Phew!!!

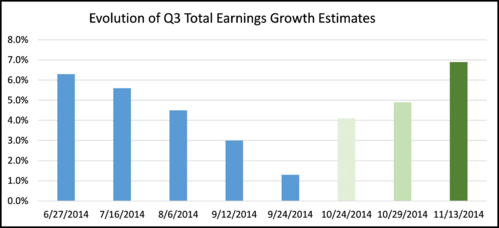

The Q3 earnings season ended with a report from Walmart last week. When we kicked this season off, expectations were very low but gradually improved.

S&P 500 companies were expected to grow earnings by 1.3% at the launch of the season and they produced a whopping 6.9% growth.[i,ii]

Amazing!

Unfortunately, investing requires you to live in the future. While we can allocate out some of the risk of uncertainty, in my estimation, you still need an opinion when allocating assets. So any deep breath that we can take is short lived.

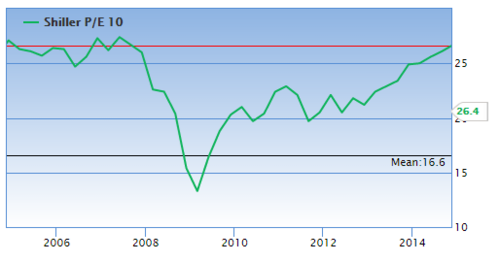

One of the biggest fundamental challenges is the higher than normal valuations on my favorite valuation metric, the cyclically adjusted price-to-earnings ratio or CAPE. We've opined on this on several occasions.

With an exceptional earnings season behind us, we can see the CAPE hardly moved.[iii]

With a current CAPE of 26.4, S&P companies are certainly valued at the higher end of the range.

So what would it take to see a normalization in the CAPE? Two things make up the CAPE: stock prices and earnings.

In order for the CAPE to revert to its mean of 16.6, stock prices could drop 37.1% in the next 3 years or an average annualized return of -14.3% on the S&P 500.[iv]

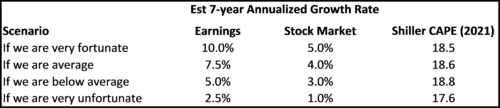

Another possibility is for earnings growth of 9% over the next 7 years, assuming 2% inflation and stocks increasing an average of 3%. The table below provides some other scenarios that could potentially get the CAPE closer to its long-term mean.[v]

A key takeaway is that if the Shiller CAPE reverts toward its mean, stock returns will be muted unless earnings stay very strong.

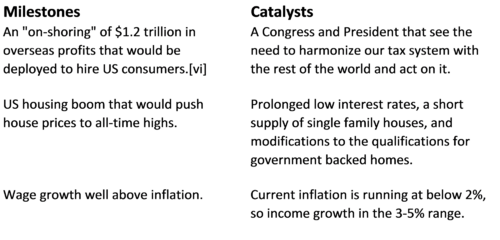

So in our real world case with the US economy improving, something would have to materialize for us to be in the very fortunate scenario. What would create an environment to propel S&P 500 companies to post astounding EPS growth in the 10%+ range?

Here are a few milestones in my opinion and the catalyst to see that happen:

Here's the good news - all of these catalysts have the possibility of materializing.

Congress is willing to act and so is the President. Presumptive Senate Majority Leader Mitch McConnell said the Senate “needs to be fixed” and that he and his Republican colleagues are willing to work with President Obama on some issues.[vii] White House press secretary Josh Earnest said,

“If there are things that the president can do differently to make sure that we're getting results for middle class families, for the American people, then he's willing to change his tactics to do exactly that.”[viii]

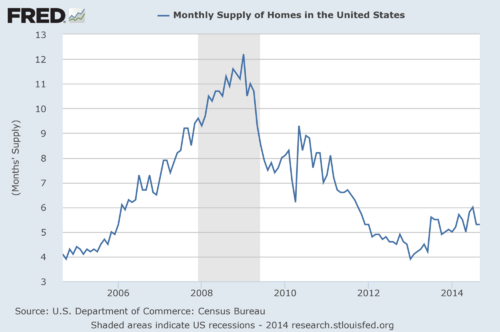

US housing is in very short supply.[ix]

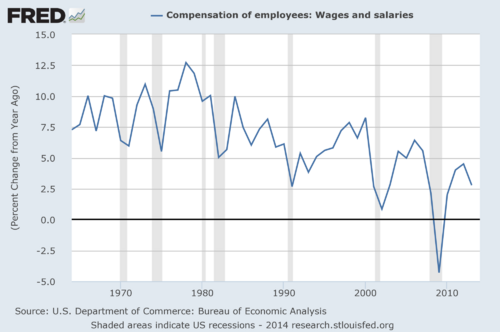

Since 1964, annual wage growth has exceeded 2% every year, except the recent recessions in 2001-2002 and 2008-2010.[x]

While it's no time (nor is it ever a time) to take a deep breath when you are invested in the equity markets, there are certainly some real catalysts that can push us to see a normalization in valuations and provide for reasonable returns for equity investors.

PHEW!!!

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Jeff Paul, Senior Investment Analyst – Phillips & Company

References

[i] Paul, J. (Nov 3, 2014). New Driver Needed for Economic Growth. Phillips & Company blog.

[ii] Mian, S. (Nov 13, 2014). Q3 Earnings Season in Final Stretch. Zacks Research.

[iii] GuruFocus.com. (Nov 17, 2014). Shiller P/E.

[iv] Ibid.

[v] Calculations estimated using data from www.econ.yale.edu/~shiller/data/ie_data.xls and assume 2% annual inflation.

[vi] Ehley, B. (Jun 3, 2014). Without Offshore Tax Havens, These Companies Would Owe the U.S. This Much. The Fiscal Times.

[vii] Chappell, B. (Nov 5, 2014). McConnell Says ‘Senate Needs To Be Fixed,’ Discussing GOP Gains. NPR.

[viii] FoxNews. (Nov 6. 2014). White House: Obama ‘willing to change his tactics’ to work with Republicans.

[ix] Federal Reserve Economic Data.

[x] Ibid.