The Cost of Closure

With a temporary reprieve from the longest shutdown in our government’s history, from an investor’s perspective, it makes sense to examine the costs of the shutdown and what those costs mean for investors going forward. [ix]

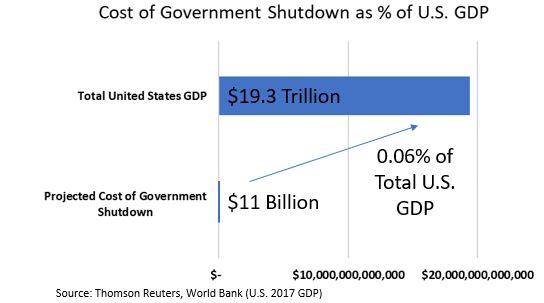

According to Thomson Reuters, the closure will cost the U.S. economy $11 billion. However, in the grand scheme of things, that’s practically a rounding error for the United States’ nearly $20 trillion economy. [ii] [iii]

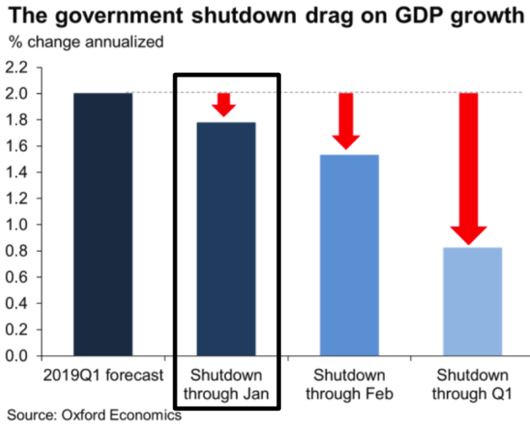

Other estimates would suggest the shutdown could cost the United States 0.20 percent of GDP growth. [i]

The threat of another government shutdown doesn’t necessarily mean negative equity returns. In fact, during the recent shutdown, the S&P 500 rallied more than 13 percent. [iv]

This growth is slightly uncharacteristic to what history has shown. On average, shutdowns have produced slightly negative returns since 1976. [v]

However, as I’ve echoed many times, it would be foolish to try and predict the outcomes of the stock market due to a government shutdown. And yet, that’s exactly what many have tried to do. Look no further than the outspoken J.P. Morgan Chase CEO, Jamie Dimon. Here’s what he said:

“Someone estimated that if it [government shutdown] for the whole quarter, it can reduce growth to zero… We just have to deal with that. It’s more of a political issue than anything else.” – Jamie Dimon, J.P. Morgan Chase CEO [vi]

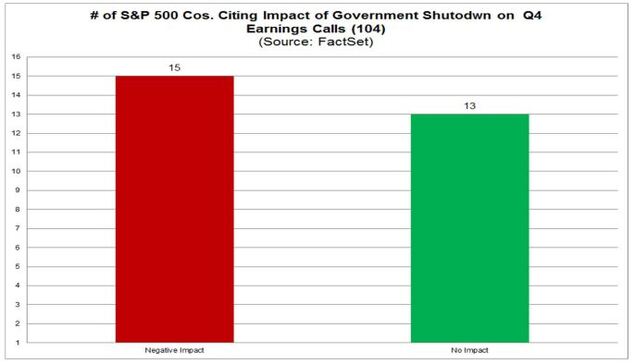

Furthermore, according to FactSet, 33 percent of companies that have reported earnings have mentioned the government shutdown in their reports; however, only 15 companies cited that the shutdown affected them negatively. [vii]

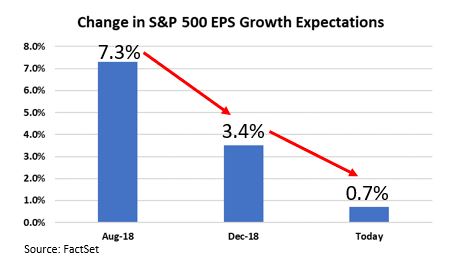

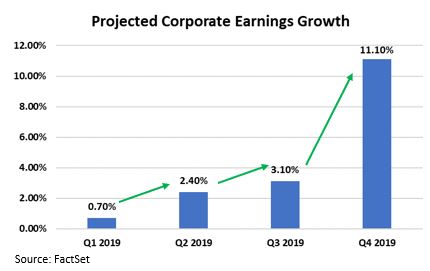

It’s clear that the shutdown is having little, if any, impact on corporate earnings. The bigger concern for market participants is the ongoing weakening of earnings growth. If the recent trend of downward earnings growth revisions for Q1 2019 continues, we might see negative earnings growth once all the numbers are reported in May. [vii] [viii]

With that said, my expectations in the coming quarters will be an increase in volatility, similar to what we have seen in the recent past. [iv]

I also expect a range-bound market for the coming months until investors begin factoring in their anticipations for better earnings growth in the second half of 2019. [vii]

The cost of the shutdown has been a nice distraction from a normal top-of-cycle earnings event. However, there are more challenges ahead beyond another government shutdown and the costs associated with that.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://blogs.wsj.com/dailyshot/2019/01/28/the-daily-shot-is-the-unemployment-rate-close-to-bottoming/ (subscription only)

ii. https://www.reuters.com/article/us-usa-shutdown-economy/partial-u-s-government-shutdown-cost-economy-3-billion-budget-office-idUSKCN1PM1SL

iii. https://data.worldbank.org/indicator/NY.GDP.MKTP.CD

iv. Bloomberg, L.P.

v. https://www.marketwatch.com/story/should-wall-street-fear-a-government-shutdown-heres-how-stocks-fared-during-past-closures-2017-04-21

vi. https://www.cnbc.com/2019/01/15/jamie-dimon-says-shutdown-could-reduce-economic-growth-to-zero-this-quarter-if-it-continues.html

vii. https://bit.ly/2CSMurx

viii. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_081018.pdf

ix. https://www.cnn.com/2019/01/03/politics/government-shutdown-length-trnd/index.html