Is It Time to Reflect?

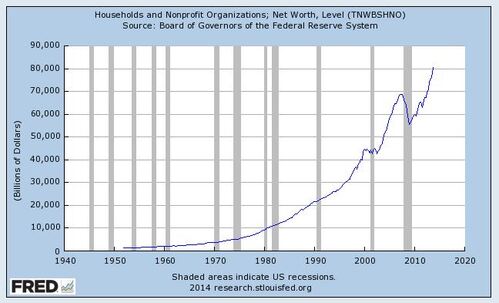

On Thursday, the Fed released its quarterly net worth statistics for American households and nonprofit organizations.[i]

The data suggests that household net worth is now at record levels, over $10 trillion above 2008 levels, thanks to gains from stock, bond, and real estate investments. Further, recent credit card data from the Survey of Consumer Finances indicates that U.S. households have been deleveraging.

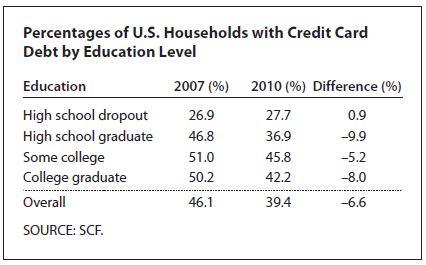

Overall, fewer U.S. households have credit card debt, though there was a slight increase among high school dropouts.[ii]

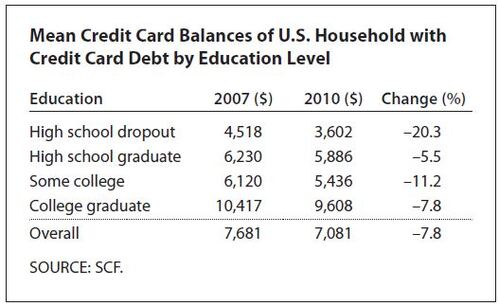

However, the average balance for households with credit card debt decreased 7.8% on average from 2007-2010 for all educational cohorts.[iii] This occurred despite U.S. median household income decreasing by only 2 percent and personal disposable income increasing by around 7 percent during this time period.[iv] Consumers reacted to concerns about the economy and their future income by saving more and spending less, resulting in more assets and less liabilities.

If Americans choose to take advantage of their newfound financial strength, this could bode well for our consumption-driven economy.

From an investment perspective and the nearly 30 years of managing wealth for others, this is the time for investors to look in the mirror. You may have made one or more of the following statements in the past months:

- "My portfolio was not up that much last year."

- "My advisor (or portfolio) is too conservative."

- "I want to take more risk."

We believe that on-going conversations about your changes in circumstance are healthy. Aligning your portfolio with your goals, financial strength, risk tolerance, and time horizon is valuable. However, if you are reacting to the monster year that the S&P 500 had and want to chase returns, such market timing will generally hurt your portfolio’s performance. Heed Warren Buffett’s words of wisdom in his recent letter to shareholders:[v]

- “…To achieve satisfactory investment results…follow a course certain to work reasonably well. Keep things simple and don’t swing for the fences. When promised quick profits, respond with a quick ‘no’.”

- “If you instead focus on the prospective price change…you are speculating…Half of all coin-flippers will win their first toss; none of those winners has an expectation of profit if he continues to play the game.”

If your financial situation is similar to the data presented above, it may be time to reassess your investment objectives with us.

Here are some things to think about:

- Your household net worth has improved since the Great Recession and you want to add more risk to your holdings. However, you are now 6 years older and may need to draw down your assets in the next few years. How much risk can you reasonably add?

- Your household net worth is unchanged and you are now 6 years closer to retirement. What's the right level of risk that you can tolerate and to meet your retirement goals?

- You have generated more liquidity and don't need to access your invested assets for a longer time period. What's the right level of risk?

If you realize that there is no free lunch in investing and that you take various risks to achieve your returns then you will be fine.

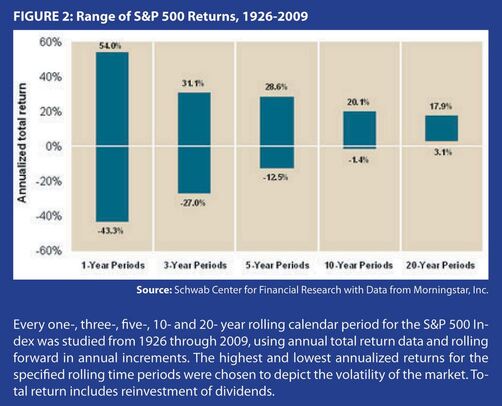

Further, time is really the only way to shape most risks. Short-term results from a diversified portfolio can vary widely, both in terms of return and volatility. Over longer time periods, we arrive at a narrower range of returns. The table below shows performance statistics for the S&P 500 for different rolling return periods.[vi]

Simply put, if indeed your household net worth has improved dramatically then it's worth a reexamination of your investment policies and goals. It might not mean adding more risk. Time matters most when adding risk and that should be factored into our discussion.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Jeff Paul, Senior Investment Analyst – Phillips & Company

[i] Federal Reserve Economic Data. (Mar 10, 2014). Households and Nonprofit Organizations, Net Worth, Level.

[ii] Sanchez, Juan M. (Feb 24, 2014). The Deleveraging of U.S. Households Since the Financial Crisis. Economic Synopses. Federal Reserve Bank of St. Louis. p.1.

[iii] Ibid.

[iv] Ibid., p.2.

[v] 2013 Shareholder Letter. Berkshire Hathaway. http://www.berkshirehathaway.com/letters/2013ltr.pdf. p.18.

[vi] Sensenig Capital Advisors, Inc. (Sep 16, 2011). Fundamentals in Uncertain Times. Data from Schwab Center for Financial Research / Morningstar.