The Handoff

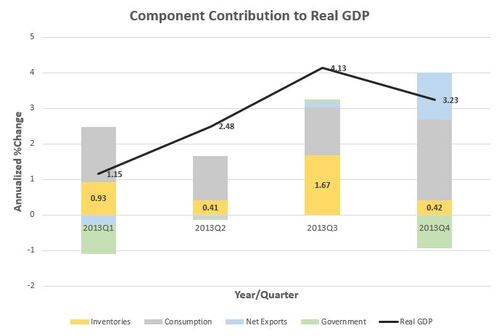

As we have opined in the past several months, much of the US GDP growth has come from businesses pushing "all in" on the US consumer and building up inventories to meet expected demand.

(Source: Moody’s Analytics, GDP)

As the impact of inventory on GDP begins to diminish, will consumption take its place? It's a risky bet as we have seen an increase in tax rates, a reduction in unemployment benefits, and brutal weather, all of which impact consumption.

All of that headwind aside, there are some strong currents that can bode very well for the US consumer in the coming years. Perhaps inventory driven GDP can hand off to the next player in the relay....US banks. If we hold consumer savings and wages at current low levels, we can isolate and look at bank lending to allow credit expansion.

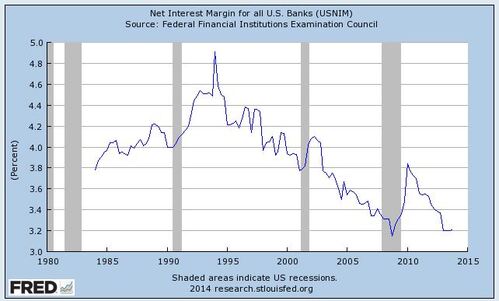

First, banks have every incentive to lend more. They are making some of the lowest margins on deposits since 2008, as shown in the graph below.[i]

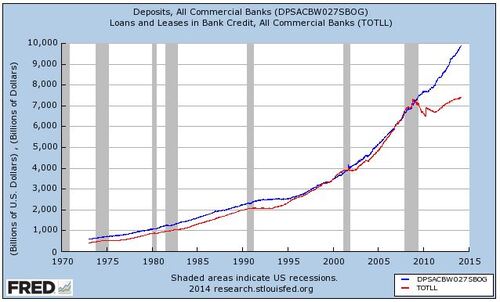

Second, banks are sitting on historically high amounts of cash (making near zero returns), as observed by the widening gap between the total deposits (blue) and total loans (red) lines on the graph.[ii]

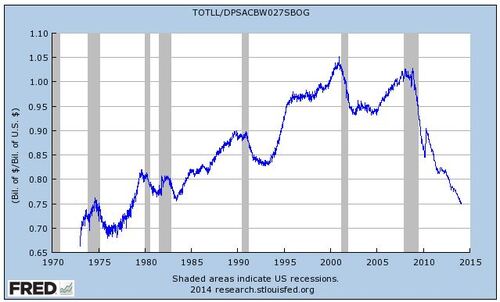

Third, banks are at historically low levels of loans to deposits not seen in over 35 years.[iii]

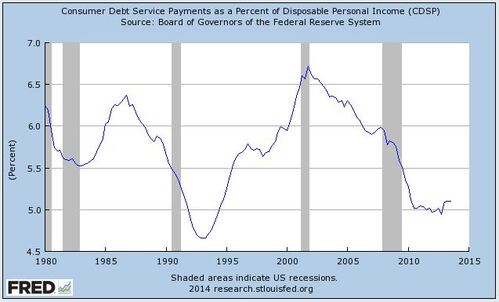

Finally, if willing, the consumer is in the best shape to lever up their personal balance sheets and consume more.[iv]

What if banks were to simply return to their average loan to deposit ratio of 0.87 from the current ratio of 0.75?[v] That would pump $1.4 trillion dollars back into the economy fueling 6.7% of GDP growth on top of what we are currently growing.[vi]

If US banks can take the handoff from US business, we could see another leg up for corporate profits driven by consumption. The key will be the willingness for the US consumer to lever up. Banks will also need to be willing to make credit more available. In 2014Q1, lending standards for prime residential mortgage borrowers tightened, and demand weakened for the second consecutive quarter. However, other types of consumer credit improved due to looser lending standards and increased demand.[vii]

Watch out - if "animal spirits" return, we could have another surprise to the upside.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Jeff Paul, Senior Investment Analyst – Phillips & Company

[i] Federal Reserve Economic Data. Feb 14, 2014.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Ibid. Average calculated from weekly ratios from Jan 1, 1973 to Feb 5, 2014.

[vi] GDP Report. Bureau of Economic Analysis, US Dept of Commerce. Jan 30, 2014.

[vii] Moody’s Analytics. Feb 3, 2014. US: Senior Loan Officer Opinion Survey.