High Hurdles!

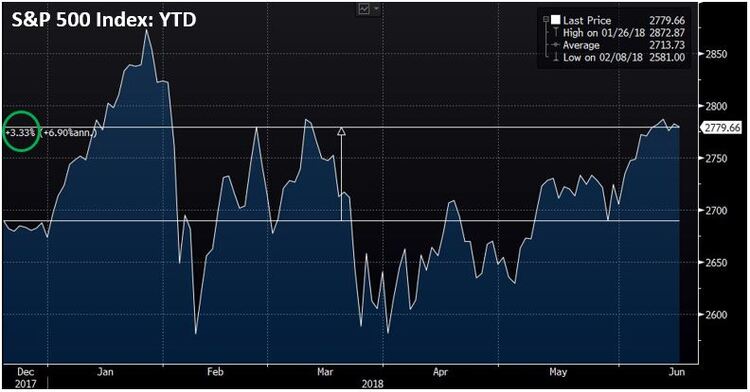

U.S. equity markets have remained relatively flat year-to-date, despite the phenomenal corporate earnings we’ve seen this year. Just consider this: The S&P 500 index is up 3.33 percent. [i]

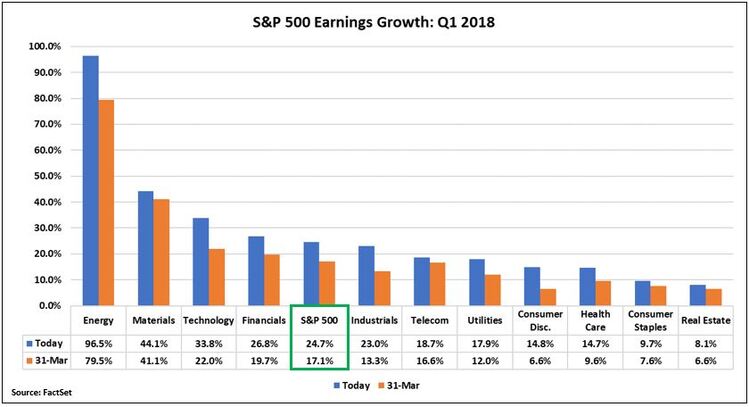

All the while, earnings per share growth in Q1 came in at more than 20 percent. [ii]

The outcome from this combination of low price appreciation and strong corporate earnings growth is a reduction in valuations. The S&P 500 Forward P/E ratio has dropped from a peak of 20.05 to its current level of 17.45, representing a 2.6 percentage point drop, or, in other words, a 12.96 percent decline. [i]

The outcome from this combination of low price appreciation and strong corporate earnings growth is a reduction in valuations. The S&P 500 Forward P/E ratio has dropped from a peak of 20.05 to its current level of 17.45, representing a 2.6 percentage point drop, or, in other words, a 12.96 percent decline. [i]

In my assessment, all of this is healthy in maintaining stable markets, regardless of the rash of geopolitical turmoil and disruption scattered throughout the news headlines.

The question now, in front of many investors, is what will keep this good going?

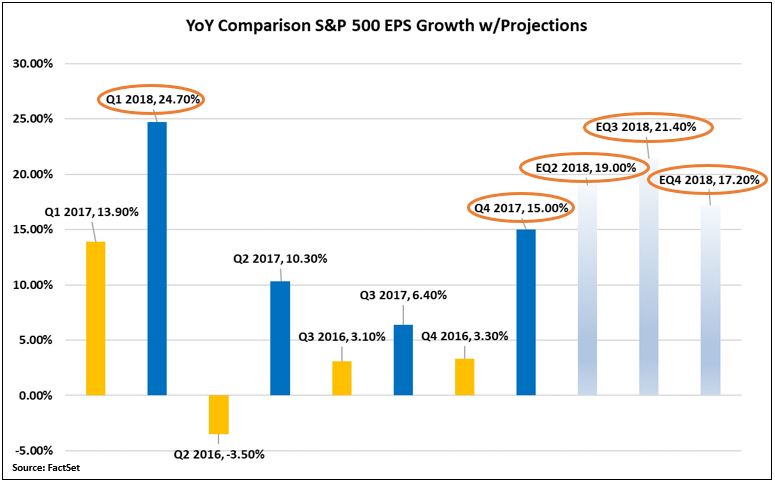

First, consider that in Q1 2019, many of the companies in the S&P 500 will need to overcome the hurdle rate set by the enormous Q1 2018 corporate earnings growth just to keep pace with 2018’s phenomenal numbers. Furthermore, if earnings growth is close to what is forecast for the remaining quarters of 2018, those hurdle rates don’t seem to get any easier to clear. [ii]

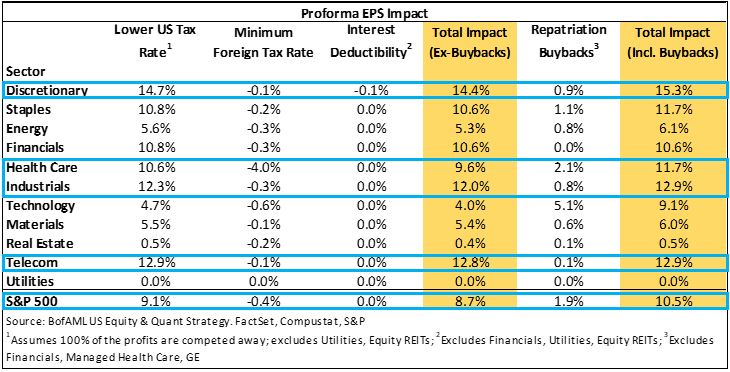

And because tax reform is estimated to contribute 10.5 percentage points to overall earnings growth for S&P 500 companies in 2018, these hurdle rates are even more difficult to overcome beginning in 2019. [iii]

Thinking ahead, we will likely need significant catalysts to fuel this kind of corporate earnings growth much higher in 2019 and beyond.

So, what might these catalysts be? There are really two main drivers beyond the strength in the American consumer that can help companies maintain EPS growth.

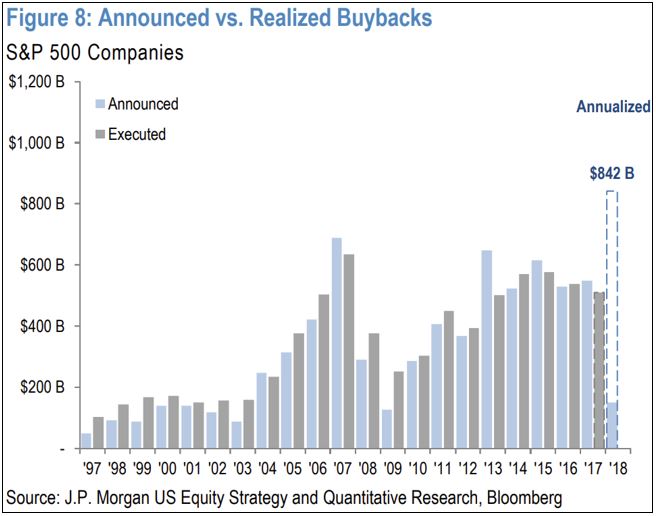

The first is share buybacks. This type of financial engineering can add a significant amount of fuel to EPS growth. In its simplest form, companies that are buying back shares, are shrinking the number of shares in circulation relative to the company’s earnings, which in turn increases earnings-per-share.

In fact, according to data provided by JP Morgan, companies are taking advantage of share buybacks at levels never before seen, which is something that we pointed out in our Q1 2018 Look Ahead. [iv]

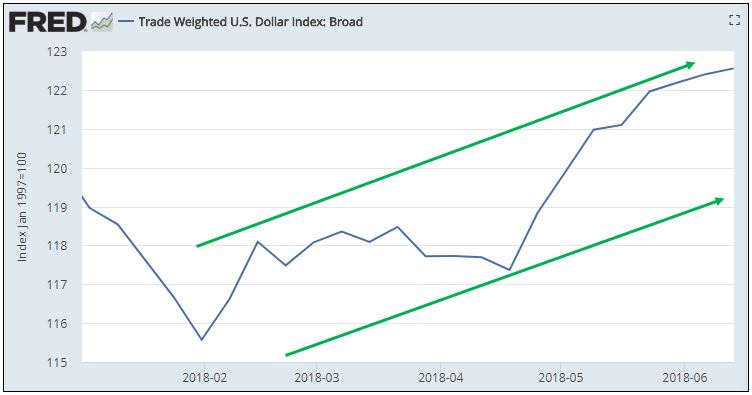

The second is the U.S. dollar. A weakening U.S. dollar helps export-driven companies compete in the global trade economy. Considering S&P 500 companies generate 39 percent of their revenues internationally, the U.S. dollar has more and more become a stronger catalyst. [ii]

The U.S. dollar has been strengthening in 2018, but any weakness in the coming quarters could be an additional contribution to EPS growth for many of the S&P 500 companies and certainly a catalyst that could help elevate future EPS growth above 2018 hurdles going forward. [v]

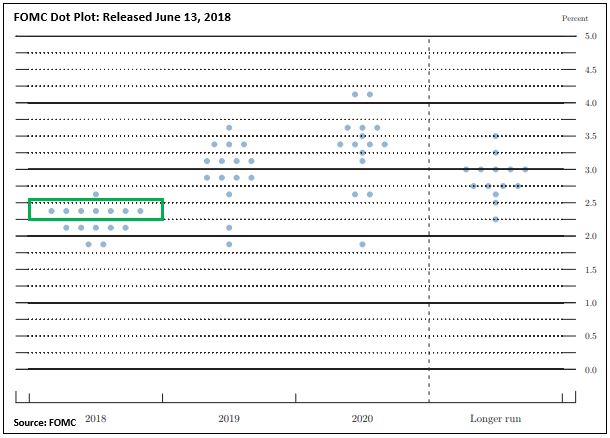

Keep in mind, that none of this suggests equity markets will move much higher, especially in the face of rising interest rates alongside a Federal Reserve that continues to raise interest rate guidance for 2018. [vi]

After last Wednesday’s FOMC meeting, where the Fed hiked interest rates another quarter point to 1.75 percent, the median forecasted Fed Funds Rate for 2018 by the members of the FOMC sits between 2.25 – 2.50 percent, which would indicate another two rate hikes this year, for a total of four. [vi]

While I don’t anticipate an economic recession in the coming twelve months, without earnings-per-share growth in 2019, we could certainly see a period of consolidation in U.S. equity markets. Let’s just hope that share buybacks and a weakening dollar can keep the good going as we try to jump some tall hurdles.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. Bloomberg, L.P.

ii. https://insight.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_061518A.pdf

iii. https://phillipsandco.com/files/9615/1519/3009/Look_Ahead_2018Q1_-_Final.pdf

iv. https://www.bloomberg.com/news/articles/2018-03-02/-800-billion-buyback-guess-is-latest-bombshell-in-tax-cut-debate

v. https://fred.stlouisfed.org/series/TWEXB

vi. https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20180613.pdf