Policy Driven Boom!

Credit in America is booming. There is simply no other way to say this. Let’s take a look at the recent data.

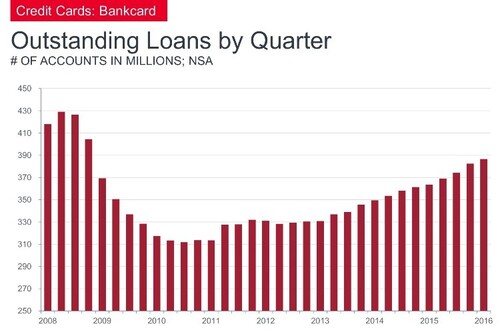

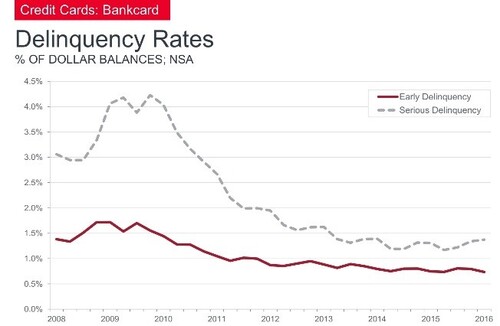

Credit card debt is expected to top $1 trillion by the end of 2016, which comes close to the peak that was set prior to the 2008 Financial Crisis. [i] [ii]

While outstanding loans are trending up, delinquencies have been fairly stable with only a small uptick in serious delinquencies. [iii]

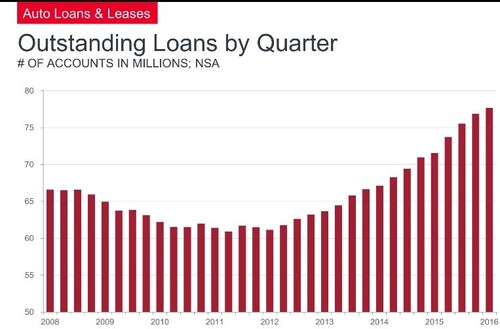

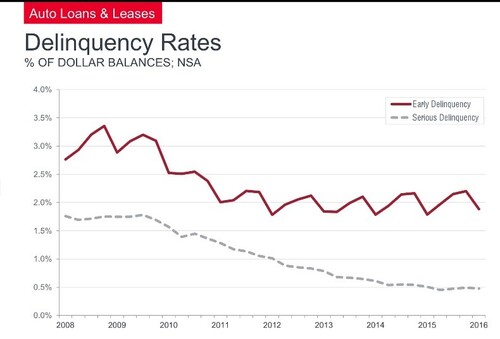

When we take a look at Auto loans, we reveal similar trends. [iv]

Outstanding loans are trending up while delinquency rates are below trend. [v]

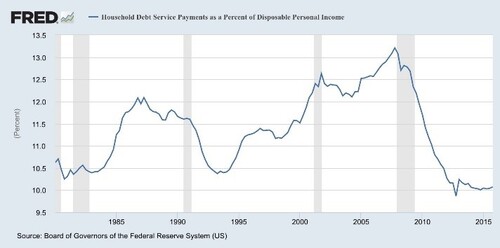

Combine this with the fact that the amount households pay to service all of this debt is still at very low levels, relative to where we were prior to the financial crisis. [vi]

All of this is very strong data for the U.S. Consumer and should bode well for Consumer Discretionary stocks, especially corporations focused more on domestic sales vs. U.S. domiciled companies who export throughout the world.

It's hardly a surprise that the Federal Reserve has signaled their willingness to consider rate increases in June or July versus later in the year. The world is certainly Central Bank driven.

When our markets stumbled at the beginning of the year, it took Fed dovishness on interest rates to reverse the trend. [vii]

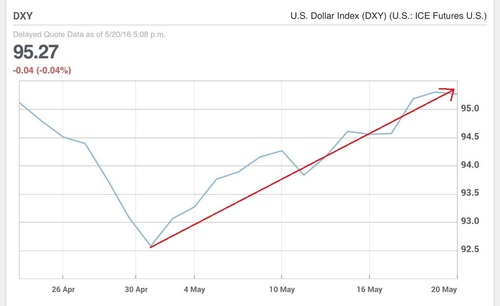

Over the last month, the Fed has been talking up the need to raise rates and you have seen our markets shutter… [viii]

… while the dollar has gotten stronger. [ix]

With rate increases comes the following potential consequences to individual investors:

- It will cost more to borrow money

- Expected return on investments will be lower

- Payback periods will be longer

- Cash will earn higher returns

- Bank’s will earn more margin interest from lending at higher rates

International Markets:

- Money will flow from emerging markets to the U.S.

- Investors will seek higher interest rates and lower risk for their debt purchases

- Emerging economies are driven by selling debt to international purchasers

- This is likely to have a negative impact on their markets

Exports from the U.S.:

- Become more expensive

- With rate increases the dollar becomes stronger

- This trend will continue to hurt large U.S. exporters’ earnings, putting a drag on Large Cap equities

Importers to the U.S.:

- Benefit from a continued strong dollar

- Help’s Europe, Japan, and select Asian emerging economies

- Especially automakers in Germany and Japan

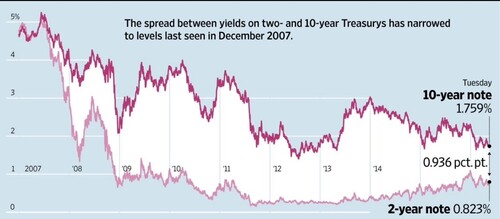

The yield curve can get a little flatter as we have discussed in prior posts and this could be a precursor to a recession. This chart from the WSJ. [x]

The winners and losers are never perfectly clear in a policy driven world. However, if the U.S. Consumer is any indication of overall trends, our allocations to Consumer Discretionary and U.S. Large Cap Growth could benefit our investors.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Chris Porter, Senior Investment Analyst – Phillips & Company

References:

[i] http://www.wsj.com/articles/balance-due-credit-card-debt-nears-1-trillion-as-banks-push-plastic-1463736600?tesla=y

[ii] http://www.equifax.com/home/en_us

[iii] http://www.equifax.com/home/en_us

[iv] http://www.equifax.com/home/en_us

[v] http://www.equifax.com/home/en_us

[vi] https://research.stlouisfed.org/fred2/graph/

[vii] https://www.google.com/finance

[viii] www.morningstar.com

[ix] http://www.marketwatch.com/story/dollar-slips-as-market-looks-ahead-to-next-weeks-g-7-2016-05-13

[x] www.wsj.com