The Onion Has More Than One Layer: Crying or smiling will depend on your sensitivity

The Onion Has More Than One Layer: Crying or smiling will depend on your sensitivity

Weekly Market Commentary 6-3-13

Tim Phillips, CEO—Phillips & Company

As discussed in last week’s blog, policy errors are all around us. The US equity markets have pulled back 1.44% since May 22, when the Federal Reserve Chairman suggested they might ease off on buying bonds in the open market if the economy improves.[i]

So why would equity prices drop if the economy improves? It would seem logical if the economy improves, companies and consumers are doing much better and that should drive stock values higher not lower.

While this is all true, what is also true is interest rates would have to rise to reflect the strength of our economy and act as a brake to inflation. Generally this is done through monetary policy set by the Federal Reserve Bank. As efficient as our capital markets are, participants (bond traders, mutual funds, pension plans, etc.) all anticipate changes well before the Fed can take action. In this case, rates rise before monetary policy can be enacted.

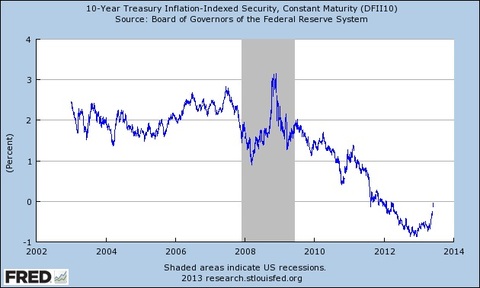

Take a look at the 10 year Treasury market that measures real interest rates (TIPS). It is important to note that what matters is real rates (those that adjust for inflation, as inflation erodes our buying power).

(Source: Federal Reserve)

You can see that quite a spike recently occurred.

So back to the question, why would equities drop when the economy improves and real interest rates rise?

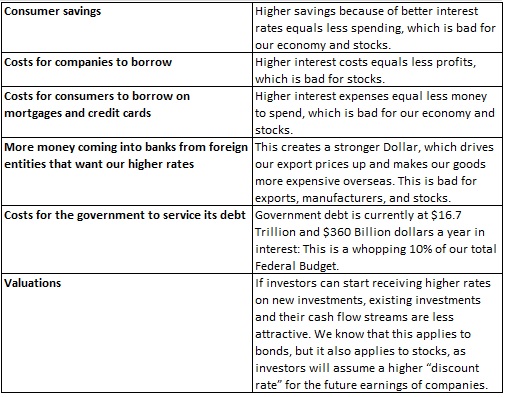

The simple answer is higher interest rates lead to the following, in theory:

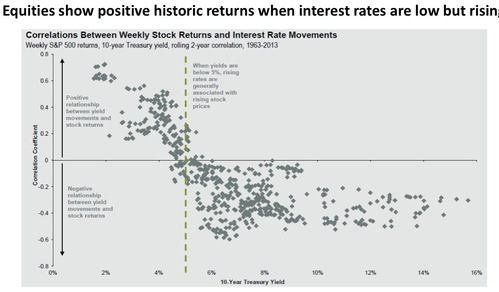

Note that I said all this could happen, in theory. In practicality, stocks tend to rise during rising rate environments up until a point:

(Source: JP Morgan 2Q 2013 Guide to the Markets)

As you can see from the chart, stocks have historically risen with rates up until around a 5% rate on the 10 year Treasury.

Why? This is the speculative part.

- Rising rates don't always impact consumers immediately at lower rate levels. Take housing for example; if your house price rises faster than inflation, you might feel good and spend more in spite of a rise in interest rates. By the way, housing prices have risen by 8.74% in the last two years.[iii]

- If you are collecting more interest income, you might spend more of it.

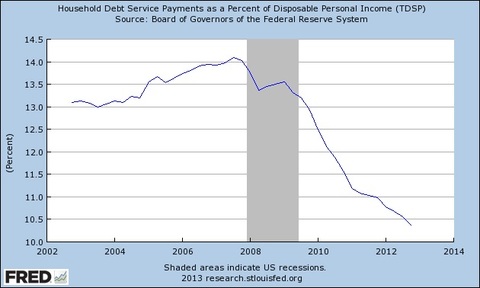

- If you are not paying that much in interest expense, a rise in interest rates might not impact you as much at lower rate levels. As you can see below, household debt service payments as a percent of disposable personal income are at multiyear lows:

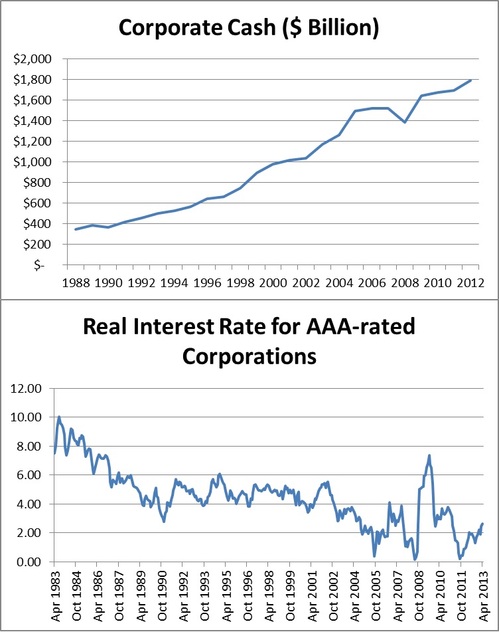

- If companies can buy things with cash vs. borrow, or borrow at very low long term rates, a rise in interest rates might not impact them at lower rate levels. You can see below that corporate cash levels are at generational highs, and real interest rates for corporations are at generational lows.

(Source: Federal Reserve. Real interest rates for AAA corporations based on AAA bond yields deflated against the year over year change in CPI).

- US Government borrowing needs are dropping with a rise in taxes and a cut in spending, which reduces our debt services going forward—almost not worth mentioning but theoretically true. According to a Wall Street Journal article on May 15, the Congressional Budget Office is expecting the deficit to shrink to $642 billion, which is substantially smaller than the $1.087 trillion deficit last year.

My guess is market participants are once again only looking at the outer peel of the onion and reacting (selling) when it comes to stocks. While this time could be different, we might just have some time to go before rising rates impact our consumer and economy.

Special note on bonds

None of this diminishes the notion that bond durations should be lowered in portfolios and that requires some active management on your part as well as ours.

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Alex Cook, Investment Analyst – Phillips & Company

[i] Bloomberg LP

[ii] National debt figure and interest expense figure from TreasuryDirect.gov “Debt to the Penny” and “Interest Expense on the Debt Outstanding.” Interest expense as a percent of the budget is calculated as the 2012 interest expense divided by total actual FY 2012 federal outlays from the CBO.gov publication “CBO—The Budget and Economic Outlook: Fiscal Years 2013 to 2023.”

[iii] “S&P/Case Shiller US National Index Levels Q1 2013 Not Seasonally Adjusted”, S&P Dow Jones Indices