Policy or Political Errors Abound

If the market playbook had followed its recent script, we should have had an extremely positive week last week. Over the past several months, heated China trade-war rhetoric and hawkish Federal Reserve interest-rate remarks have taken center stage, and markets have responded accordingly with increased volatility. [i]

Last week, those two catalysts had what would appear to be a reprieve. President Trump and China’s President Xi Jinping both confirmed a desire to resolve trade tensions within 90 days following their meeting on December 1, 2018, at the 2018 G20 Buenos Aires summit. [ii] Furthermore, China agreed to purchase over $1 trillion in U.S. goods in the coming years. [iii] [iv]

On top of the progress with China, the Federal Reserve took a dovish tone last week when discussing the future of interest rates. On Friday, St. Louis Federal Reserve Bank President James Bullard indicated his opinion that the Fed should pause its current cycle of interest rate increases. Here’s what he said:

“Financial markets do not expect the Fed to attain its stated inflation target… The current level of the policy rate is about right.” – St. Louis Federal Reserve Bank President James Bullard [v]

What should have been a positive week for U.S. equity markets, given the change in tone for trade talks and interest-rate comments, turned decidedly bad, leading to another market sell-off. [i]

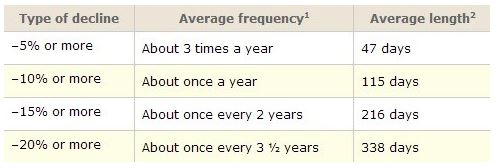

Given last week’s 5.63 percent decline in stocks (S&P 500 – SPY), U.S. equity markets re-entered the 10 percent correction for the third time this year. [i]

Under a typical year, we would have one 10 percent correction, as you can see from the table below. [vi]

However, we may just be catching up to the averages because, before last February, we hadn’t seen a 10 percent or greater correction in 689 days. [i]

So, what happened last week?

In my opinion, market participants started looking forward to 2019 and saw a few things we’ve discussed in the past:

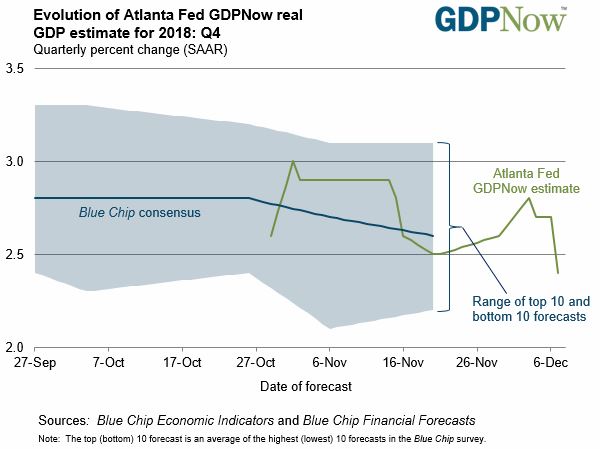

- GDP growth is expected to moderate. Expectations are for a downshift from 3 percent to around 2.5 percent growth. [vii]

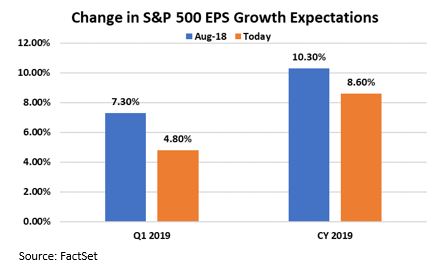

- Earnings-per-share (EPS) growth is downshifting. As we have discussed for several months now, EPS growth is also downshifting significantly. [viii] [ix]

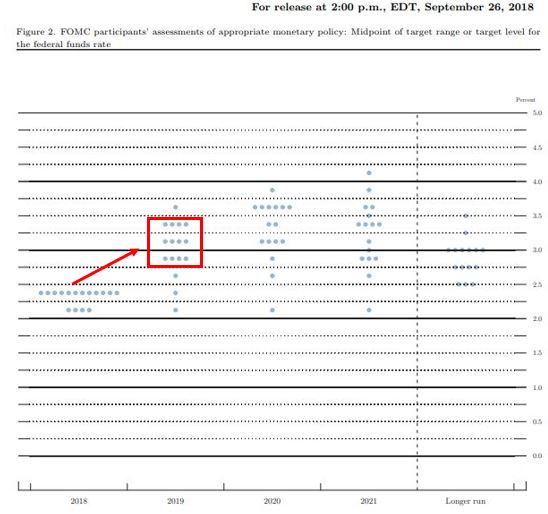

- The Federal Reserve’s interest-rate policy is changing. The Fed consensus still suggests three rate hikes next year, which might seem out of step for a slowing macroeconomic picture. [x]

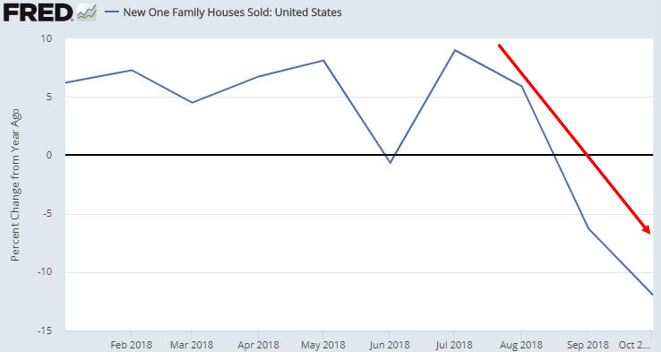

- Housing growth is slowing. New homes sales are beginning to slow. [xi]

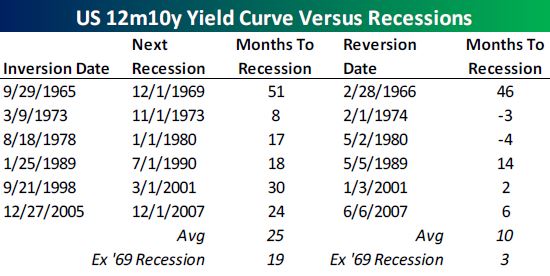

- The yield curve has inverted. The yield curve has seen a two-year and five-year inversion, which created some concerns over a looming recession. However, what investors need to consider is that usually, recessions lag the inverted yield curve by an average of 25 months. [xii]

While slowing growth is of concern for investors, there is little on the near-term horizon to suggest we are heading for a recession. Our call is near flat-line growth in Q3 2019 with accompanying monetary policy following shortly thereafter.

The biggest challenge might just be a major policy or political error that could cause something dramatic to happen. That to me is the biggest risk of all.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. Bloomberg, L.P.

ii. https://www.barrons.com/articles/stock-market-up-on-g20-trade-deal-1543800197

iii. https://www.straitstimes.com/world/china-made-more-than-us12-trillion-trade-commitments-mnuchin

iv. https://ustr.gov/countries-regions/china-mongolia-taiwan/peoples-republic-china

v. https://www.reuters.com/article/us-usa-fed-bullard/st-louis-feds-bullard-fed-should-halt-further-rate-hikes-idUSKBN1O626I

vi. https://PHILLIPSANDCO.COM/blog/breathtaking/

vii. https://www.frbatlanta.org/cqer/research/gdpnow.aspx

viii. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_081018.pdf

ix. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_120718.pdf

x. https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20180926.pdf

xi. https://fred.stlouisfed.org/series/HSN1F#0

xii. https://PHILLIPSANDCO.COM/files/4615/4447/2500/The_Bespoke_Report_2019_--_Yield_Curve_and_the_Fed.pdf