What Else Can You Buy?

One of the best parts of visiting with your friends and clients is the fairly large dose of reality that you receive. For professional investors, getting used to the up’s and down’s of the market builds a certain level of emotional immunity. Those that make their living in the real economy, such as many of our readers, have a growing concern over how inflated the markets have become.

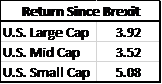

It's no surprise seeing as how the U.S. equity markets have been on a tear lately. From the Brexit vote alone, we have seen prices rise to all-time highs. [i]

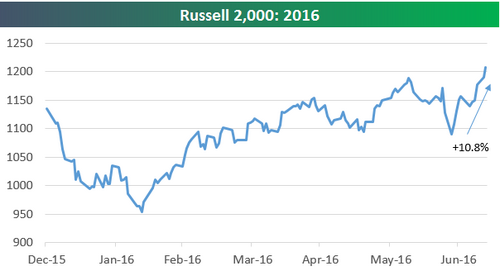

Over the last three weeks, the Russell 2000 is up over 10%. Which is causing some real concern to investors. [ii]

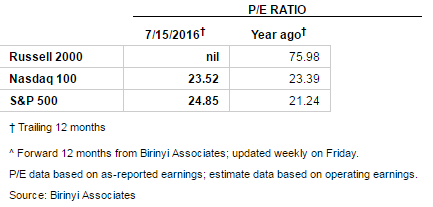

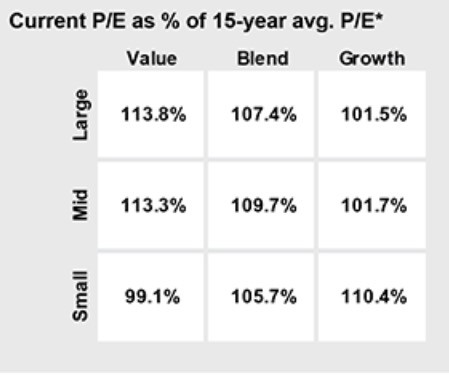

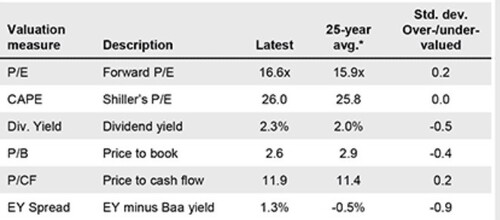

On a trailing earnings basis, there is no denying equity valuations in the U.S. are elevated. [iii] [iv]

However, when we buy stocks, we are purchasing future earnings and dividends. Therefore, reviewing trailing earnings may be a mental mistake. We are buying the future and in most cases, holding our position, all based upon future earnings. From that perspective, across most measures, valuations look closer to fair value. [v]

Let's not gloss over the simple fact that the difference between trailing earnings and forward earnings is the fact that future earnings, while expected to grow, are questionable.

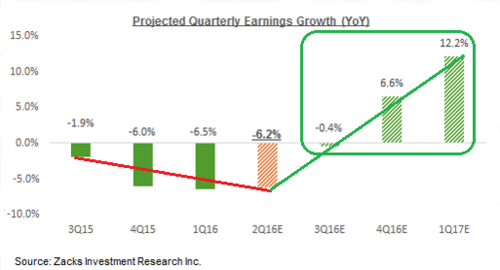

The latest rally in the markets suggests investors are pricing in an earnings recovery for Q3 that we have discussed in past posts. [vi]

There is no doubt that investors have bid the markets up, with expectations that Q2 earnings reports will beat very low expectations. With 7% of the companies in the S&P 500 reporting earnings to date for Q2 2016, 66% have reported earnings above the mean estimate and 51% have reported sales above the mean estimate. [vi]

The other phenomenon that might be creating a rally in equity markets, is the simple fact that there's not much else to buy.

Fixed Income is at historically high valuations. Remember, bond yields drop as bond prices rise. [vii]

Real Estate across most asset classes (Apartments, Commercial and Retail) are trading at near historic valuations. [viii]

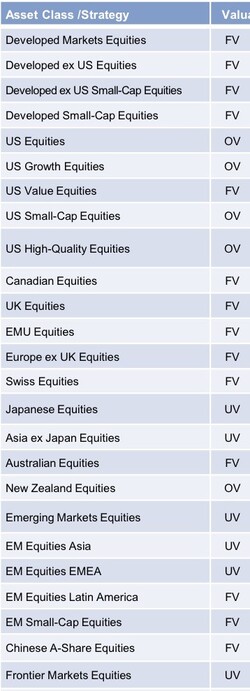

In fact, a leading research firm lists most asset classes as overvalued (OV) vs. fairly valued (FV) or undervalued (UV).

Your alternative to buying assets is to consume. However, it’s hard to fathom that investors will consume massive amounts in lieu of investing.

Recently, investors have done the opposite from consuming. Investors continue to chase one of the most expensive asset classes, U.S. Treasuries. You can see the yield curve below Long-Term Treasuries have been bid up to historic highs (or lows on a yield basis). [ix]

What does all this mean?

- There are not many alternatives to buying U.S. equities in spite of their elevated valuations.

- There is a lot of fear in the debt markets, pushing investors to seek the safe haven of U.S. Treasuries.

- Investors are betting on an earnings growth period starting in Q3, and are running stocks up in anticipation of the end of an earnings recession.

- If an earnings growth recovery fails to materialize, the U.S. equity markets could contract and test the lows set in February, which would be an 18% correction. [x]

- The policy driven world we live in is working. Central Banks have inflated risk assets and created wealth in the absence of earnings to support such valuations. How long this will last is anyone's guess.

While we wait out the next several weeks as the data comes in, the choices for investors are limited to what they can buy!

If you have questions or comments, please let us know as we always appreciate your feedback. You can get in touch with us via Twitter, Facebook, or you can email me directly. For additional information on this, please visit our website.

Tim Phillips, CEO – Phillips & Company

Chris Porter, Senior Investment Analyst – Phillips & Company

References:

[ii] http://seekingalpha.com/article/3988022-chart-day-russell-2000-10-percent-last-10-trading-days

[iii] http://www.wsj.com/mdc/public/page/2_3021-peyield.html

[iv] https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/guide-to-the-markets/viewer

[v] https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/guide-to-the-markets/viewer

[vi] http://www.factset.com/websitefiles/PDFs/earningsinsight/earningsinsight_7.15.16

[vii] https://www.zacks.com/commentary/85922/early-read-on-the-q2-earnings-season

[viii] https://fred.stlouisfed.org/series/DGS10

[ix] http://www.realtor.com/news/real-estate-news/home-prices-hit-all-time-high-may-2016/

[x] http://www.cambridgeassociates.com/our-insights/

[xi] https://am.jpmorgan.com/us/en/asset-management/gim/adv/insights/guide-to-the-markets/viewer