Earnings Outlook

Earnings Outlook

Weekly Market Commentary 7-15-2013

Tim Phillips, CEO—Phillips & Company

Earnings season is starting, and as we have written about in the past, earnings are what really drive stock prices.

Expectations for this earnings season are somewhat cautious. According to Thomson Reuters:

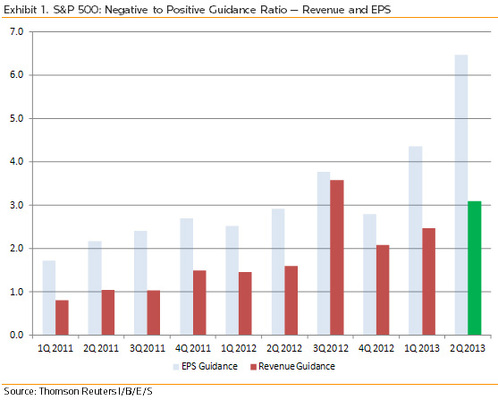

“So far, S&P 500 companies have issued 97 negative earnings preannouncements and only 15 positive ones, for a negative to positive ratio of 6.5.”[i]

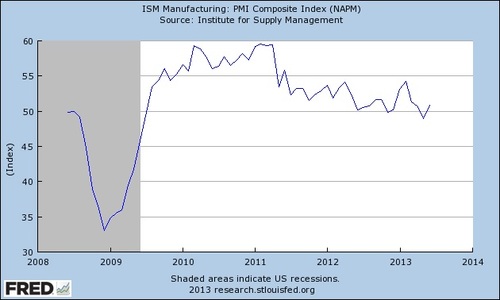

Businesses are indeed cautious. The Institute for Supply Management (ISM) puts together an indicator called the Purchasing Managers Index, which tracks inventory levels, new orders, and other indicators of health in the manufacturing sector.

Whenever the index is below 50, it is a sign of contraction. In May, the index was at 49.0, showing a slowdown in manufacturing. The most recent report released a few weeks ago showed the index rebounded to 50.9 in June, but this is still a borderline reading.[ii] You can see in the chart below that the index has been hovering around 50 for some time.[iii]

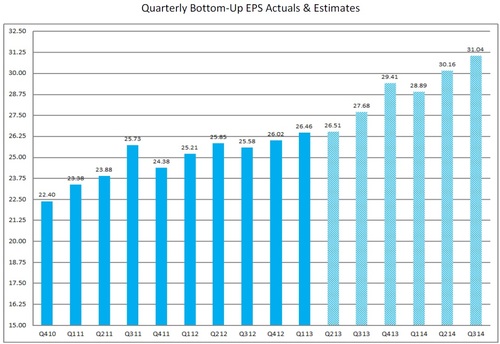

In aggregate, quarterly earnings per share expectations on S&P 500 stock are for new highs of 26.51, and growth of 2.55% from Q2 of last year.[iv]

Sector breakdown

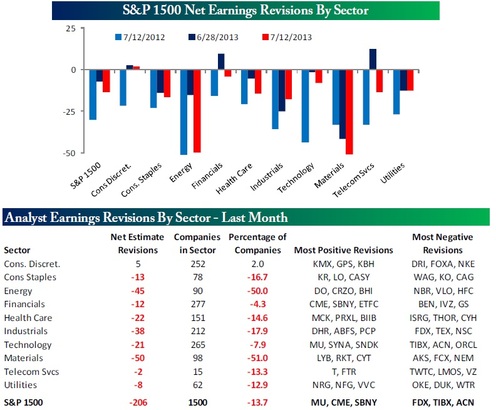

Analysts have revised down earnings estimates for nearly every sector, as you can see below.[v]

The sectors with the greatest amount of downward revisions are energy and materials. This could be a sign of a contracting global economy, if businesses slow down and use fewer raw materials in their manufacturing. I say global economy instead of just saying a contracting US economy, since much of the demand in recent years for energy and materials has been driven by China.

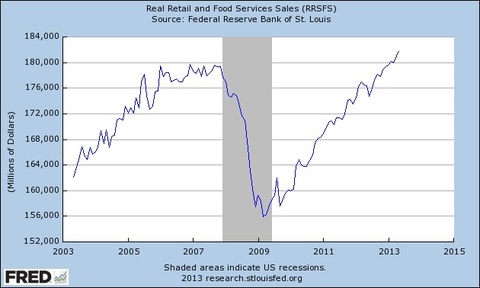

On the good side, consumer discretionary was interestingly one sector that stood out as actually having positive net revisions. We have indeed seen consumers start to spend, as we wrote about last week, and as we have seen in economic data. Real spending (inflation-adjusted) on retail and food services have reached pre-recession levels, as you can see below.[vi]

Some key earnings releases to monitor are Exxon Mobil on August 1, Freeport-McMoRan on July 23, and Nordstrom on August 15. Beyond just the actual earnings numbers, the management commentary and forward outlook will help give us insight into whether or not energy and materials are slowing, and also insight into how strong the consumer is really.

Conclusion

The last time that we saw this level of negative to positive earnings revisions was December 2012.[vii] Since then, the S&P 500 has rallied 19.18%.[viii] While negative preannouncements and negative estimate revisions could be a sign of caution, it could also be a chance for the market to rally if companies end up beating the (low) expectations.

Expect continued volatility ahead, and we continue to recommend splitting the fence between growth and quality.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Alex Cook, Investment Analyst – Phillips & Company

[i] Earnings Roundup: Negative revenue guidance foreshadows weak top-line growth”, Thomson Reuters Alpha Now, July 1, 2013

[ii] “June 2013 Manufacturing ISM Report On Business”, Institute for Supply Management, July 1, 2013

[iii] “ISM Manufacturing: PMI Composite Index”, Federal Reserve Economic Data

[iv] “Earnings Insight”, FactSet, July 12, 2013

[v] “Earnings Revisions”, Bespoke Investment Group, July 12, 2013

[vi] “Real Retail and Food Service Sales”, Federal Reserve Economic Data

[vii] “Earnings Preview: Q2 earnings season gets into high gear”, Zacks, July 12, 2013

[viii] Bloomberg LP