The Public Utility Kicks In

With just a few weeks’ worth of S&P 500 earnings reports released for Q1 2019, the earnings recession we have been talking about for many weeks is beginning to take shape.

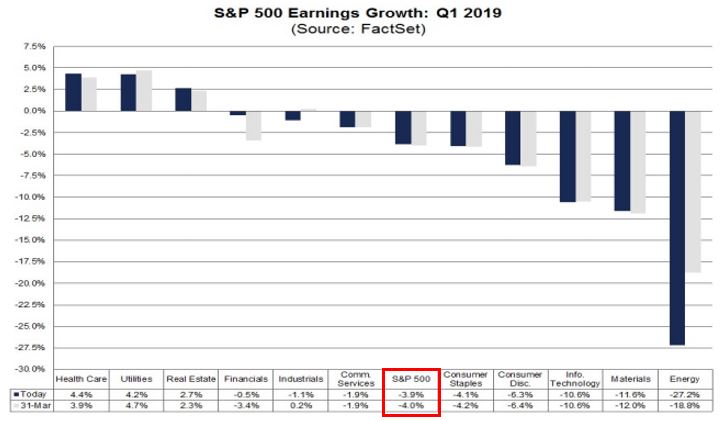

So far with 15 percent of companies reporting their Q1 2019 earnings, FactSet is anticipating a decline of -3.9 percent versus the prior year’s Q1 earnings. [i]

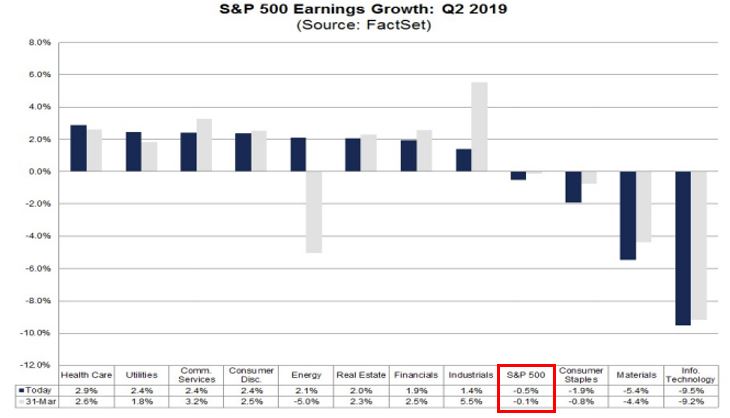

Furthermore, FactSet goes on to anticipate a decline in corporate earnings of -0.5 percent for Q2 2019. [i]

If these forecasts come to fruition, we will indeed be in an earnings recession.

Given the negative earnings growth for Q1 thus far, and the expected release of an extensive number of earnings reports expected out for S&P 500 companies, this week should shed a lot of light on the staying power of these forecasts. Simultaneously, we see a very busy week of activity for global central banks as well. The following banks are set to meet and discuss expectations on growth, inflation, and potential changes in their respective monetary policies: [ii]

- Bank of Canada – April 24, 2019

- Bank of Japan – April 25, 2019

- Riksbank (Bank of Sweden) – April 25, 2019

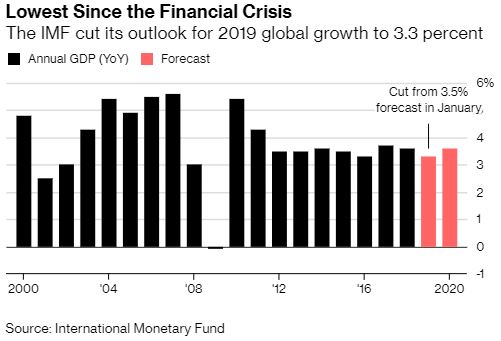

I suspect all of these central banks are likely to take their cues from the U.S. Federal Reserve and hold, or even ease, their monetary policy. This is especially true considering the IMF’s continued reports on moderating global GDP growth, primarily driven by Euro-area economies. [iii]

If these central banks do in fact take their cues from the U.S. Federal Reserve, it’s worth looking at how U.S. markets reacted to the Federal Reserve’s recent dovish stance to gain a better understanding about how those markets may react. [iv]

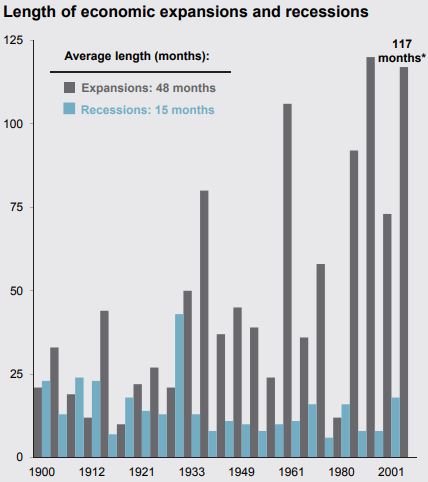

It’s these types of market reactions, based on central bank rhetoric, that further support central banks becoming the new public utility. It’s clear they provide the needed fuel to expand this extraordinarily long economic cycle. [v]

I’ve recently returned from ten days of doing business in China. It’s my belief that no country understands the public utility approach to monetary and fiscal policy better than China. The Communist Party has rolled out all the stops to protect its economic growth. Here’s the list of what China is doing to keep the engine firing on all cylinders: [vi] [vii] [viii]

- Tax cuts

- Infrastructure spending – Belt and Road Initiative

- Lowering interest rates

- Cutting the reserve requirements for large, medium, and small banks

- Shantytown project

- China’s “Cash for Clunkers” program

It’s clear to me that centralized command of economies is the new normal after the Great Recession. What’s not clear, and I’m quite uncertain about, are the consequences for the length, strength, and reliability of the new public utility, especially as we face several months of uncertain earnings reports.

My best advice is to prepare for some rocky roads ahead. Perhaps these rocky roads will lead to an opportunity to buy some assets at cheaper prices in the coming quarters.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Tim Phillips, CEO, Phillips & Company

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://www.factset.com/hubfs/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_041819.pdf

ii. https://www.dailyfx.com/central-bank-calendar

iii. https://www.bloomberg.com/news/articles/2019-04-09/imf-cuts-global-growth-outlook-to-lowest-since-financial-crisis

iv. https://finviz.com/quote.ashx?t=spy

v. https://am.jpmorgan.com/blob-gim/1383407651970/83456/MI-GTM_2Q19_%20LINKED.pdf?segment=AMERICAS_US_ADV&locale=en_US

vi. https://PHILLIPSANDCO.COM/files/5915/5442/5884/Look_Ahead_Q2_2019_Final.pdf

vii. https://www.wsj.com/articles/a-new-stimulus-cant-keep-chinese-auto-stocks-at-top-speed-11547030617 (subscription required)

viii. https://www.reuters.com/article/us-china-economy-property/china-spends-256-billion-on-shantytown-redevelopment-in-2018-idUSKCN1PG0NB