Risk Is Not Relative

This week marked another week in which the major market indexes hit all-time highs. It’s clear that investors are feeling very good and continue to pour more money into equities. Since the start of October, investors have added $34.2 billion into equity funds, and have withdrawn $26.9 billion from bond funds, according to Investment Company Institute data. [i]

The one surprise for me which I would have never predicted is the amount of aggressive behavior that I am witnessing. For example, an article in Forbes in September said that at Tesla’s current price, the company would have to be selling cars at a price of $1.1 million each, whereas the actual price of a Tesla Model S is between $80-110,000. [ii]

I'm shocked at how quick greed has come back to the US investor. I thought it would be a generation before we saw speculative behavior return.

Intrinsic Value

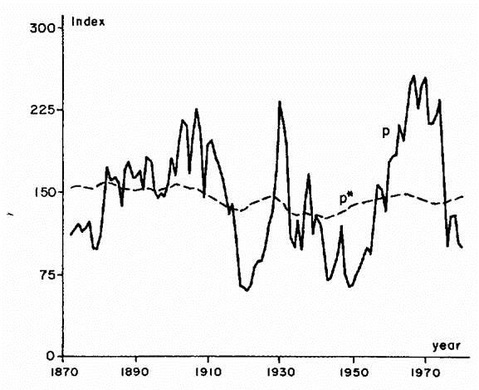

Just by first principles, finding out how much a company should be worth is easy. In fact, the recent Nobel Prize winning economist, Robert Shiller pondered a simple question. If companies can be valued based upon their cash flows (dividend growth), stock prices should be fairly stable. In the chart below, the dotted line represents the present value of the dividends of a stock—fairly consistent. [iii]

The problem comes in to play with the solid line, which represents the actual price of the stock. Shiller suggested something else was going on with prices—namely, investor behavior. He went on to spend his career understanding that exact behavior.

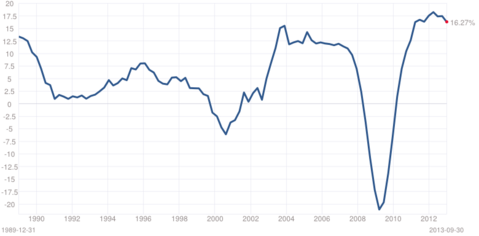

Let's walk his Nobel Prize-winning question forward through today. We have seen dividend growth rates start to peak out. Below is the dividend growth rate chart on S&P 500 stocks: [iv]

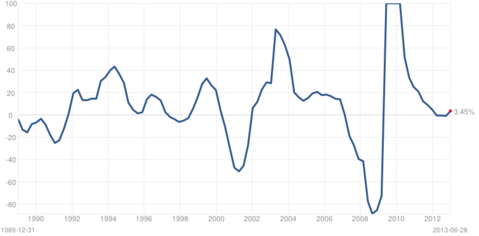

Also, earnings growth rates have been declining and are presently close to flat. Below is a chart on earnings growth rates on S&P 500 stocks: [v]

Shiller’s study was written in 1981. Nowadays, more companies sometimes choose to reinvest earnings into their own business activities, so earnings growth rates are one of the major drivers for the true intrinsic value of a stock—as we have written before.

Yet, we are seeing multiples expand and prices rise in spite of a drop in earnings growth rates. Below is a graph of the S&P 500 PE ratio since the start of the year. Just look at how it keeps pushing higher: [vi]

So, how is it that stock prices are going up when drivers of intrinsic value are not?

Answer: Investor’s behavior toward risk is changing. In the past 5 years, investors have gone from evaluating risk on an absolute basis to a relative basis. Before, investors were asking how long will my assets last and how will the markets impact me if I see a drop a few years before retirement?

Now they are asking, how I can get 24% returns like the S&P 500 is posting this year?

Risk isn’t relative

It's a little like driving your car on a highway going 90 mph when everyone else is going 90 mph. It may feel like you are going with the flow...until you hit something. Whenever price diverges from intrinsic value (which is what we are seeing right now), risk in the market goes up.

Risk perception is not a relative exercise. Risk is an absolute based upon your individual circumstances.

So how long can investors drive valuations higher before they hit something? Let's take a look. Below is a chart on the PE ratio of the S&P 500 over the last 30 years:

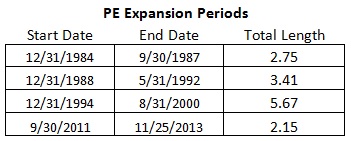

PE ratios expand over several years and then consolidate. Right now, we are just over two years into a multiple expansion cycle. As you can see below, those cycles can run for a long time.

The undisputed truth in any investment is you are going to pay for whatever returns you generate in the form of risk. There is no way around that simple truth. You simply need to decide how much risk is really appropriate for your long-term financial plan. Remember, your landlord doesn't care how many shares of Tesla you own.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Alex Cook, Investment Analyst – Phillips & Company

[i] “Summary: Estimated Long-Term Mutual Fund Flows Data”, Investment Company Institute

[ii] “Tesla is Overvalued: Let me count the ways”, Forbes

[iii] “Do stock prices move too much to be justified by subsequent changes in dividends?”, Robert Shiller

[iv] “S&P 500 Dividend Growth”, multipl.com

[v] “S&P 500 Earnings Growth Rate”, multipl.com

[vi] Bloomberg LP

[vii] Bloomberg LP