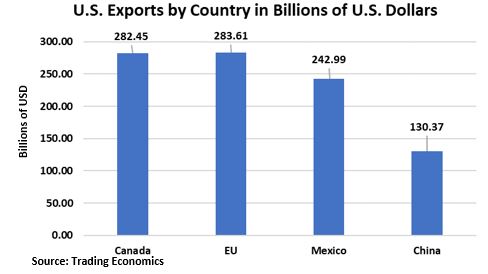

However, the downturn in China’s GDP growth may not be as big an issue as many are making it out to be. China’s $130 billion in exports it receives from the United States is only 8.6 percent of the United States total exports. Compared to the other regions that make up a larger share of the United States exports, the effects from China may be overplayed. In fact, the European Union, Canada, and Mexico, all dwarf China when it comes to the United States export market. [ix]

The fact still remains that earnings growth is slowing, and that was to be expected in 2019. Blaming it all on China may be convenient, but it’s factually inaccurate.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://www.imf.org/external/datamapper/NGDP_RPCH@WEO/CHN/USA

ii. https://www.visualcapitalist.com/visualizing-the-worlds-largest-importers-in-2017/

iii. https://www.ceicdata.com/en/indicator/china/private-consumption--of-nominal-gdp

iv. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_011819A.pdf

v. https://insight.factset.com/sp-500-likely-to-report-earnings-growth-above-20-for-second-straight-quarter

vi. https://www.nytimes.com/2019/01/20/business/china-economy-growth-davos.html

vii. https://finviz.com/quote.ashx?t=aapl&ty=c&ta=1&p=d

viii. https://finviz.com/quote.ashx?t=f&ty=c&ta=1&p=d

ix. https://tradingeconomics.com/united-states/exports-by-country