Rising Mortgage Rates: No Big Deal for Now?

It’s no secret that interest rates have been on the rise, but it appears they are rising at a faster pace as of late. Specifically, home mortgage rates, which impact so many Americans, are at levels they haven’t been in some time. In fact, 63 percent of Americans own their own home, and of those homeowners, 65 percent carry a home mortgage. [i]

We must go back to mid-2011 to find a thirty-year mortgage rate that exceeds the current (as of May 17, 2018) 4.61 percent rate. [ii]

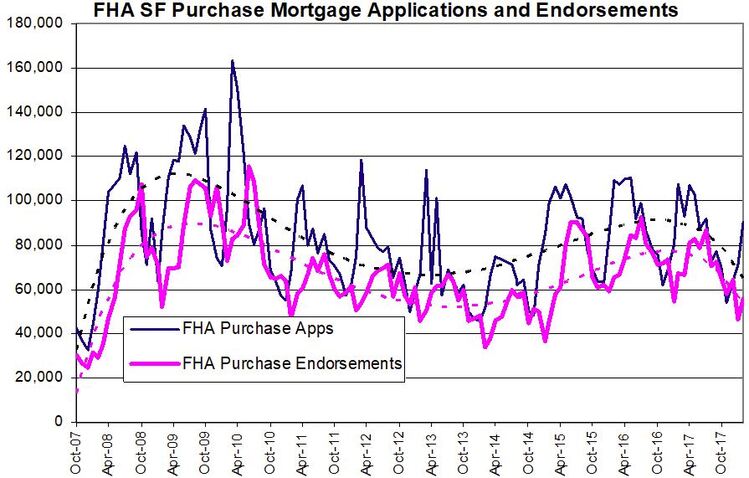

As you may suspect with such elevated mortgage rates, mortgage applications and endorsements for FHA loans are posting year-over-year declines of 12.2 percent and 14.8 percent, respectively. Numbers like those should give everyone pause. [iii]

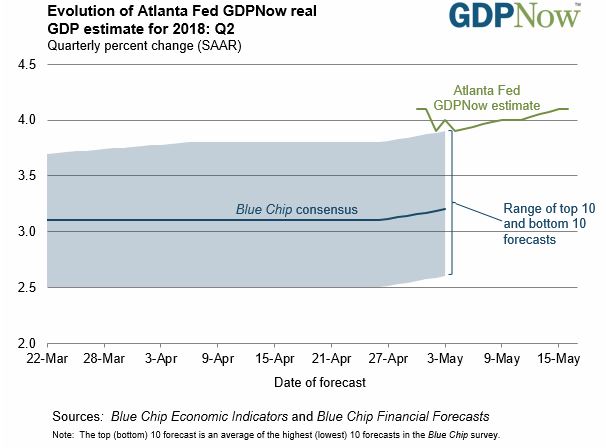

Furthermore, it should give us pause when we consider the likelihood of the U.S. economy growing at over 4 percent, which is what the Federal Reserve Bank of Atlanta is forecasting for second quarter GDP. [iv]

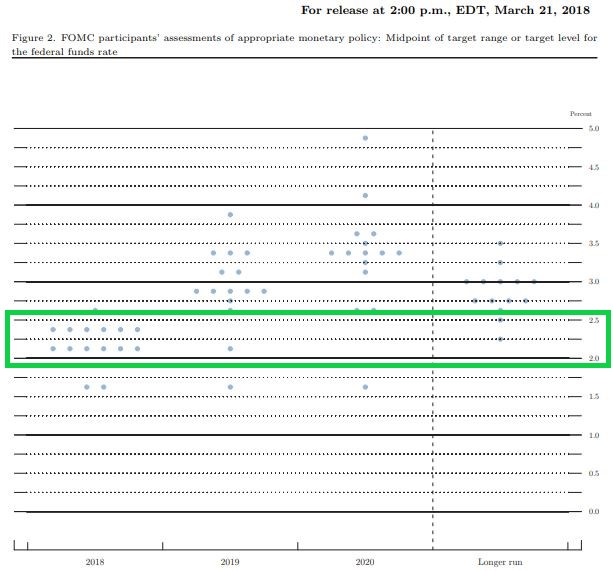

With forecasts like those, we could see the Federal Reserve raise rates an additional three times this year. [v]

In general, rising mortgage rates can erode the purchasing power of many Americans. With rising interest rates, the cost of home ownership is bound to rise, which would likely decrease available money to purchase other homes or other goods and services. It’s important to note that interest payments, despite the flow through large financial institutions, are not an overall addition to our economy.

Often, homeowners can become “rate locked” into their existing homes due to an unwillingness to buy a new home at a higher interest rate and, thus, take on a higher cost of ownership. Perhaps higher mortgage rates are why we’ve seen the average length of home ownership increase over the last few years. The median number of years homeowners stay in their homes before selling has increased from a pre-financial crisis level of 6-years to almost 10-years now. [vi]

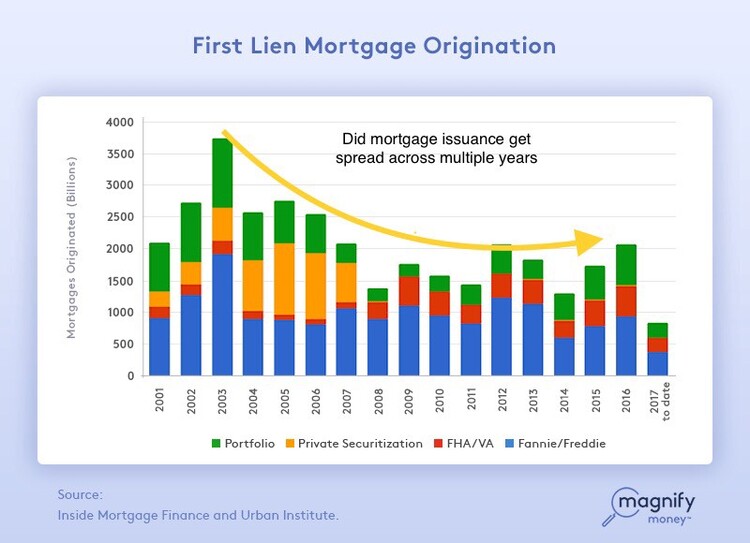

A little basic math indicates that the next large mortgage wave may have already occurred since origination's peaked back in 2003. [vii]

Perhaps a slowdown in mortgages and an increase in the length of home ownership are reflections of borrowers holding onto their homes at lower interest rates, and thus preserving their purchasing power. If my assumption is correct, that approach should continue to leave plenty of purchasing power in reserve to withstand additional increases in mortgage rates.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://www.magnifymoney.com/blog/mortgage/u-s-mortgage-market-statistics-2017/

ii. https://fred.stlouisfed.org/series/MORTGAGE30US

iii. http://www.calculatedriskblog.com/

iv. https://www.frbatlanta.org/cqer/research/gdpnow.aspx

v. https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20180321.pdf

vi. https://www.wsj.com/articles/stuck-in-place-u-s-homeowners-hunker-down-as-housing-supply-stays-tight-1509274802

vii. https://www.magnifymoney.com/blog/mortgage/u-s-mortgage-market-statistics-2017/