To Dividend or Not to Dividend

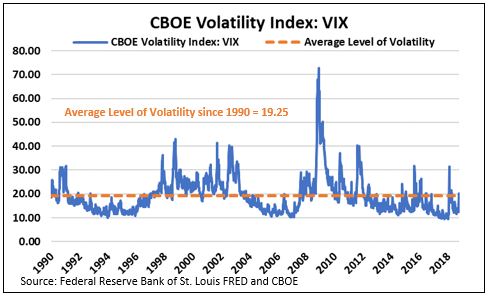

Despite the rise in market volatility and the recent pullback in stock prices, the market still lays claim to the longest bull market in history. However, as the market readjusts to a normalized level of volatility, many investors have begun to wonder if a longer-term correction is just around the corner. [i] [ii]

In light of this, I get a lot of questions about adding dividend stocks, ETFs, and other dividend-focused mutual funds as a way of becoming more defensive with the equity portion of investors' portfolios.

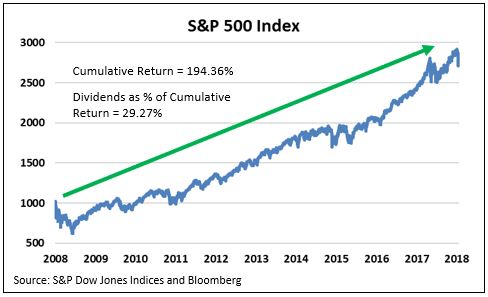

In reality, this is a fair question. Over the past ten years, the cumulative return of the S&P 500 has been 194.36 percent, of which dividends have contributed nearly 30 percent to that total return. [iii] [iv]

However, to breathe a word of caution your way, adding just any type of dividend-focused securities to a portfolio may, in fact, lead many cautious investors down a path of greater risk. In fact, many investors believe that by adding high-dividend-yielding securities to their portfolios, the higher level of income will insulate them from large drawdowns in the event of a market correction. Unfortunately, that couldn’t be further from the truth.

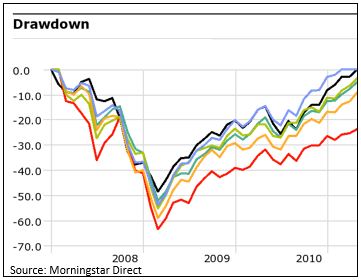

To illustrate my point, I plotted the max drawdowns during the financial crisis for several of the top-rated, high dividend-focused ETFs and compared them to the S&P 500 (the black line). It was no surprise that the higher-yielding funds had much larger max drawdowns in the wake of the financial crisis. [v]

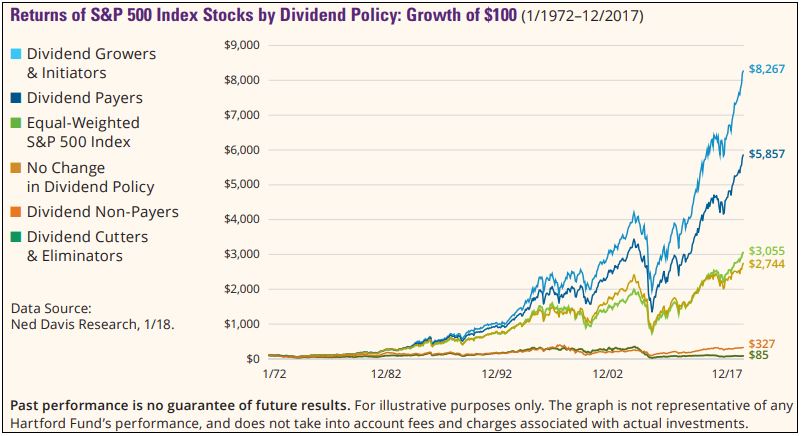

But that’s not the case for all dividend-focused securities. Although it’s clear that high-dividend yields may lead to larger inherent risks, securities that focus on dividend growth versus dividend yield may just be what we’re looking for.

Companies within the S&P 500 with a history of consistent dividend growth have outperformed their counterparts, both to the upside as well as offering more protection to the downside. In other words, this translates to higher risk-adjusted returns. [vi]

Well all of this makes sense when looking retrospectively.

The question we must ask now: Can the dividends keep growing?

The simple answer is yes, for three reasons:

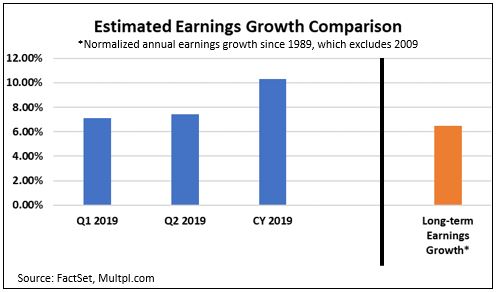

The first is earnings growth. As we’ve opined in many past commentaries, as well as in our most recent Q4 2018 Look Ahead, earnings growth is projected to remain strong through 2019 and well above its long-term growth rate. [vii]

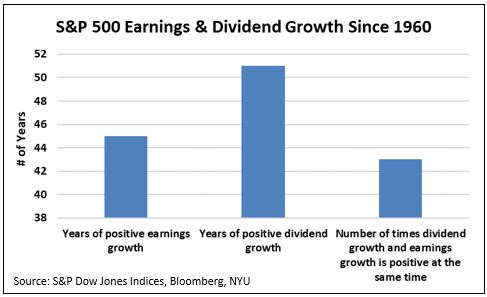

One thing to point out is that since 1960, the S&P 500 has seen positive earnings growth in 45 out of those 57 years, or almost 80 percent of the time. During those same 57 years, the S&P 500 has grown dividends in 51 of those years, or almost 90 percent of the time. Remarkably, 95 percent of the time that the S&P has experienced positive earnings growth, dividend growth has remained positive. [iii] [vi] [viii]

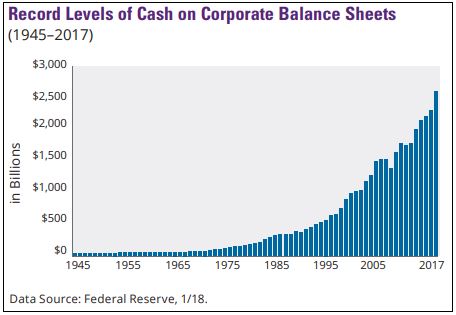

The second is corporate cash. Cash on the balance sheets of corporations has never been higher. In fact, over the past 15 years, cash on corporate balance sheets has more than doubled, which suggests there is a good probability that some of it will be used for increasing dividends. [vi]

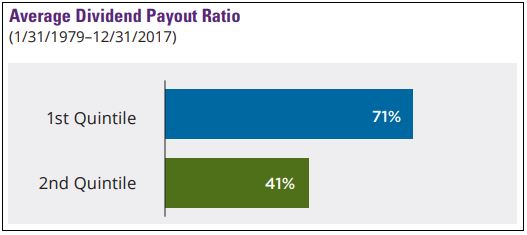

And third is the dividend payout ratios. Based on research by Wellington Management, the average dividend payout ratio between the first and second quintiles of dividend growth stocks in the S&P 500 is 30 percentage points. In fact, the second quintile stocks, with a lower dividend payout, outperformed the S&P 500 by 88.9 percent on a cumulative basis, dating all the way back to 1929. [vi]

Don’t just add dividend-paying securities to your portfolio to reduce risk; we’ve seen what that can do. If you decide to, speak to your advisor and carefully evaluate the companies and/or funds that you’re planning on adding. High levels of corporate cash, lower payouts ratios, and strong earnings growth are key to that evaluation and would suggest continued support for dividend growth, or at least support the case for not cutting dividends in the near future.

If you have questions or comments, please let us know. You can contact us via Twitter and Facebook, or you can e-mail Tim directly. For additional information, please visit our website.

Robert Dinelli, Investment Analyst, Phillips & Company

References:

i. https://www.schroders.com/en/insights/economics/the-longest-bull-market-in-history-in-five-charts/

ii. https://fred.stlouisfed.org/series/VIXCLS#0

iii. https://us.spindices.com/indices/equity/sp-500-top-50

iv. Bloomberg, L.P.

v. Morningstar Direct

vi. https://www.hartfordfunds.com/dam/en/docs/pub/whitepapers/WP106.pdf

vii. https://PHILLIPSANDCO.COM/files/6615/3876/8981/Look_Ahead_2018Q4_-_Final.pdf

viii. http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/spearn.htm