Clash of the Market Titans

Investors have been working new funds into both equities and fixed income. Yet these two markets are forecasting widely different outcomes for the future of the U.S. economy. Ultimately, like any clash of two titans, only one of them will win. [i]

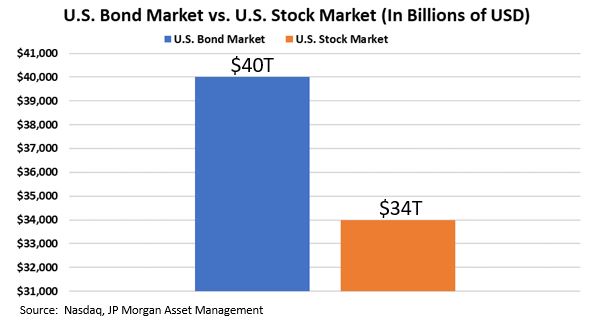

As many fables go, the odds of a victory usually lay on the side of the giant, only to be upset by the unexpected underdog. In this story, the giant is the U.S. bond market, weighing in at 15 percent heavier, leaving the underdog to be the U.S. stock market. [ii] [iii]

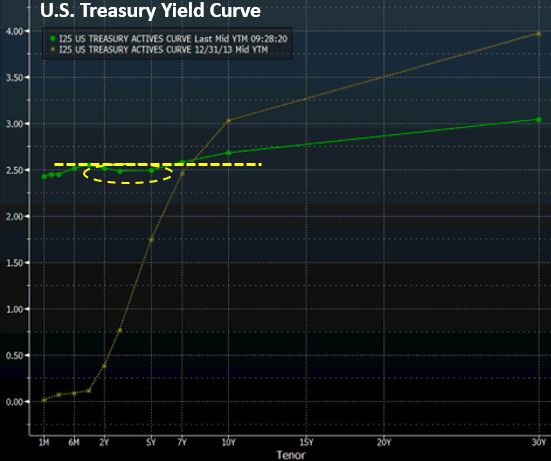

Currently, the bond market (often referred to as the “smart money”) is not trading as if it’s reflecting the same growth for the U.S. as the equity market is. In fact, the bond market is forecasting quite the opposite. Current Treasury yields imply an inflection point, leading to slower growth as the curve continues to invert. [iv]

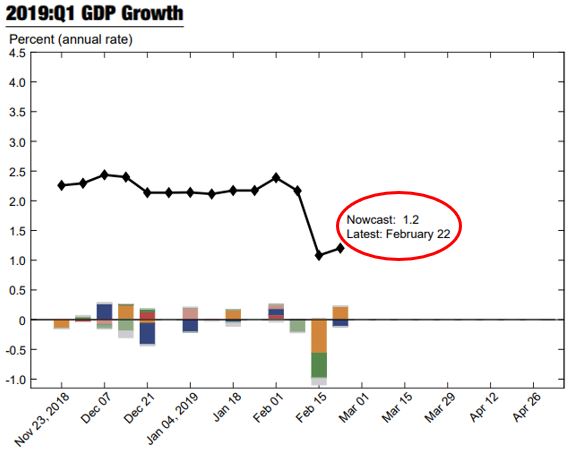

This data is now finding its way into revisions for Q1 GDP growth. The Federal Reserve Bank of New York now forecasts Q1 GDP growth at an annual rate of 1.2 percent. If this forecast is correct, this would be the lowest GDP growth for any quarter since 2015. [vii] [viii]

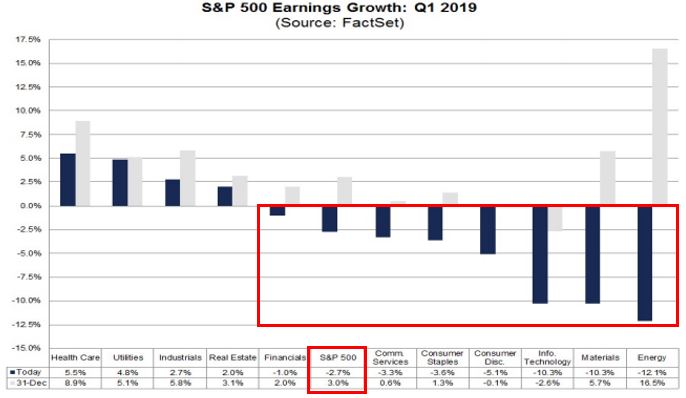

These downward revisions have also found their way into the forecasts for corporate earnings growth. Just look at the revisions between December 31, 2018, and February 22, 2019, from FactSet. Corporate earnings for Q1 2019 are expected to be negative for the first time since 2016. [ix]

However, the equity markets paint a completely different picture of future growth. Stocks have been on a euphoric high since the low point on the S&P 500 during the worst December since the Great Depression. Since the low on December 24, 2018, stocks are up 18.78 percent, one of the best starts to a year in quite some time. [iv]

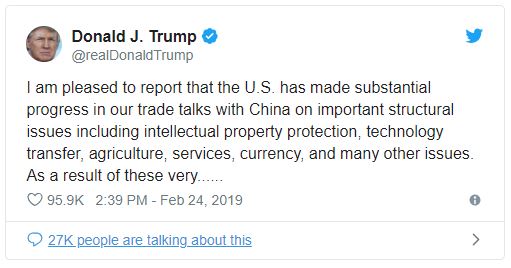

The equity market euphoria has been driven by the idea that a trade deal between the U.S. and China will curtail any potential slowdown in GDP and continue to provide fuel for corporate earnings growth. The likelihood of a U.S.-China trade agreement becomes more front and center as tweets from the White House show continued progress toward an amicable agreement. President Trump’s positive tone was echoed by President Xi Jinping to his home country, igniting the best day for Chinese stocks in more than three years. [v] [vi]

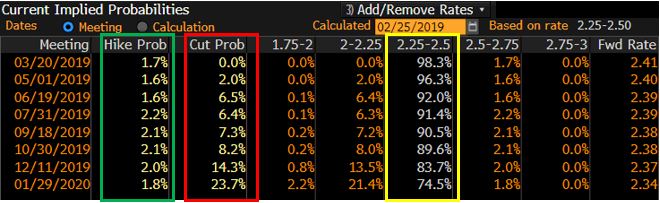

The odds may also be shifting in favor of stocks as the U.S. Federal Reserve continues its dovish stance on future restrictive monetary policy. In fact, the market is now pricing in zero rate increases for the Fed Funds rate in 2019. Furthermore, the market places a higher probability on a rate decrease than on an increase. [iv]

Following Chairman Powell’s latest comments on global growth, a common theme many analysts are pointing to is the potential for the Fed to halt the normalization of its balance sheet. By doing this, the Fed would then purchase enough securities to maintain the size of its current balance sheet. This would mean purchasing the same amount as what is maturing (rolling of the balance sheet). In other words, rather than removing liquidity from the market, the Fed would be providing a level of liquidity, which would further benefit equities. [x]

At this point, the answer isn’t clear, and it would be too difficult to assess which titan will come out on top. What I do know is that one of these markets will be correct in the end. For now, the best course of action is to hope for the best, but prepare for the worst. Make sure you’re not overextending your risk in any one direction while these two market giants battle it out in this epic tale.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://bit.ly/2SqaKH6

ii. https://www.nasdaq.com/article/us-stock-market-is-biggest-most-expensive-in-world-but-us-economy-is-not-the-most-productive-cm942558

iii. https://am.jpmorgan.com/blob-gim/1383407651970/83456/MI-GTM_1Q19_Linked.pdf?segment=AMERICAS_US_ADV&locale=en_US

iv. Bloomberg L.P.

v. https://twitter.com/realDonaldTrump/status/1099800961089003522

vi. https://www.cnn.com/2019/02/25/investing/us-and-china-trade-war-stocks/index.html

vii. https://www.newyorkfed.org/medialibrary/media/research/policy/nowcast/nowcast_2019_0222.pdf?la=en

viii. https://www.statista.com/statistics/188185/percent-chance-from-preceding-period-in-real-gdp-in-the-us/

ix. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_022219.pdf

x. https://www.bloomberg.com/opinion/articles/2019-01-31/the-fed-s-bold-step-toward-main-street