On the Rise

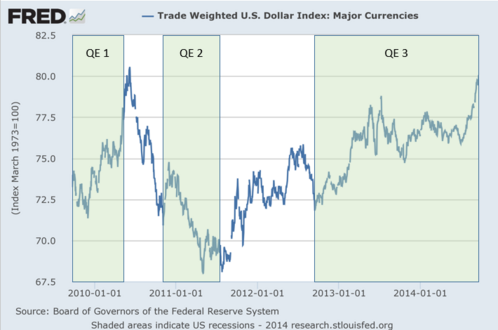

The US Dollar has been on a breathtaking rally we have not seen since 2010. The last time the US Dollar reached this level of value relative to other major currencies, our economy was finally emerging from the worst recession since the Great Depression and The Fed's Quantitative Easing policies were just taking hold.[i, ii]

It is clear that several factors are driving global investors back into US dollars as opposed to other currencies:

- The US economy is apparently leading the world back to normalized monetary policy

- The Global uncertainty of Russia and ISIS

- Europe's continued battle with deflation

- China's uncertain path of contraction or expansion

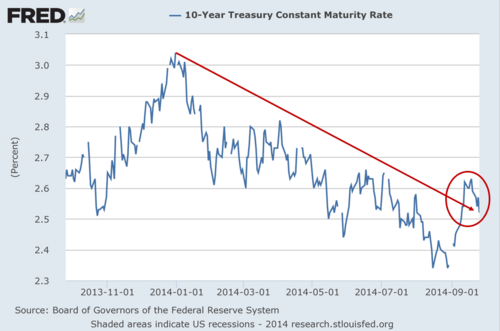

Validating this flow of funds is our 10-Year Treasury Bonds. In spite of the consensus view on the direction of interest rates and the clear direction provided by the Fed, actual rates are not rising. They are actually falling since January.[iii]

While a rising dollar is good news as an indicator of strength in the US economy, it also poses a set of challenges.

Mostly, US manufactured goods sold overseas become much more expensive. This hurts those companies’ earnings from operations after currency conversion (not that many companies are bringing those dollars back on-shore to pay high US taxes). Conversely, foreign manufactured goods and component parts become much cheaper to the US consumer, helping their earnings.

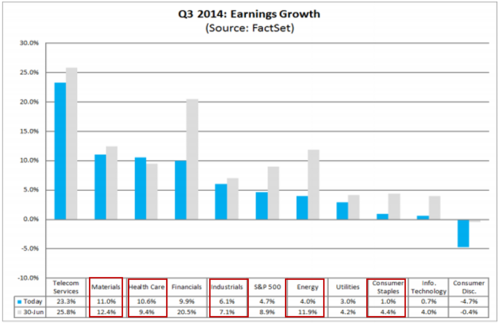

Energy, materials, industrials, medical equipment, pharmaceuticals, and consumer staples companies are all facing the challenge of a rising dollar. You can see from the chart below the earnings growth expectations for these sectors during Q3.[iv] Perhaps there might be an earnings miss. What's troubling is these industries make up 47% of the S&P 500.[v]

What could cause a reversal in the dollar’s rise is certainly open to speculation, but here are some potential events that have driven the dollar down in the past:

- The Fed changing its outlook on interest rate hikes.

- Foreign countries raising interest rates, leading to reduced foreign demand for US Treasuries.

- A growing US trade deficit.

- Fear, which causes investors to sell dollar-denominated assets and purchase more tangible assets, such as precious metals.

Our tilts toward emerging and developed markets might help mitigate against some of these potential headwinds if we see a continued rise in the dollar.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Jeff Paul, Senior Investment Analyst – Phillips & Company

References

[i] Federal Reserve Economic Data.

[ii] Murray, K. (Jun 9, 2013). Quantitative Easing and the Early Rally of 2013. The Queen’s Business Review.

[iii] Federal Reserve Economic Data.

[iv] Butters, J. (Sep 26, 2014). Earnings Insight. FactSet. p 14.

[v] S&P Dow Jones Indices (Aug 29, 2014). S&P 500 Sector Breakdown.